🐋 EWZ $7.4M Covered Call Mega-Sell - Institutional Money Caps Upside While Collecting Premium!

📅 February 25, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold 102,000 call contracts on EWZ at the $45 strike for $7.4 MILLION in premium - that's 10.2 million shares of exposure (~$403M notional) on the Brazil ETF that just hit a new 52-week high. This is almost certainly a massive covered call write by an institution sitting on a huge long EWZ position, capping their upside at $45 (+13.9% above spot) while pocketing $7.4M in income over the next 4 months. With rate cuts imminent in Brazil and record EM inflows, this whale is saying: "I love the rally, but I'll take the cash."

📊 ETF Overview

iShares MSCI Brazil ETF (EWZ) is the go-to ETF for getting exposure to Brazil's equity market:

- 🌎 What it tracks: MSCI Brazil 25/50 Index - the 54 largest and most liquid Brazilian companies

- 💰 AUM: ~$9.3-9.6B

- 🏢 Sector Mix: Financials (Nu, Itau, Bradesco), Energy (Petrobras), Mining (Vale), Industrials (WEG)

- 📈 Exchange: NYSE Arca

- 📊 Current Price: ~$39.51, hitting a new 52-week high of $39.69 today

- 🇧🇷 Key Story: Brazil is the biggest beneficiary of the current US tariff regime, with a rate-cutting cycle about to begin, record EM inflows, and BRL strength at 2-year highs

Top Holdings:

- 🏦 Nu Holdings (NU) - 11.25% - Brazil's fintech giant with 127M customers and 42% YoY revenue growth

- ⛏️ Vale (VALE) - 10.79% - Iron ore powerhouse at 7-year production highs

- 🏦 Itau Unibanco (ITUB) - 8.87% - Brazil's largest company by market cap

- 🛢️ Petrobras (PETR4 + PETR3) - 11.36% combined - Oil giant with 15.5% total dividend yield

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:31:28 | EWZ | MID | SELL | CALL $45 | 2026-06-18 | $7.4M | $45 | 102,000 | - | 102,000 | $39.51 | $0.73 | EWZ20260618C45 |

🤓 What This Actually Means

Let me break this down in plain English:

- 💸 $7.4 million collected: 102,000 contracts at $0.73 each ($0.73 x 100 shares x 102,000 = ~$7.4M in premium income)

- 📉 This is a SELL, not a buy: Classified as STO (Sell-to-Open) - the trader is opening a brand new short call position

- 📊 102,000 contracts = 10.2 MILLION shares of exposure - at $39.51 per share, that's roughly $403M in underlying notional

- 📈 Strike $45 is 13.9% above current price - this is well out-of-the-money, giving the seller a big cushion before they get called away

- ⏰ June 18 expiration (Triple Witch) - approximately 4 months out, capturing significant time decay

- 🤝 MID fill - executed at the midpoint, classic institutional execution quality

- 🎯 Breakeven for the seller: The stock needs to rally above $45.73 ($45 strike + $0.73 premium) before this trade loses money

What's the thesis here?

This is textbook institutional income generation - almost certainly a covered call strategy. Here's the logic: a large fund (think pension, sovereign wealth, or EM-focused asset manager) already owns millions of EWZ shares. They're bullish enough to hold the position through Brazil's rate-cutting cycle, but they don't think EWZ will rally past $45 by June. So they sell calls against their position, collecting $7.4M in premium that they keep no matter what happens.

Why $45? Look at the math: $45 is 13.9% above the current price of $39.51. The options market is only pricing a ~5.1% move by March Triple Witch - and even extrapolating to June, $45 is a stretch. The seller is essentially saying: "I'll take a 13.9% cap on my upside in exchange for guaranteed $7.4M income." That's a very calculated, very institutional trade.

Why June Triple Witch specifically? Triple Witch (third Friday of March, June, September, December) is when index options, equity options, and futures all expire simultaneously. Liquidity is deepest, spreads are tightest, and settlement is most efficient for these mega-sized institutional trades. Plus, June sits right before election-season volatility ramps up in Brazil (October 4 first round) - clever timing.

