🌊 DOCN: Someone Just Bet $3.9M That DigitalOcean Reaches $75 by 2027!

📅 March 11, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone loaded up $3.9 MILLION on DOCN January 2027 calls this morning — a LEAP bet that DigitalOcean will trade above $75 in 10 months. At today's spot price of $67.54, that's asking for another 11% gain on a stock that's already surging +9.9% today on a monster AI customer win. This isn't a short-term gamble — this is a trader planting a long-horizon flag on DigitalOcean's transformation into an "Agentic Inference Cloud" company. Let's dig in. 👀

📊 Company Overview

DigitalOcean Holdings (DOCN) is a cloud computing platform built for developers, startups, and small-to-medium businesses who want powerful infrastructure without the complexity of AWS or Azure:

- Market Cap: $5.7 Billion

- Industry: Services — Computer Programming, Data Processing

- Current Price: $67.54 (up ~9.9% today on Workato AI migration news)

- Primary Business: On-demand cloud infrastructure (Droplets, managed databases, Kubernetes) and increasingly, AI inference infrastructure through its Gradient / Agentic Inference Cloud platform

- FY2025 Revenue: $901M (+15% YoY) | FY2026 Guidance: $1.075B–$1.105B (+19–23% YoY)

Think of DigitalOcean as the "anti-hyperscaler" — simpler, cheaper, and laser-focused on builders who don't need enterprise bureaucracy. And now, they're rapidly becoming the go-to place for AI startups to run inference workloads at scale.

💰 The Option Flow Breakdown

📊 The Tape — March 11, 2026 @ 10:47:07

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:47:07 | DOCN | BUY | CALL $75 | 2027-01-15 | $3.9M | $75 | 2,500 | 366 | 2,500 | $67.54 | $15.48 | DOCN20270115C75 |

🤓 What This Actually Means

This is a pure directional bet — someone paid $15.48 per contract × 2,500 contracts = $3.9M to own the right to buy DOCN at $75 anytime through January 15, 2027. No hedging. No spread. Just raw conviction that DOCN keeps climbing.

Here's what stands out:

- 💸 $3.9M committed: This isn't someone playing around with a few hundred contracts. That's a serious conviction trade.

- 🏔️ LEAP structure — 10 months out: Choosing January 2027 expiry gives this trade time to capture Q1 2026 earnings (~May), Q2 2026 earnings (~August), the NVIDIA Blackwell GPU Droplet rollout (mid-2026), and AMD MI355X liquid-cooled deployments (Q2 2026). Plenty of runway.

- 📊 Vol/OI Ratio of 6.83: Volume came in at 6.83x the existing open interest of 366 contracts. Translated: whoever did this basically blew out the entire existing position and then some — this isn't piggybacking on an existing crowd, this is a fresh directional statement.

- 🔥 Z-Score: EXTREMELY_UNUSUAL: This trade is statistically far outside normal activity for this contract. It doesn't happen every week — this is the kind of flow that shows up a handful of times per year for a name like DOCN.

- 🎯 Strike at $75 — right where gamma resistance clusters: As we'll see in the chart below, $75 is a significant resistance level in the gamma exposure map. The buyer is essentially targeting a breakout above that zone.

Real talk: This is a trader who did their homework on DigitalOcean's AI pivot, looked at the 2027 growth roadmap, and decided the risk/reward over 10 months was compelling enough to drop nearly $4M. It's a bet that DigitalOcean's "Path to 30%" growth narrative plays out and the stock clears the $75 gamma wall.

