🧬 CNTA $563K Bullish Call Bet - Sleep Disorder Biotech Swings for Blockbuster! 💊

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $563,000 on CNTA call options this morning at 10:44:08! This aggressive bet bought 5,000 contracts of $30 strike calls expiring December 19th - betting on an 8.7% rally from $28.88 over the next 17 days. With Centessa sitting on Phase 2a narcolepsy data that's already driven a 200%+ rally from the 52-week low, smart money is positioning for another leg higher ahead of Q1 2026 pivotal trial initiation. Translation: Institutional investors are loading up before the next catalyst wave hits!

📊 Company Overview

Centessa Pharmaceuticals (CNTA) is a clinical-stage pharmaceutical company racing to compete with Takeda and Alkermes in the exploding sleep disorder market:

- Market Cap: $4.21 Billion

- Industry: Pharmaceutical Preparations

- Current Price: $28.59

- Primary Business: Developing ORX750 (OX2R agonist) for narcolepsy type 1 (NT1), narcolepsy type 2 (NT2), and idiopathic hypersomnia (IH); SerpinPC for hemophilia; other pipeline assets

- Headquarters: Altrincham, Cheshire, UK (114 employees)

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 10:44:08):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:44:08 | CNTA | BUY | CALL $30 | 2025-12-19 | $563K | $30 | 5,000 | 1,600 | 4,500 | $28.88 | $1.25 | CNTA20251219C30 |

🤓 What This Actually Means

This is an aggressive bullish bet on near-term upside! Here's what went down:

- 💸 Solid premium paid: $563K ($1.25 per contract × 4,500 contracts executed out of 5,000 volume)

- 🎯 Strike selection: $30 provides just 3.9% upside from $28.88 - targeting quick move

- ⏰ Short-dated: Only 17 days to expiration (December 19) - betting on IMMEDIATE catalyst

- 📊 Big size: 5,000 contracts traded represents 500,000 shares worth ~$14.4M

- 📈 Opening position: Volume (5,000) >> Open Interest (1,600) signals NEW money entering

- 🏦 Institutional conviction: This is a calculated bet on specific near-term catalyst(s)

What's really happening here: This trader believes CNTA is heading higher FAST. With the stock trading at $28.88, they're paying $1.25 per share for the Dec 19 $30 calls which need the stock above $31.25 to profit (8.2% rally in 17 days). They could've bought cheaper strikes or longer-dated options, but chose DECEMBER expiration for a reason - they expect something to happen THIS MONTH.

Timing clues:

- 🎤 Piper Sandler Healthcare Conference: TODAY (Dec 2) at 3:00 PM ET

- 🎤 Evercore Healthcare Conference: Tomorrow (Dec 3) at 9:35 AM ET

- 🎤 Oppenheimer Movers in Rare Disease Summit: December 11

- 🚀 Q1 2026 Pivotal Trial Initiation: Expected announcement in next 4-6 weeks

Smart money is betting Centessa drops bullish news at one of these investor conferences - new partnership, trial design details, expanded OpenAI-like collaboration, or accelerated timeline announcement.

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL (Z-score 8.78) - This happens maybe 2-3 times per year for CNTA! The volume-to-open-interest ratio of 3.125 signals this is NOT routine hedging - this is fresh conviction. Only 0 similar trades in past 30 days at this size.

Strategy Classification: Long Call (standalone directional bet on upside)

📈 Technical Setup / Chart Check-Up

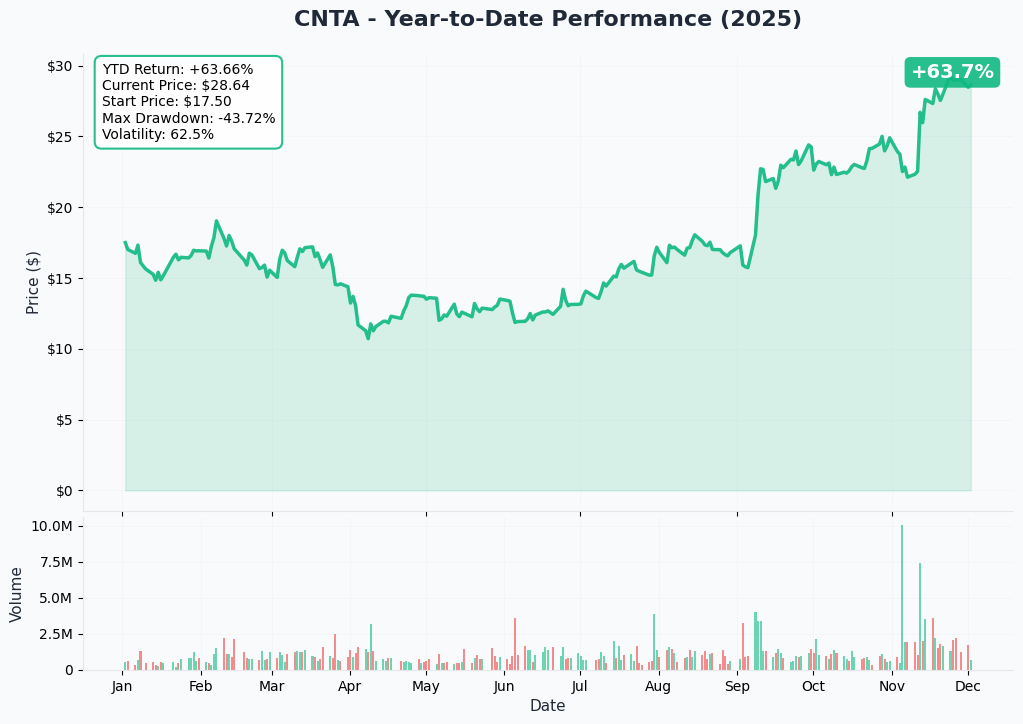

YTD Performance Chart

CNTA is absolutely crushing it in 2025 - the chart tells the story of a biotech hitting all the right clinical milestones. Starting the year around $10-12, the stock traded sideways through August before EXPLODING in early November on Phase 2a CRYSTAL-1 data.