📈 Technical Setup / Chart Check-Up

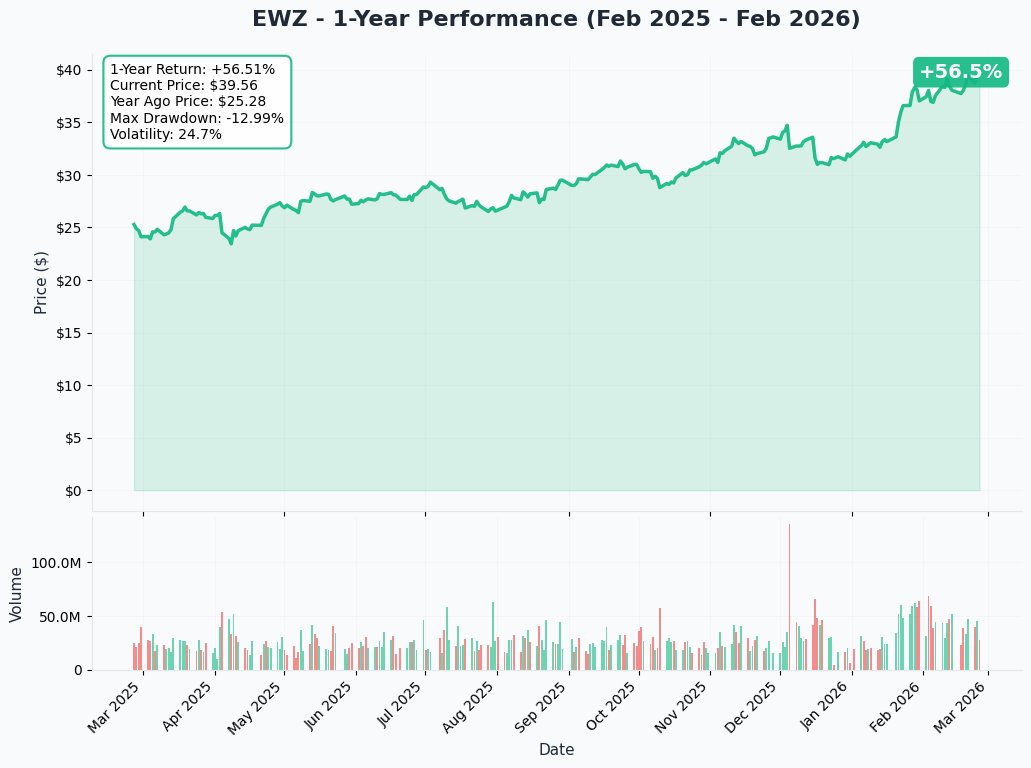

YTD Performance

EWZ is up +16.5% YTD and just hit a new 52-week high of $39.69 today. The chart tells a powerful emerging market recovery story:

- 🚀 Massive rally from 52-week low: Up from $23.05 low to $39.69 - a stunning +72% recovery

- 📈 Well above moving averages: Trading 13.1% above the 50-day SMA ($35.03) and 22.7% above the 200-day SMA ($32.29) per Markets Daily

- 💪 Record fund inflows: $3.46B in 1-year net inflows - representing 37% of total AUM

- 🇧🇷 Ibovespa at record highs: The underlying Brazilian index hit 191,519 points - up 53.5% YoY

- 💵 BRL tailwind: The Real at 5.15/USD is the strongest since May 2024, boosting USD-denominated returns

Key takeaway: EWZ is in a strong uptrend with momentum, flows, and macro all aligned. The covered call seller isn't betting against this rally - they're harvesting income from it while accepting a cap at $45. That cap is 13.9% overhead, which is generous enough to still participate in continued upside.