📈 Technical Setup / Chart Check-Up

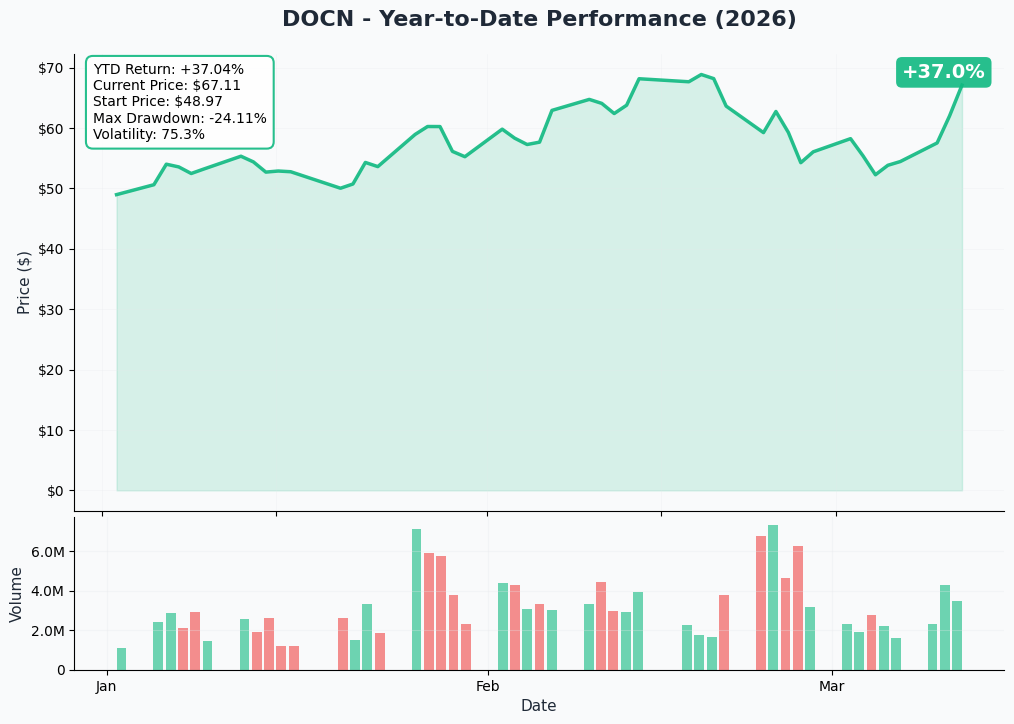

YTD Performance

DOCN has had a remarkable run in 2026. After spending much of late 2025 in the $35–$55 range, the stock has ripped higher on a combination of a strong Q4 2025 earnings beat, accelerating AI customer ARR, and a wave of analyst upgrades. Today's +9.9% move on Workato's AI migration win pushed the stock firmly into the mid-$60s.

Key observations from the chart:

- 🚀 Sustained uptrend: DOCN has essentially more than doubled from the $35 range in December 2025

- 📈 Breaking out today: The +9.9% surge puts the stock near its 52-week high zone ($70.43)

- 🎢 Elevated vol: This isn't a slow-mover — DOCN can gap meaningfully on news, which is exactly why LEAP calls give the buyer breathing room to be right without worrying about timing