Key observations:

- 🚀 Massive November breakout: Vertical move from ~$18 on Nov 1 to peak of $29.99 on clinical data

- 📊 200%+ rally from lows: Stock bottomed at $9.60 in 52-week range, now at $28.59

- 💰 $250M capital raise catalyst: Stock surged 18% on November 12 when pricing $250M offering at $21.50

- 📈 Strong institutional accumulation: 82.01% institutional ownership shows smart money loading up

- 🎯 Testing all-time highs: Current price near $29.99 resistance level

- 🔄 Recent consolidation: Trading in tight $27-30 range after initial pop - coiling for next move

The November 5 Phase 2a data release was the KEY catalyst - ORX750 showed >20 minute MWT improvement and 87% cataplexy reduction with favorable safety profile. The stock initially dipped (profit-taking), then rallied hard into the $250M raise, and has been consolidating ever since. This consolidation at elevated levels (rather than giving back gains) shows strong hands holding.

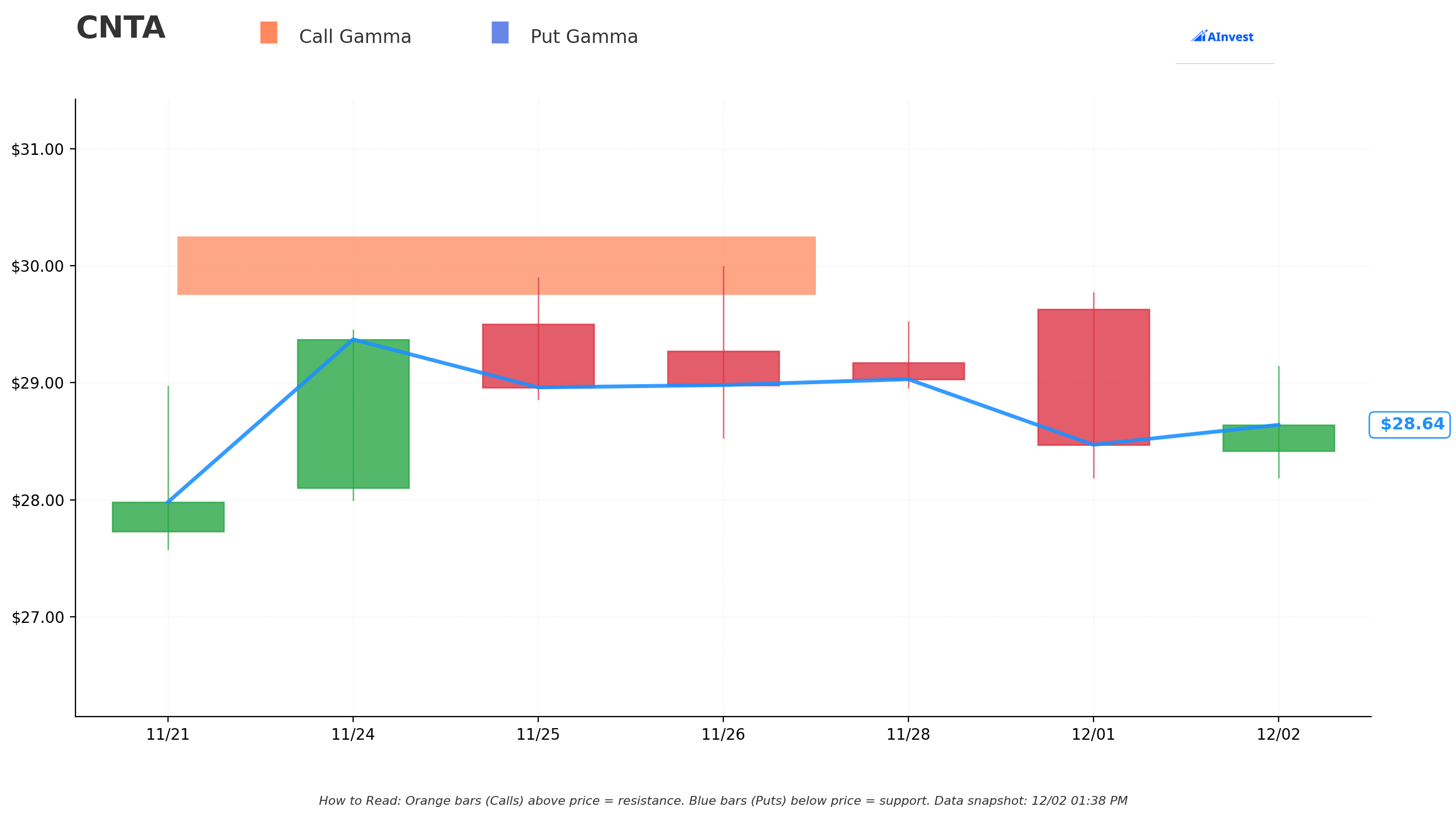

Gamma-Based Support & Resistance Analysis

Current Price: $28.59

The gamma exposure map reveals critical price magnets and barriers for near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $25.00 - Major support with 0.251B total gamma exposure (strongest floor below current price!)