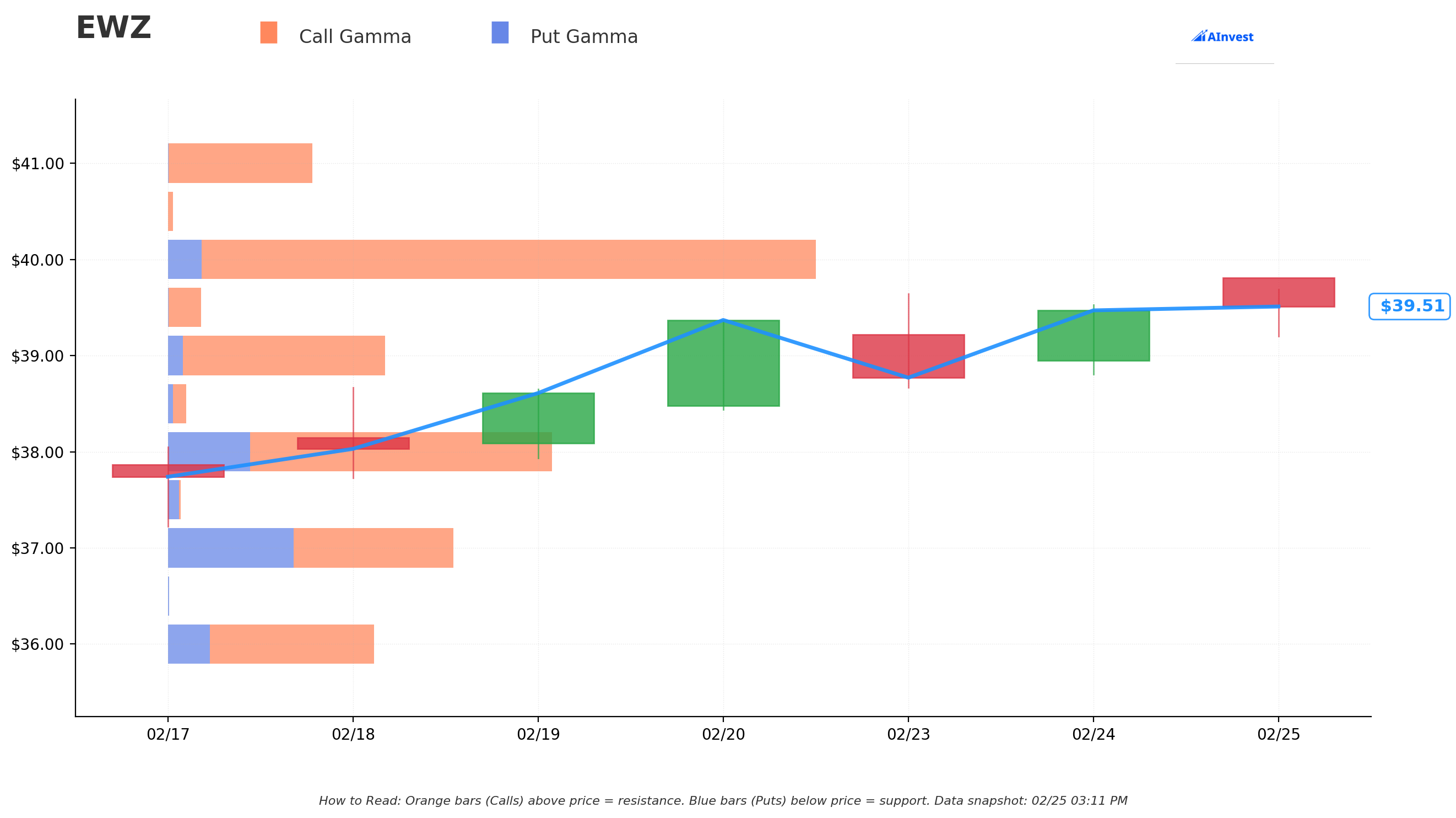

Gamma-Based Support & Resistance Analysis

Current Price: $39.50

The gamma exposure map reveals where options market makers have concentrated positions, creating natural price magnets and barriers:

🔵 Support Levels (Put Gamma Below Price):

- $39 - Nearest support with 51.4B total gamma exposure (just 1.3% below - tight floor!)

- $38 - Strongest structural support with 91.4B total gamma (3.8% below - this is the LINE IN THE SAND)

- $37 - Secondary support at 68.5B gamma (6.3% below)

- $36 - Extended support at 50.1B gamma (8.9% below)

- $35 - Deep support at 39.3B gamma (11.4% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $40 - MASSIVE resistance at 152.8B total gamma (just 1.3% above - the big round-number magnet!)