- 📊 52-week range: $25.45–$70.43, with current price near the top of the range

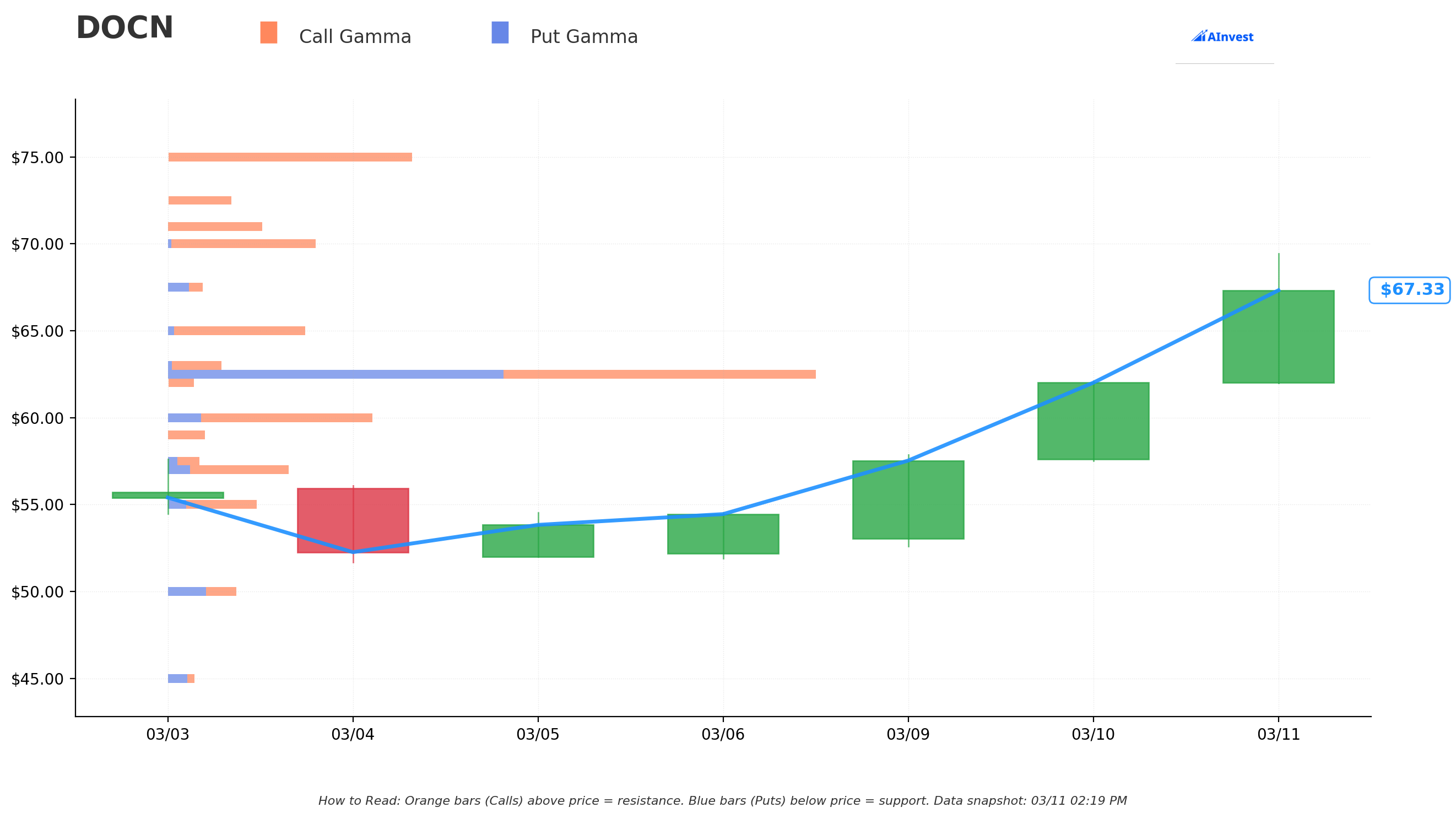

🔵 Gamma-Based Support & Resistance

Current Price: ~$67.19

The gamma exposure map (from options positioning across all active contracts) tells us where the real price magnets and barriers are:

🔵 Support Levels (Blue bars — where market makers will buy the dip):

| Strike | Total GEX | Distance from Spot |

|---|---|---|

| $65 | 0.555B | -3.3% |

| $62.50 | 2.642B | -7.0% (strongest nearby support!) |

| $60 | 0.836B | -10.7% |

| $57 | 0.496B | -15.2% |

| $55 | 0.363B | -18.1% |

The $62.50 level is your key floor — that's where the biggest concentration of gamma lives below the current price. If DOCN pulls back, expect buyers to show up aggressively around $62–$63.

🟠 Resistance Levels (Orange bars — where market makers will sell into strength):

| Strike | Total GEX | Distance from Spot |

|---|---|---|

| $70 | 0.598B | +4.2% (first ceiling!) |

| $71 | 0.383B | +5.7% |

| $72.50 | 0.259B | +7.9% |

| $75 | 0.992B | +11.6% (biggest resistance wall!) |

| $80 | 0.403B | +19.1% |

This is the key insight: The $75 strike — exactly where this $3.9M trade is positioned — is the largest single resistance cluster above current price. The LEAP buyer knows this is a wall that needs to get cleared, and they've structured their trade to profit when/if that happens over the next 10 months.