- Put GEX: 0.144B vs Call GEX: 0.108B = net bearish positioning

- Distance: 12.6% below current price

- This is THE line in the sand - break below and momentum shifts

🟠 Resistance Levels (Call Gamma Above Price):

- $30.00 - MASSIVE resistance with 0.415B total gamma (STRONGEST LEVEL - exactly where this call trade is struck!)

- Call GEX: 0.409B vs Put GEX: 0.006B = overwhelmingly bullish positioning

- Distance: 4.9% above current price

- This is where market makers have enormous call exposure - creates natural ceiling

What this means for traders: CNTA is trading in a CRITICAL zone between $25 support and $30 resistance. The gamma data shows the $30 level has 0.415B total exposure (65% higher than $25 level) - this is THE line to break for the next leg higher. The call buyer struck EXACTLY at $30 where there's 0.409B call gamma - they're betting on a breakout above this massive resistance within 17 days.

Here's the play: If CNTA breaks $30 convincingly (with volume), the call gamma forces market makers to BUY stock to hedge their short calls, creating explosive upside acceleration. This is what the call buyer is betting on - a gamma squeeze through $30 that shoots the stock to $32-35 quickly.

Net GEX Bias: Bullish (0.916B call gamma vs 0.388B put gamma = 2.36:1 ratio) - Overall positioning remains VERY bullish with call buyers dominating. The stock wants to go higher - it just needs a catalyst to break $30.

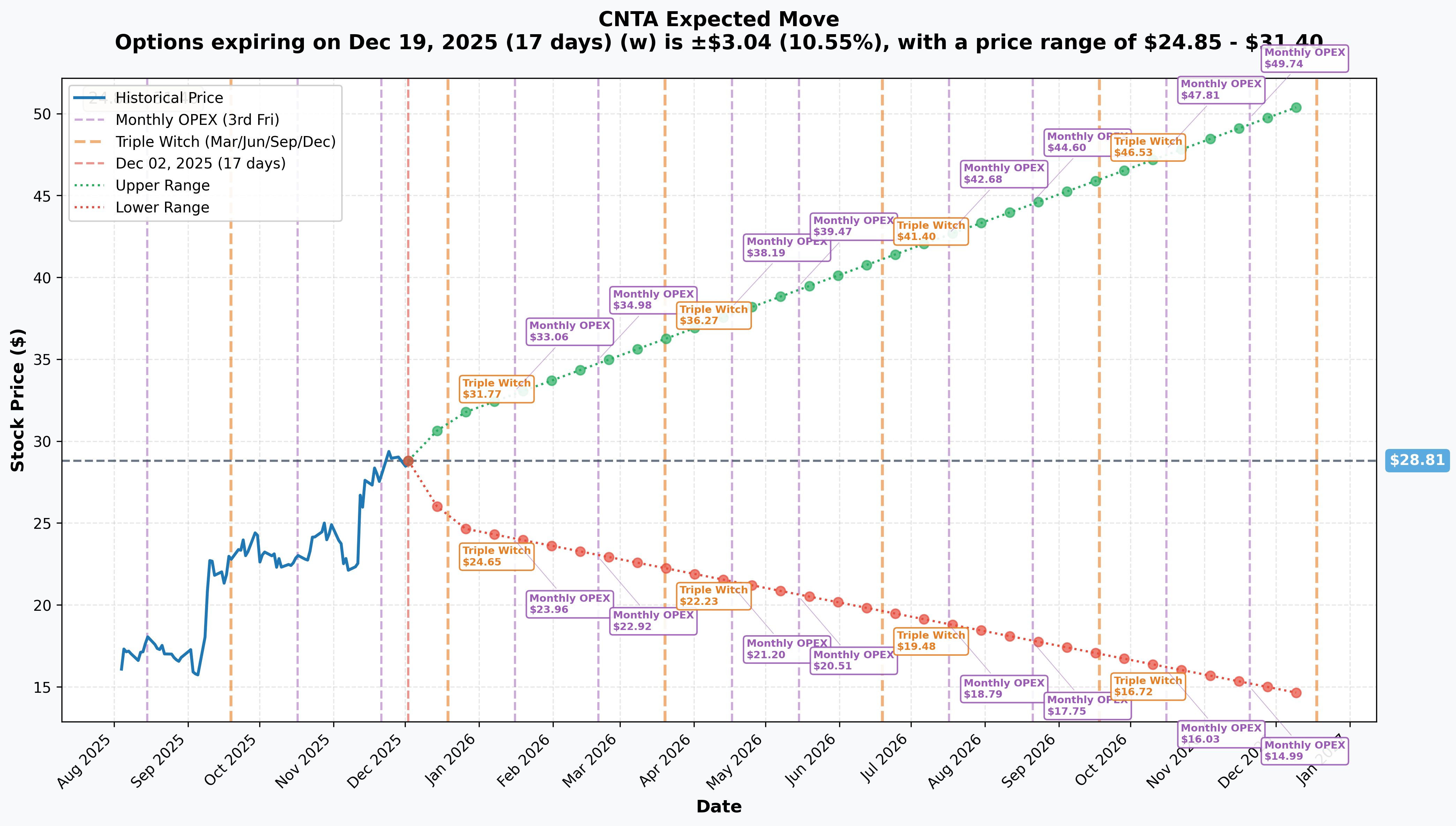

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX / Triple Witch (Dec 19 - 17 days - THIS TRADE!): ±$3.04 (±10.55%) → Range: $24.85 - $31.40

- 📅 January OPEX (Jan 16 - 45 days): ±$4.08 (±14.16%) → Range: $23.96 - $33.06

- 📅 February OPEX (Feb 20 - 80 days): ±$5.14 (±17.75%) → Range: $22.92 - $34.98

- 📅 March Triple Witch (Mar 20 - 108 days): ±$5.76 (±19.86%) → Range: $22.24 - $36.26

- 📅 LEAP expiration (Dec 18, 2026 - 381 days): ±$16.02 (±55.61%) → Range: $14.39 - $50.86

Translation for regular folks: Options traders are pricing in a 10.55% move ($3.04) through December 19 expiration - that's HUGE for a 17-day window! The upper range of $31.40 is ABOVE the $30 strike, meaning the market thinks there's a legitimate shot at this call trade paying off.