- $41 - Lighter resistance at 34.0B gamma (3.8% above)

- $42 - Strong resistance at 101.2B gamma (6.3% above)

- $45 - The sold strike! 52.0B gamma at 13.9% above current price

What this means for traders: EWZ is sandwiched between massive $40 resistance overhead and $38 support below. The $40 level is the near-term battlefield - if EWZ can push through that 152.8B gamma wall, the path opens to $42. But the call seller at $45 has chosen a strike that sits above ALL major gamma resistance levels, giving them a substantial cushion. The seller is essentially betting that all this gamma overhead will slow any rally before it reaches $45.

Net GEX Bias: Bullish (713B total call gamma vs 129B total put gamma) - dealer positioning is overwhelmingly bullish, suggesting the floor is well-supported and dips should be bought.

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 27 - 2 days): ±1.81% (±$0.71) --> Range: $38.80 - $40.22

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 23 days): ±5.13% (±$2.03) --> Range: $37.48 - $41.54

- 📅 June 18 OPEX (THIS TRADE!): Extrapolating the vol surface, the expected range extends roughly to $35 - $44 (approximately ±11-12% over ~4 months)

Translation: The options market expects EWZ could move anywhere from about $35 to $44 by the June 18 expiration. The $45 strike on this call sell sits above that implied upper range - meaning the market views $45 as unlikely by June. The seller has the probabilities on their side.

Key insight: The monthly implied move upper range is $41.54 - that's the highest the market expects EWZ to go by March 20. Even by June with more time, $45 is a stretch. This validates the covered call seller's thesis: collect $7.4M in premium because the odds of getting called away at $45 are relatively low (probably 15-20% based on the delta).

🎪 Catalysts

🔥 Upcoming Catalysts

Copom Rate Cut Decision - March 17-18, 2026 🏦

This is THE catalyst for Brazilian equities right now. BCB Governor Galipolo signaled rate cuts are likely to begin at the March meeting:

- 📉 Selic at 15% - highest since July 2006 - has been the primary headwind for Brazilian stocks

- 🎯 Market expects a 50 bps cut to 14.50% as the first step in an easing cycle

- 📊 Year-end consensus: Selic at 12.25% (-275 bps total in 2026)

- 💪 Capital Economics argues cuts could be deeper than most expect

- 🚀 Rate cuts = lower CDI yields = domestic rotation from fixed income into equities = bullish EWZ

Q1 2026 Earnings Season - March/April 2026 📊

Key EWZ holdings reporting:

- 🏦 Nu Holdings: Watch for credit growth and ROE trajectory toward 30-35% target

- ⛏️ Vale: Q1 production data and iron ore pricing guidance (2026 target: 335-345M mt)

- 🛢️ Petrobras: Fuel pricing policy and dividend guidance (next payment date March 27)

- 🏦 Itau: Credit growth execution against cautious 5.5-9.5% guidance

Subsequent Copom Meetings - May, July, August 2026 🏦

- Each meeting expected to deliver another 50 bps cut

- The cumulative easing effect on equity multiples compounds with each cut

- By June 18 (this trade's expiration), we should have 2-3 rate cuts under our belt

Brazilian Presidential Election - October 4, 2026 🗳️

- Lula leads Bolsonaro 36% vs 23% in first-round polling, with a projected 45% to 38% runoff margin

- Campaign season heats up in August - this trade expires BEFORE peak election volatility

- Smart timing by the call seller: collect premium during the calm period, avoid the election storm

✅ Recent Catalysts (Already Happened)

Supreme Court IEEPA Tariff Ruling - February 20, 2026 ⚖️

The game-changer. The US Supreme Court ruled 6-3 that IEEPA does not authorize presidential tariffs, invalidating the punitive 40% + 10% tariffs on Brazil:

- 📉 Brazil's trade-weighted tariff rate plunged 13.6 percentage points overnight

- 🇧🇷 46% of Brazilian exports to the US now face zero additional tariffs

- ✈️ Brazil hailed zero tariffs on aircraft exports (Embraer)