Net GEX Bias: Bullish (Total call gamma of 7.57B vs put gamma of 2.36B) — overall market structure favors continued upside, but that $75 wall is real and will create friction on the way up.

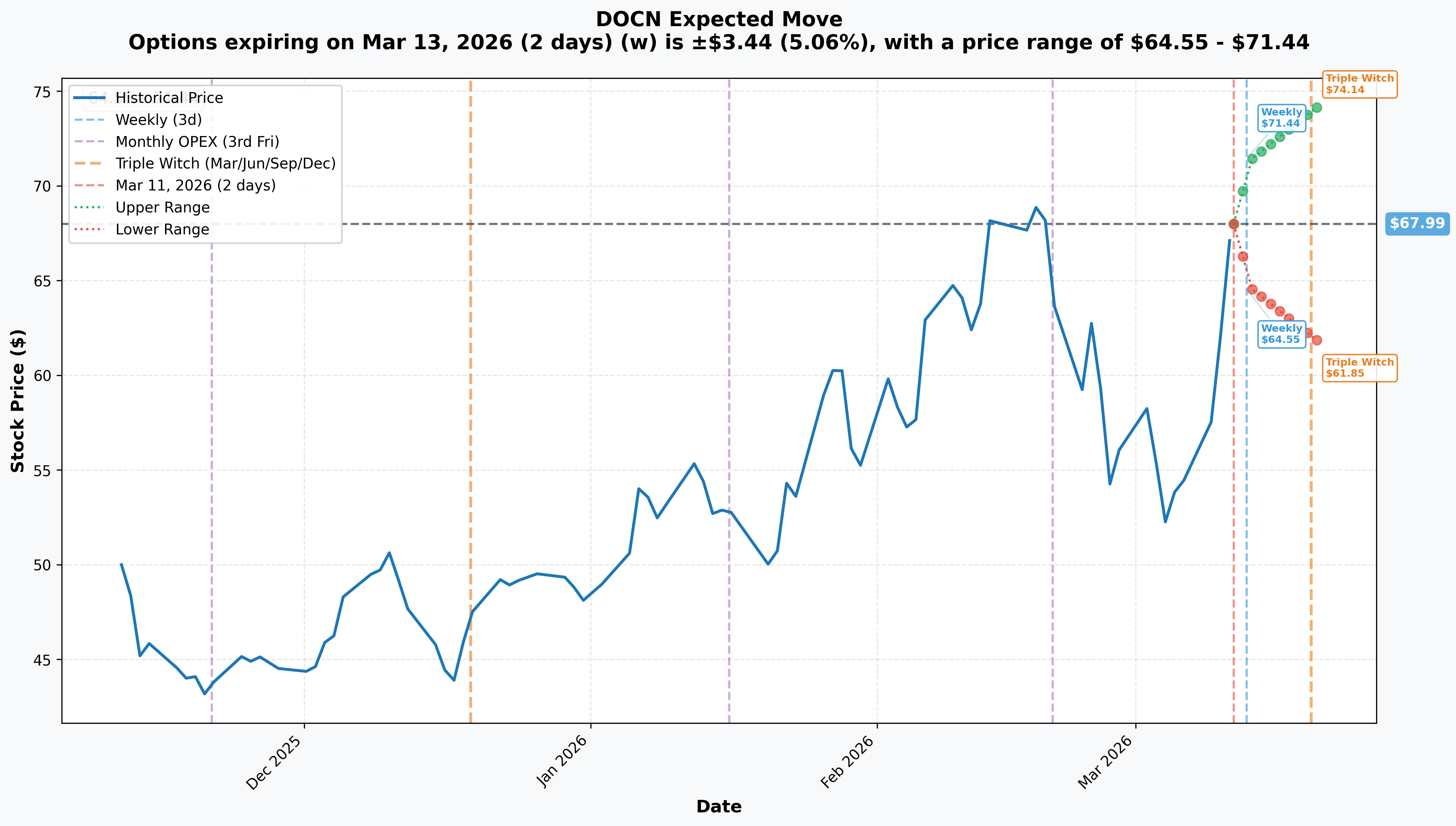

📉 Implied Move Analysis

What options are pricing in for near-term expirations:

| Timeframe | Expiry | Days Out | Implied Move | Upper Range | Lower Range |

|---|---|---|---|---|---|

| 📅 Weekly | 2026-03-13 | 2 days | ±5.1% (±$3.44) | $71.44 | $64.55 |

| 📅 Monthly OPEX | 2026-03-20 | 9 days | ±9.0% (±$6.14) | $74.14 | $61.85 |

| 📅 Triple Witch | 2026-03-20 | 9 days | ±9.0% (±$6.14) | $74.14 | $61.85 |

Translation for regular folks:

The market is pricing in a 5.1% move by Friday — so we're looking at $64.55–$71.44 as the expected range for the week. For the monthly OPEX on March 20, that widens out to a $61.85–$74.14 range (a 9% total implied move).

Notice that the monthly upper bound of $74.14 is right below the $75 gamma resistance wall. This isn't a coincidence — the options market is essentially saying "we think $74 is about as high as this goes in the next 9 days." The LEAP buyer has a different view for the next 10 months. That's the bet.

Also noteworthy: Today's +9.9% pop is itself almost exactly the full monthly implied move. The stock has front-loaded a ton of the near-term options pricing in a single session.

🎪 Catalysts

✅ Already Happened (Driving Today's Price Action)

🔥 Workato AI Migration Win (March 3, 2026) DigitalOcean announced Workato's AI Research Lab migrated to its Agentic Inference Cloud, running Llama-3.3-70B with 67% lower inference costs, 67% higher throughput, and 77% faster time-to-first-token vs. prior setup. This is the kind of real-world proof point that converts skeptics.

📊 Q4 2025 Earnings Beat (February 24, 2026) Revenue of $242.4M (+18.3% YoY), AI Customer ARR hit $120M (+150% YoY), and non-GAAP EPS came in above consensus. Management outlined a "Path to 30%" growth by 2027 — the thesis that likely triggered this LEAP trade.

📈 FY2026 Guidance Issued (February 24, 2026) $1.075B–$1.105B in revenue (+19–23% YoY) with Adjusted EBITDA margins guided 36–38%. The Street respects this guide because DOCN has been consistently beating and raising.

🖥️ AMD MI350X GPU Droplets Launch (February 19, 2026) New GPU Droplets powered by AMD Instinct MI350X went live, expanding DigitalOcean's inference cloud capacity with lower latency and larger context windows.

🤖 Analyst Upgrades (February 25, 2026) Oppenheimer raised to Outperform with an $85 target (the highest on the Street). Barclays bumped its target to $69. The consensus sits at 10 Buy / 4 Hold, average target ~$69.23.

📊 Character.AI Performance Win DigitalOcean delivered 100% throughput increase and ~50% lower cost per token for Character.ai on production inference. Two marquee AI customers validated in rapid succession.

🚀 Upcoming Catalysts (This Is What the LEAP Is Betting On)

📅 Q1 2026 Earnings (~May 2026) This is the first real test of the $1.075B+ revenue guide. Consensus expects $249M–$250M in Q1 revenue (+18–19% YoY). Key things to watch:

- AI ARR trajectory (can $120M become $150M+ by Q1?)

- Net revenue retention rate

- Progress toward $1B+ annual revenue

🖥️ AMD MI355X Liquid-Cooled Deployments (~Q2 2026) DigitalOcean's first liquid-cooled rack deployments are targeted for next quarter — designed for larger models and bigger datasets. Could unlock enterprise-scale AI inference workloads and push AI ARR above the $120M run-rate.