The longer-dated moves get progressively larger: 14% (January), 18% (February), 20% (March) reflecting increasing uncertainty around Q1 2026 pivotal trial initiation timing and design details. The 1-year LEAP implied move of 55.6% shows the market expects MASSIVE volatility over next 12 months - either ORX750 delivers and stock doubles to $45-50, or clinical setbacks cut it in half to $14-15.

Key insight: The December 19 implied move perfectly captures the upcoming investor conferences (Dec 2, 3, 11) and potential Q1 2026 trial announcement. The call buyer is betting the actual move exceeds the 10.55% expectation - they need 8.2% just to breakeven, so they're implying a 12-15% rally is coming.

🎪 Catalysts

🔥 Immediate Catalysts (Next 2 Weeks - INSIDE THE OPTION EXPIRATION!)

Investor Conference Schedule (THIS IS WHY THEY BOUGHT DECEMBER EXPIRATION!) 🎤

-

📅 Piper Sandler Healthcare Conference - TODAY (Dec 2, 2025) @ 3:00 PM ET

- Live webcast available

- Probability: 40% chance of material news drop during Q&A

- Potential announcements: Pivotal trial design details, partnership updates, MI325X/MI350 timeline clarity

-

📅 Evercore Healthcare Conference - TOMORROW (Dec 3, 2025) @ 9:35 AM ET

- Live webcast available

- Probability: 35% chance of new information

- Management typically provides updates across multiple conferences - cumulative impact matters

-

📅 Oppenheimer Movers in Rare Disease Summit - December 11, 2025

- Details at investors.centessa.com

- Probability: 30% chance of orphan drug designation news or rare disease expansion commentary

- Focused investor audience may elicit more detailed pipeline discussion

Why these conferences matter: Biotech companies often use investor conferences to "soft launch" news before formal press releases. Management may provide:

- 🎯 Specific Q1 2026 pivotal trial start dates (vs vague "Q1" guidance)

- 📊 Enrollment projections, trial design details, endpoint selection

- 🤝 Partnership discussions or collaboration announcements

- 💰 Capital allocation priorities post-$250M raise

- 🚀 Accelerated MI350/ORX142/ORX489 timelines

The call buyer clearly expects something substantive THIS WEEK or next that moves the stock above $30.

🚀 Near-Term Catalysts (Q4 2025 - Q1 2026)

Pivotal Trial Initiation: ORX750 Registrational Program (Q1 2026 - HIGHEST IMPACT!) 🎯

According to Centessa's November 5 guidance, the company expects to initiate pivotal trials for ORX750 across NT1, NT2, and IH indications in Q1 2026 (January-March):

- 🏆 Market Opportunity: U.S. narcolepsy market $2.23B by 2033 (CAGR 7.88%), global market $6.04B by 2030 (CAGR 8.04%)

- 💪 Competitive Edge: Only OX2R agonist with robust Phase 2a data across all three indications (NT1, NT2, IH)

- 📈 Peak Sales Forecast: $875M by 2031 vs Takeda's oveporexton at $1.26B

- 🎯 Trial Design Clarity: Announcement of enrollment targets, endpoints, and timelines will be MAJOR catalyst

- 💰 Funded with $619M cash: $250M raise in November extended runway into 2028

Probability Assessment: 85-90% trial initiation happens in Q1 2026 based on positive Phase 2a data and confirmed company guidance. The TIMING announcement (exact start date) could come at December conferences.

Patient Studies: ORX142 and ORX489 (Q1 2026) 🧪

According to BioSpace reporting, Centessa plans to initiate patient studies for TWO additional OX2R agonists in Q1 2026:

- 🔬 ORX142: Targets neurological/neurodegenerative disorders with rapid onset of action, Phase 1 data showed dose-dependent MWT improvements

- 💊 ORX489: "Most potent OX2R agonist to date" targeting neuropsychiatric disorders

- 🎯 Portfolio Diversification: Three shots on goal in OX2R space reduces binary risk vs single-asset biotechs

- 📊 Market Expansion: ORX142/ORX489 address different patient populations than ORX750

Analyst Price Target Momentum (BUILDING CONVICTION!) 📊

Recent flurry of analyst activity shows growing Street confidence:

| Date | Firm | Action | Price Target | Prior Target |

|---|---|---|---|---|

| December 2 | B. Riley | Raised PT | $42 | $33 |

| November 18 | Guggenheim | Raised PT, Buy | $43 | $28 |

| November 13 | Wells Fargo | Raised PT, Overweight | $35 | $30 |

Consensus: 10 analysts covering with Strong Buy rating, average PT $37.10 (29% upside from $28.78), range $19-$43

Notice the acceleration: B. Riley raised their target TODAY (Dec 2) from $33 to $42 - that's a 27% increase! This suggests new information or increased confidence in near-term catalysts. The average Street target of $37 is well above the $30 call strike.

📊 Q4 2025 Earnings (Expected February 2026)

Expected mid-February 2026 based on historical 45-day post-quarter pattern:

Key Metrics to Watch:

- 💰 Updated cash position: Expected ~$619M after $250M November raise

- 🔥 R&D expense trajectory: Q3 was $41.6M, expect increase with pivotal trials

- 🚀 Pivotal trial enrollment updates and timelines

- 📈 Collaboration revenue: TTM was $15.0M, up 118.88% YoY

- 🎯 2026 guidance and catalyst calendar

🔬 Recently Completed Catalysts (Context for Current Positioning)

Phase 2a CRYSTAL-1 Results - November 5, 2025 ✅

Centessa reported positive data from initial dosing cohorts in CRYSTAL-1 study:

- 💪 NT1 Efficacy (1.5 mg dose): >20 minute increase in MWT vs placebo (p=0.0026)

- 🎯 Cataplexy Reduction: 87% relative reduction vs placebo (p=0.0025)

- ✅ Safety Profile: Well-tolerated across all doses, no serious safety signals

- Most common side effects: pollakiuria (51%), insomnia (22%), dizziness (13%), headache (11%)

- All treatment-emergent adverse events (TEAEs) were transient and mild to moderate

- No clinically meaningful cardiac, visual, liver, or renal changes

- 📊 Study Population: 55 participants across NT1, NT2, and IH completed 2-week crossover dosing

This was the catalyst that drove the stock from ~$18 to $30 - the data de-risked the pivotal program significantly.

$250M Capital Raise - November 12, 2025 ✅

Centessa priced offering at $21.50, selling 11,627,907 ADSs:

- 💰 Gross proceeds: ~$250 million

- 📊 Stock reaction: Surged 18% on announcement day

- 🎯 Extended runway: From mid-2027 to into 2028

- 🏦 Underwriters: Jefferies and Guggenheim Securities

The positive market reaction (18% pop vs typical biotech dilution selloffs) showed investors WANTED Centessa to have more cash to fund the aggressive ORX750 pivotal program across three indications plus ORX142/ORX489 development.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through December 19 expiration (17 days):

📈 Bull Case (35% probability)

Target: $32-35

How we get there:

- 🎤 Management announces specific Q1 2026 pivotal trial start date (e.g., "We will dose first patient week of January 15, 2026") at Piper Sandler or Evercore conferences

- 🤝 Partnership/collaboration announcement with larger pharma player for commercial rights or co-development (similar to OpenAI-AMD deal structure)

- 📊 New analyst coverage initiation or major bank upgrade citing Phase 2a data quality and market opportunity

- 🚀 ORX142/ORX489 timeline acceleration or positive preclinical data release

- 💰 Institutional investor day announcement providing detailed 2026 roadmap

- 📈 Breakout above $30 gamma resistance triggers short squeeze and momentum buying toward implied move upper range of $31.40

- 🎯 Technical breakout above November 26 high of $29.99 brings in momentum traders

Key metrics needed:

- Conference presentation with substantive new information (not just rehash of Phase 2a data)

- Volume expansion above 2M average on positive news

- Break above $30 on heavy volume (confirms gamma squeeze potential)

- Analyst community reacting positively with PT raises

Call option P&L in Bull Case:

- Stock at $32 on Dec 19: Calls worth $2.00, profit = $0.75/share × 4,500 = $337.5K gain (60% ROI)

- Stock at $35 on Dec 19: Calls worth $5.00, profit = $3.75/share × 4,500 = $1.69M gain (300% ROI!)

Probability assessment: 35% because it requires a SPECIFIC catalyst in the next 17 days. The December conference schedule creates legitimate shot at news. Gamma setup at $30 supports explosive move if broken. Recent analyst momentum (B. Riley to $42 TODAY) shows Street getting more bullish.

🎯 Base Case (45% probability)

Target: $27-30 range (SIDEWAYS CONSOLIDATION)

Most likely scenario:

- 📊 Conference presentations provide color but no major new info - management sticks to "Q1 2026" timeline without specifics

- 🤝 No partnership announcements - still in discussions phase

- 📈 Stock continues trading in tight $27-30 consolidation range established since late November

- ⚖️ Positive sentiment maintained but no catalyst strong enough to break $30 resistance

- 💤 Holiday seasonally light trading (Dec 15-31) limits volatility

- 🎯 Market waits for January/February timeframe when pivotal trial details and Q4 earnings arrive

- 📊 Implied move plays out but stock stays WITHIN the range rather than testing extremes

- 💰 Call buyers who paid $1.25 hoping for quick pop get time decay and modest loss

Call option P&L in Base Case:

- Stock at $29 on Dec 19: Calls worth $0 (out-of-money), loss = -$1.25/share × 4,500 = -$562.5K loss (100%)

- Stock at $30 on Dec 19: Calls worth $0 (at-the-money), loss = -$1.25/share × 4,500 = -$562.5K loss (100%)

This is why options are risky: Even if the stock does NOTHING wrong and holds $28-29 range (perfectly respectable for a biotech that's already up 200%), the call buyer loses their entire $563K because they need the stock ABOVE $31.25 to profit.

Why 45% probability: Biotech conference presentations usually don't move stocks dramatically unless there's unexpected news. Management tends to be conservative with guidance. The $30 gamma resistance is real and hard to break without volume catalyst. December holiday trading typically favors consolidation over breakouts.