🚀 NVIDIA Blackwell GPU Droplet Rollout (Mid-2026) Full rollout of Blackwell B300 GPU Droplets expected mid-2026. If demand continues at current pace, new capacity could be booked out fast. Potential to add $30M–$50M+ to AI ARR by year-end and drive upward revisions to full-year guidance.

📈 Gradient Platform Expansion (Ongoing) DigitalOcean's Gradient AI platform (train, infer, build agents) is being positioned as the standard for SMBs deploying AI agents. If successful, creates a high-margin software revenue stream on top of infrastructure — which is exactly the kind of multiple expansion story that institutional investors pay up for.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst timeline, here's how the next 10 months could play out for this LEAP:

📈 Bull Case — 30% probability

Target: $80–$90

- ✅ Q1 2026 earnings crushes — AI ARR hits $150M+, guidance raised toward $1.1B+

- 🚀 Blackwell GPU Droplet rollout gets booked out within weeks, driving material upside to AI revenue

- 🤖 Additional marquee AI customer wins announced (the Workato/Character.ai playbook at scale)

- 📈 "Path to 30%" growth narrative gets more institutional buy-in — multiple expands from ~5.9x P/S to 7–8x

- 🔵 Gamma at $75 gets cleared, and $80 becomes the next magnet (implied move upper range expands)

- 📊 Consensus targets move toward $85–$90 (Oppenheimer's current high target)

LEAP P&L: Stock at $85 on Jan 15, 2027 → intrinsic value = $10.00, total profit = ~($10.00 + remaining time value) per contract. At $15.48 paid, you'd be looking at meaningful appreciation.

🎯 Base Case — 45% probability

Target: $70–$80 (gradual grind higher)

- ✅ DOCN executes in line — hits $1.075B–$1.105B revenue range, steady AI ARR growth

- 📊 Stock consolidates in the $67–$75 zone through mid-2026 as the market digests today's run

- 🎯 Mid-2026 Blackwell rollout and Q2 earnings provide the next catalyst to push through $75 gamma resistance

- 💤 Stock drifts toward $75–$80 by Q3–Q4 2026 as guidance raises materialize

- 🔑 LEAP buyer profitable if DOCN gets above ~$75 with enough time premium remaining

📉 Bear Case — 25% probability

Target: $50–$60 (gives back today's gains)

- 😰 Broader software sector continues underperforming — DOCN gets caught in the tide

- ⚠️ AI inference margins compress as GPU supply normalizes and hyperscalers undercut pricing

- 📉 Q1 2026 earnings disappoints — AI ARR growth decelerates from 150% to something lower

- 💸 Rising interest expense from refinanced floating-rate debt weighs on EPS

- 🛡️ $62.50 gamma support floor gets tested; if that cracks, $60 is next

- ❌ LEAP expires significantly out-of-the-money — most/all of the $3.9M premium erodes

💡 Trading Ideas

🛡️ Conservative: The "Ride the Wave" Stock Play

Play: Buy DOCN shares on any pullback toward gamma support

Why this works:

- 📊 The gamma floor at $62.50 is the strongest support nearby — that's where market makers mechanically step in to buy

- ✅ You own the upside through all the upcoming catalysts (Blackwell launch, Q1/Q2 earnings, MI355X deployment) without option decay eating your position

- 🎯 Analyst consensus at $69.23 average and Oppenheimer's $85 target give you defined upside scenarios

- 💰 If you've been wanting DOCN exposure, today's move has compressed the risk/reward vs. a few weeks ago — but a pullback to $62–$65 would be a better entry with gamma support beneath you

Entry: Look for $62–$65 on any pullback (3–7% below current) Risk: Below $60, gamma support thins out and the story gets harder to defend Target: $75–$85 over 6–12 months

Risk level: Moderate (stock position, no leverage) | Skill level: Beginner-friendly

⚖️ Balanced: The "LEAP Lite" — Smaller Size, Same Thesis

Play: Buy the DOCN January 2027 $75 Call — same contract as the whale trade, but sized appropriately

Structure: Buy DOCN Jan 15, 2027 $75 Call — currently ~$15.48 per contract

Why this works:

- 🎯 You're making the same directional bet as the institutional buyer — that DOCN reaches $75+ by January 2027 — but with defined risk (your max loss is the premium paid)

- ⏰ 10 months of runway captures every major catalyst: Q1 earnings, Blackwell launch, Q2 earnings, AMD MI355X deployment

- 💡 At $15.48 per contract, you control 100 shares for $1,548 vs. $6,754 to buy 100 shares outright — roughly 4.4x leverage with defined downside

- 📈 Breakeven at expiration: $75 + $15.48 = $90.48 — that's about 34% above today's spot price. Not trivial, but achievable over 10 months given the growth runway

Position sizing: Risk only 2–5% of your portfolio. This is speculative. Size accordingly. Max loss: 100% of premium paid (if DOCN is below $75 on Jan 15, 2027) Max gain: Theoretically unlimited; every dollar above $90.48 is pure profit

Risk level: Moderate-to-High (options, defined risk) | Skill level: Intermediate

🚀 Aggressive: The "Nearer-Term Ladder" — Catch the Breakout First

Play: Buy the DOCN March 20 $70 Call to play the near-term implied move breakout, and if that works, roll proceeds into the January 2027 calls

Why this could work:

- 💥 With today's +9.9% move and the monthly implied upper range at $74.14, DOCN could challenge the $70–$72 resistance zone by Triple Witch on March 20

- 🎰 Near-term calls are cheaper in dollar terms and give high leverage if the breakout continues

- 🔄 If DOCN clears $70 by OPEX, near-term calls can pay for the LEAP position with money you made on the shorter-dated trade

Why this could blow up:

- ⏰ Near-term calls have brutal theta decay — 9 days to expiration means if DOCN stalls, you lose fast

- 📉 Today's +9.9% move means implied volatility is likely elevated right now — options are expensive intraday

- 🎢 DOCN could easily pull back 3–5% after a day like today, and short-dated OTM calls would get crushed fast

Estimated P&L on March 20 $70 Calls:

- Stock to $72 by Mar 20: Calls potentially worth $2–$3 (significant gain from entry)

- Stock flat at $67–$68: Calls likely expire near worthless (high loss%)

- Stock to $65: Calls expire worthless (total loss on this leg)

This is for experienced options traders only. Not a set-it-and-forget-it trade.

Risk level: High (short-dated, leveraged, high decay) | Skill level: Advanced

⚠️ Risk Factors

Don't let the excitement of a $3.9M whale trade cloud your judgment on the real risks:

-

💸 DOCN just ran +9.9% in a single day — today's Workato news is a great catalyst, but the stock may need time to digest this move before the next leg up. Chasing a gap-up day is a classic way to get burned. Patience may be rewarded.

-

🏦 Balance sheet complexity: DigitalOcean carries significant debt after its refinancing. The shift from 0% convertible notes to floating-rate Term Loans adds meaningful interest expense. Negative shareholders' equity is a structural quirk that bears love to point at. It's not fatal, but it does matter if rates stay high.

-

⚖️ Scale vs. hyperscalers: AWS, Azure, and Google Cloud are all pushing downmarket, and they have unlimited capex. DigitalOcean's competitive moat is simplicity and pricing for SMBs — but that moat gets narrower if hyperscalers decide to compete aggressively on price.

-

💻 AI revenue concentration risk: AI customer ARR of $120M is growing fast but represents only ~13% of total ARR. Character.ai and Workato are marquee wins, but losing a major customer would be felt. The inference business is still relatively early-stage.

-

🛡️ GPU pricing pressure: As NVIDIA and AMD expand supply, the premium pricing that early inference cloud providers command may compress. GPU rental margins could narrow if demand normalizes.

-

📉 Broader software sector headwinds: Software as a sector is down ~24% in 2026. DOCN has bucked the trend (+12% before today), but macro pressure on growth multiples is real. If rates stay high and growth stocks continue to lag, even a good story doesn't guarantee the stock goes up.