📉 Bear Case (20% probability)

Target: $24-27 (PULLBACK TO SUPPORT)

What could go wrong:

- 😰 Conference presentations disappoint - no new trial details, vague Q1 timeline, conservative commentary

- ⏰ Pivotal trial delay whisper - management hints at "late Q1 or early Q2" vs "early Q1" expectation

- 💸 Profit-taking ahead of holidays - institutions locking in 150%+ YTD gains, reducing exposure into year-end

- 🇨🇳 Macro selloff in biotech sector or broader market weakness drags CNTA lower

- 📊 Analyst downgrade or PT cut citing valuation stretch at $4.2B market cap for Phase 2 asset

- 🚨 Competitive news - Takeda or Alkermes announces positive development in competing OX2R programs

- 💀 Safety signal emergence - new data or analysis raises questions about 51% pollakiuria incidence or urinary urgency issues

- 🔨 Break below $27 support accelerates selling toward $25 gamma floor (12.6% below current)

Critical support levels:

- 🛡️ $27: Recent consolidation floor - MUST HOLD or momentum shifts

- 🛡️ $25: Major gamma support (0.251B total GEX) - likely heavy buying here

- 🛡️ $24.85: December implied move lower range - disaster scenario

Call option P&L in Bear Case:

- Stock at $27 on Dec 19: Calls worth $0, loss = -$1.25/share × 4,500 = -$562.5K loss (100%)

- Stock at $25 on Dec 19: Calls worth $0, loss = -$1.25/share × 4,500 = -$562.5K loss (100%)

Probability assessment: Only 20% because fundamentals remain strong (positive Phase 2a data, $619M cash, clear path to pivotal trials). The recent $250M raise at $21.50 provides technical support - institutions who bought at $21.50 unlikely to sell at $25-27. Short interest of 3.35M shares creates potential short-squeeze fuel. Analyst community remains bullish with $37 average target.

💡 Trading Ideas

🛡️ Conservative: Wait for Pivotal Trial Clarity

Play: Stay on sidelines until Q1 2026 pivotal trial initiation is CONFIRMED with details

Why this works:

- ⏰ Stock already up 200%+ from lows - no FOMO needed, you haven't "missed it"

- 💸 Options premium expensive at current implied volatility levels (10.55% for 17 days)

- 📊 Current $28.59 price assumes significant success - if trials delayed or disappoint, 30-40% correction possible

- 🎯 Better entry likely in January-February if stock pulls back or if trial news creates dip-buying opportunity

- 🤔 The $563K call buyer is making a SPECULATIVE bet on December catalyst - you don't have to match their risk tolerance

- 📈 Long-term thesis intact regardless of December conference noise

Action plan:

- 👀 Watch December 2, 3, and 11 conference presentations for any material updates

- 🎯 Look for pullback to $24-26 range (near $250M raise price of $21.50 adjusted for time) as ideal stock entry

- ✅ Wait for CONCRETE pivotal trial announcement: patient enrollment start, trial sites activated, endpoints confirmed

- 📊 Monitor competitive landscape - Takeda's oveporexton and Alkermes' alixorexton timelines

- ⏰ Revisit in late January when Q1 2026 trial initiation becomes imminent and Q4 earnings provide update

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if conferences disappoint. Maintain optionality. Get better entry with more clarity on pivotal program.

⚖️ Balanced: March Call Spread (Copy The Setup With More Time)

Play: Buy call spread targeting $30-35 range with March 20 expiration (108 days vs 17 days)

Structure: Buy $30 calls, Sell $35 calls (March 20 expiration)

Why this works:

- 🎯 Captures ALL Q1 2026 catalysts: Pivotal trial initiation, Q4 earnings, analyst days, partnership potential

- ⏰ Much more time - 108 days vs 17 days gives thesis time to play out without weekly theta bleed

- 💰 Defined risk spread - Max loss is limited to net debit paid (likely $2-3 per spread)

- 📈 Same price targets as the unusual activity trade but with realistic timeframe

- 🎢 Lower implied volatility on March options vs December = better value

- 🛡️ Selling $35 call reduces cost and caps upside at level matching analyst targets

Estimated P&L (current market - adjust for fills):

- 💰 Pay ~$2.50-3.00 net debit per spread (buy $30 call ~$4.50, sell $35 call ~$2.00)

- 📈 Max profit: $2.00-2.50 if CNTA above $35 at March expiration (80-100% ROI)

- 📉 Max loss: $2.50-3.00 if CNTA below $30 (100% loss but smaller dollar amount vs naked calls)

- 🎯 Breakeven: ~$32.50-33.00

- 📊 Risk/Reward: ~1:1 which is fair for biotech speculation

Entry timing:

- ⏰ Enter on ANY pullback to $27-28 (better entry than current $28.59)

- 🎯 Alternatively, wait until January for Q1 trial announcement, then enter on "buy the news" dip

- ❌ Skip if stock already above $31 (spread too close to in-the-money)

Position sizing: Risk only 5-10% of portfolio (this is directional speculation on clinical success)

Risk level: Moderate (defined risk, long timeframe) | Skill level: Intermediate

Why this beats the unusual activity trade: The $563K buyer is betting on 17-day catalyst. You get 108 days to be right, lower cost due to spread, and still participate in same upside thesis. Much smarter structure for retail.

🚀 Aggressive: Earnings + Pivotal Trial Straddle (ADVANCED ONLY!)

Play: Buy straddle betting on massive volatility around Q4 earnings and Q1 trial announcement

Structure: Buy $30 calls + Buy $30 puts (March 20 expiration)

Why this could work:

- 💥 Binary outcomes: Pivotal trials either start on schedule with great design (stock to $40+) or encounter delays/issues (stock to $20-22)

- 🎰 Betting the Street is UNDERPRICING biotech volatility - implied move of 19.86% for March may be too low

- 📊 At $4.2B market cap for Phase 2 asset, stock could EXPLODE either direction based on trial execution

- 🚀 Partnership announcement could send stock to $45-50 (jazz/takeda acquisition interest)

- ⚡ Only need stock to move >20% either way to profit

- 📈 March expiration captures Q4 earnings (mid-Feb) + pivotal trial initiation (Jan-Mar)

Why this could blow up (SERIOUS RISKS):

- 💸 VERY EXPENSIVE: Straddle costs ~$8-10 ($800-1,000 per straddle at current prices)

- ⏰ HUGE TIME DECAY: Theta burns as you wait for catalysts

- 😱 IV CRUSH POST-EVENTS: Even if stock moves 15%, IV collapse after earnings/trial news could still result in LOSS

- 📊 Two-way risk: Stock could consolidate $25-32 range and you lose entire premium

- 🎢 Need 25-30% move to breakeven after paying for both calls and puts

- ⚠️ "Good but not great" scenario kills you - trial starts but design is conservative, stock moves to $32-33 (only 12% move) and straddle loses 40-50%

Estimated P&L:

- 💰 Cost: ~$8-10 per straddle (using current March 20 $30 strike pricing)

- 📈 Profit scenario: Stock moves to $42+ or $18- (40%+ move) = $8-12 gain (80-120% ROI)

- 🚀 Home run: Stock acquired at $50 or trials delayed to $18 = $20+ gain (200%+ ROI)

- 📉 Loss scenario: Stock ends $26-34 range = lose $5-8 (50-80% loss)

- 💀 Total loss: Stock stays near $30 = lose entire $8-10 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$38-40 (need 30%+ rally)

- 📉 Downside breakeven: ~$20-22 (need 30% drop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded biotech straddles through binary events before

- ✅ Can afford to lose ENTIRE premium (very real possibility with biotech!)

- ✅ Understand you're betting AGAINST options market's probability estimates

- ✅ Can monitor position daily and manage post-catalyst (don't hold to expiration)

- ✅ Accept that even if you're RIGHT on direction, IV crush could still cause loss

- ⏰ Have plan to close one leg after directional move and let runner ride

Risk level: EXTREME (can lose 100% of premium easily) | Skill level: Advanced only

Probability of profit: ~35% (lower than 50% due to wide breakevens and IV crush)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🇨🇳 Takeda and Alkermes head-to-head competition: Takeda's oveporexton expected 2026 approval with $1.26B peak sales forecast - 2 years ahead of ORX750's 2028 timeline. Alkermes racing to Phase 3 with Q1 2026 initiation (same timing as Centessa). First-mover advantage and market share capture could limit ORX750's commercial potential even if trials succeed. Lack of head-to-head data makes "best-in-class" claim difficult to prove.

-

⚖️ Pivotal trial execution risk with three-indication program: Running registrational studies across NT1, NT2, AND IH simultaneously requires flawless execution, huge capital, and complex logistics. Phase 3 trials may not replicate Phase 2a efficacy (>20 min MWT, 87% cataplexy reduction) in larger populations. Any delay, enrollment challenges, or safety signals emerging would crater stock 40-50%.

-

💸 Valuation stretched at $4.21B for Phase 2 asset: Current market cap prices in significant pivotal trial success. At 74.8x forward P/E (estimated), stock has minimal margin of safety. Requires $875M peak sales by 2031 to justify valuation - any reduction in peak sales estimates triggers multiple compression. Stock already up 200%+ from lows - much of "good news" already reflected in price.

-

🚨 Safety signal risk - pollakiuria and urinary urgency: 51% of patients experienced pollakiuria (frequent urination) in Phase 2a trials, with one discontinuation due to urinary urgency. While labeled "transient and mild to moderate," this could become tolerability issue in real-world use. FDA may require additional safety studies or black box warnings. Competing Jazz product (JZP441) was halted due to visual disturbances - safety bar is high.

-

🏭 Cash runway concerns despite $250M raise: Current runway extends into 2028 but running pivotal trials across three indications (NT1, NT2, IH) plus ORX142/ORX489 development will be capital-intensive. Q3 R&D was $41.6M, expect significant increase as trials ramp. May require additional dilutive financing before commercialization (2027-2028), further diluting shareholders. Burn rate acceleration could spook investors.

-

💰 No commercial infrastructure or partner: Centessa lacks sales force, marketing team, or distribution network. Must either build internal commercial team (expensive, 18-24 month lead time) or partner with big pharma (revenue share, loss of control). Partnership negotiations could delay launch or result in unfavorable economics. Decision needed by 2026-2027 for 2028 readiness.

-

🎢 Extreme biotech volatility - max drawdown risk: YTD chart shows stock can move 20-30% on single news items. Historical volatility and clinical-stage binary risk means CNTA can gap down 40%+ on trial delays, safety issues, or competitive setbacks. This is NOT a "set and forget" investment - requires active monitoring and position management. Short interest of 3.35M shares creates two-way volatility risk.

-

📉 Regulatory approval uncertainty beyond trials: Even if pivotal trials succeed, FDA may require additional studies, raise safety concerns, or impose restrictive labeling. SerpinPC hemophilia program has been in registrational studies with limited updates, suggesting regulatory path not always smooth. 2028 approval timeline could slip to 2029-2030.

-

🎯 Market share capture vs incumbents (Jazz, Harmony): Jazz's Xyrem/Xywav dominate narcolepsy treatment, Harmony's WAKIX approved for pediatric patients. Established players have payer relationships, formulary access, and physician mindshare. ORX750 will face pricing pressure and access barriers even if clinically superior. Peak sales may disappoint vs $875M forecasts.