-

🚨 Insider selling: The CFO and CAO both sold shares in early March 2026 via pre-planned 10b5-1 plans. These were scheduled well in advance and not discretionary signals, but worth noting. The one genuine positive: Director Adelman was a net buyer in the period.

-

📅 LEAP breakeven is a stretch: At $15.48 premium, this call needs DOCN at $90.48 by January 15, 2027 to break even at expiration. That's a 34% rally from today. Possible? Yes. Guaranteed? Absolutely not.

🎯 The Bottom Line

Here's the deal: Someone spent $3.9M this morning on a 10-month call betting that DigitalOcean's AI infrastructure pivot is the real deal — and that the stock can tack on another 11%+ from today's already-elevated price. This isn't a blind speculative bet. It's a thesis-driven LEAP backed by accelerating AI ARR (+150% YoY), a credible "Path to 30%" growth roadmap, marquee customer wins (Character.ai, Workato), and a pipeline of GPU capacity expansions that could drive meaningful guidance raises through 2026.

What to do if you already own DOCN:

- ✅ Today's move has been a great gift — consider locking in some gains near the $70–$72 gamma resistance zone

- 📊 If you're holding for the long-term AI thesis, keep an eye on the $62.50 gamma support as your defense line — that's where the market structure says buyers will step in on dips

- ⏰ Mark your calendar for Q1 2026 earnings (~May 2026) — that's the next major checkpoint on whether AI ARR is accelerating the way the guidance implies

If you're watching from the sidelines:

- 👀 Don't chase today's +9.9% gap-up. A pullback to $62–$65 would offer a much cleaner risk/reward setup — gamma support below, full catalyst runway ahead

- 📅 Bigger picture: Blackwell GPU rollout (mid-2026) and AMD MI355X deployments (Q2 2026) are the catalysts that could move the needle enough to clear the $75 gamma wall the LEAP buyer is targeting

If you're bearish:

- 🐻 The bear case for DOCN centers on debt load, hyperscaler competition, and margin compression risk. Those are legitimate concerns.

- 📊 If the broader software sector continues to underperform and DOCN fails to hold $62.50 support, a move back toward $57–$60 is plausible

Key dates to mark:

- 📅 March 13 — Weekly OPEX (implied range: $64.55–$71.44)

- 📅 March 20 — Monthly Triple Witch OPEX (implied range: $61.85–$74.14)

- 📅 ~May 2026 — Q1 2026 earnings report — first real test of the $1.075B guidance

- 📅 Q2 2026 — AMD MI355X liquid-cooled deployments go live

- 📅 Mid-2026 — NVIDIA Blackwell GPU Droplet full rollout

- 📅 January 15, 2027 — This $3.9M LEAP trade expires

Final verdict: DigitalOcean's AI inference pivot is generating real results — the numbers aren't made-up hype, they're showing up in revenue and AI ARR. The $3.9M LEAP reflects genuine institutional conviction that the 2026–2027 growth story has legs. But the stock has already run hard, today's gap-up adds short-term froth, and the path to $90 breakeven by January 2027 requires continued strong execution. This is a name worth watching closely — with patience.

Don't FOMO into a 10% gap-up day. Build your conviction first. 💪

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. The unusual options activity described reflects a single trade and does not imply the trade will be profitable or that you should replicate it. The Z-score of EXTREMELY_UNUSUAL reflects this contract's volume relative to its historical open interest — it identifies that this is statistically rare flow for this specific contract, not a prediction of future price movement. LEAP options can expire worthless and you can lose 100% of your invested premium. Always do your own research and consider consulting a licensed financial advisor before making any investment decisions. DigitalOcean Holdings is subject to competitive, macroeconomic, and execution risks described above that could cause the stock to decline materially from current levels.

About DigitalOcean Holdings (DOCN): DigitalOcean Holdings, Inc. provides on-demand infrastructure and platform tools for developers, startups, and SMBs through its cloud computing platform, increasingly including AI inference and agentic workloads through its Gradient / Agentic Inference Cloud offering. Market cap approximately $5.7 billion, listed on NYSE.