-

🔬 Clinical trial design and endpoint selection risk: FDA expectations for narcolepsy endpoints evolving. Company must select endpoints that satisfy regulators while being achievable in trials. Wrong endpoint choice could lead to "successful" trial that doesn't support approval. NT2 and IH have fewer precedents than NT1 - regulatory path less certain.

-

💔 December option buyer could be WRONG: The $563K call buyer may have inside information we don't (unlikely given compliance), or they may simply be wrong about December catalyst timing. Following institutional trades blindly is dangerous - they have different risk profiles, time horizons, and information. This could be a speculative hedge or part of complex multi-leg strategy we can't see.

🎯 The Bottom Line

Real talk: Someone just bet $563K that CNTA breaks above $30 in the next 17 days. That's a BOLD call on a biotech that's already up 200%+ from its lows and trading near all-time highs. This isn't a "safe" bet - this is aggressive speculation on a near-term catalyst (likely the December investor conferences or accelerated pivotal trial announcement).

What this trade tells us:

- 🎯 Buyer expects SPECIFIC news in December 2025 (not vague "Q1 2026" timeline)

- 💰 They're comfortable losing all $563K if wrong (this is RISK CAPITAL, not safe money)

- ⚖️ The $30 strike choice is deliberate - matches major gamma resistance and analyst consensus range

- 📊 December 19 expiration captures upcoming conferences (Dec 2, 3, 11) and potential early Q1 trial news

- ⏰ Short-dated = high conviction on timing, but also HIGH RISK of total loss

This is NOT a "follow blindly" signal - it's a "pay attention" signal.

If you own CNTA:

- ✅ You've already WON - stock up 200%+ from $9.60 lows to $28.59. Congratulations!

- 📊 Consider trimming 20-30% at $28-30 levels to lock in gains and reduce risk

- ⏰ Watch December 2, 3, and 11 conference presentations CLOSELY for material updates

- 🎯 Set MENTAL STOP at $25 (major gamma support) to protect remaining position if momentum shifts

- 🛡️ If holding large position, consider buying 1-2 protective $25 puts per 100 shares (insurance strategy)

- 📈 If stock breaks $30 convincingly on news + volume, could re-add trimmed shares for ride to $35-40

If you're watching from sidelines:

- ⏰ Do NOT chase at $28-29 - wait for catalyst clarity or pullback

- 🎯 Better entry at $24-26 if stock consolidates or corrects (near $250M raise price of $21.50)

- 📈 Looking for confirmation: Pivotal trial start date announced, partnership news, analyst upgrades accelerating

- 🚀 Longer-term (Q1 2026), trial initiation and Q4 earnings are legitimate catalysts for $35-42 if execution delivers

- ⚠️ Current $4.2B market cap for Phase 2 asset requires PERFECT execution - one stumble and it's back to $20-22

- 💡 March call spreads offer better risk/reward than chasing short-dated December calls

If you're bearish:

- 🎯 Wait for conference presentations before initiating shorts - momentum still bullish

- 📊 First resistance at $30 (gamma ceiling), support at $27 (consolidation floor), major support at $25

- ⚠️ Post-conference, if no material news, put spreads ($30/$25) offer defined-risk way to play disappointment

- 📉 Watch for failure at $30 - that's the trigger for retest of $25-27 support

- ⏰ Best bearish setup: Stock rallies to $31-32 on hype, then fades on "sell the news" - THAT'S when you short

Mark your calendar - Key dates:

- 📅 December 2 (TODAY) @ 3:00 PM ET - Piper Sandler Healthcare Conference

- 📅 December 3 @ 9:35 AM ET - Evercore Healthcare Conference

- 📅 December 11 - Oppenheimer Movers in Rare Disease Summit

- 📅 December 19 - Monthly OPEX / Triple Witch, expiration of this $563K call trade

- 📅 January-March 2026 - ORX750 pivotal trial initiation expected

- 📅 Mid-February 2026 - Q4 2025 earnings report (45 days post-quarter)

- 📅 Q1 2026 - ORX142 and ORX489 patient studies initiation

Final verdict: CNTA's ORX750 story is INCREDIBLY compelling for the sleep disorder market - positive Phase 2a data across NT1, NT2, and IH, $619M cash to fund pivotal trials, Street targets averaging $37, and clear path to 2028 approval targeting $2.2B+ market. BUT, at $28.59 after 200%+ rally with $4.2B market cap, the risk/reward is NO LONGER overwhelmingly favorable for aggressive new positioning.

The $563K institutional call buy signals someone with CONVICTION expects December news. They may be right! But they're also risking over half a million dollars on a 17-day outcome. That's not smart money for most retail traders.

Be patient. Watch the conferences. Look for pullbacks to $24-26 or wait for Q1 trial clarity. The sleep disorder revolution will still be here in 2-3 months, and you'll sleep better at night (pun intended) paying $25 instead of $29.

This is a marathon clinical development story, not a December sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 8.78 and "extremely unusual" classification reflects this specific trade's size relative to recent CNTA history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Biotech investments carry binary clinical trial risk with potential for 40-50% drawdowns on negative news. The call buyer may have complex portfolio hedging needs or information not applicable to retail traders. Phase 2 to Phase 3 success rates in biotech are approximately 30-40%, meaning 60-70% of drugs fail in pivotal trials.

About Centessa Pharmaceuticals: Centessa Pharmaceuticals plc is a clinical-stage pharmaceutical company developing SerpinPC for hemophilia, ORX750 for narcolepsy and sleep disorders, LB101 for solid tumors, MGX292 for pulmonary arterial hypertension, and other pipeline candidates, with a market cap of $4.21 billion in the Pharmaceutical Preparations industry.