- ⚠️ A new 15% global tariff under Section 122 replaced the struck-down tariffs - but net effect is hugely positive for Brazil

Record EM Capital Inflows - 18-Week Streak 💰

- Emerging market ETFs attracted $50.6B over an 18-week streak

- January 2026 alone saw $20.5B in EM equity ETF inflows - an all-time monthly record

- EWZ specifically attracted $3.46B in 1-year net inflows - 37% of AUM

- EM inflows are 238% above the historical 80th percentile - extraordinary demand

BRL Strength - 2-Year High at 5.15/USD 💵

- Brazilian Real appreciated 11.22% over 12 months against the dollar

- Driven by the massive carry trade spread from 15% Selic, tariff relief, and a record January trade surplus of $4.34B (+85.8% YoY)

- BRL strength is a double tailwind: it boosts EWZ's USD-denominated NAV AND signals continued foreign capital flows into Brazil

Ibovespa Record High - February 25, 2026 📈

- Brazilian benchmark hit 191,519 points - an all-time record, up 53.5% YoY

- Forward P/E at 9.25x remains cheap relative to EM peers despite the rally

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst calendar, and the specifics of this covered call trade, here are the scenarios through the June 18, 2026 expiration:

📈 Bull Case (20% probability)

Target: $44-$48

How we get there:

- 🚀 Copom delivers aggressive rate cuts (75 bps in March instead of 50 bps), signaling deeper easing cycle

- 💰 EM inflows accelerate beyond the already-record pace, pushing EWZ above $40 gamma resistance

- 💵 BRL continues strengthening below 5.00/USD, amplifying USD-denominated returns

- 📈 Nu Holdings and Itau deliver blowout earnings showing accelerating credit growth

- 🛢️ Oil prices stay elevated ($70+ Brent) supporting Petrobras

- ✅ Break above $40 gamma wall triggers technical chase to $42, then momentum toward $45

Covered call trade P&L at $45: Seller keeps the full $7.4M premium but gets called away at $45. If their cost basis is near the 200-day SMA (~$32.29), total profit = ($45 - $32.29 + $0.73) x 10.2M shares = ~$137M total return. Not bad at all, but they cap out and miss any further upside.

Covered call trade P&L at $48: Called away at $45, missing the rally from $45 to $48. Opportunity cost of ~$3/share on 10.2M shares = ~$30.6M left on the table. Still hugely profitable, just capped.

This is the scenario where the call seller "loses" - not by losing money, but by capping their upside. They still walk away very happy.

🎯 Base Case (55% probability)

Target: $38-$43 range

Most likely scenario:

- ✅ Copom begins cutting rates in March as expected - buy-the-rumor, sell-the-news reaction

- 📊 EWZ oscillates between $38 gamma support and $42 gamma resistance through spring

- 🔄 Rate-cutting cycle proceeds methodically but doesn't surprise to the upside

- ⚖️ Election uncertainty starts building in Q2, capping enthusiasm

- 💵 BRL stabilizes in the 5.00-5.30 range as rate cuts narrow the carry advantage

- 💤 Commodity prices drift lower per consensus (iron ore toward $94/t) but don't crash

- 📈 ETF grinds between $38-$43, never seriously threatening $45

Covered call trade P&L at $41: Seller keeps the full $7.4M premium. Calls expire worthless (OTM). ETF position gains ~$1.50/share. Total income: $7.4M premium + ~$15.3M unrealized gain = $22.7M. Perfect outcome for the seller.

Covered call trade P&L at $39: Seller keeps the full $7.4M premium. ETF position is roughly flat. $7.4M in pure premium income. Still a clean win.

This is the sweet spot for a covered call writer. The stock goes sideways or grinds modestly higher, calls expire worthless, and they pocket the full premium. In the base case, this $7.4M is essentially free money.

📉 Bear Case (25% probability)

Target: $33-$37

What could go wrong:

- 😰 Brazil's debt-to-GDP trajectory toward 95% triggers a fiscal scare

- 🛢️ Oil falls toward EIA's $58/bbl Brent forecast, crushing Petrobras (11.36% of EWZ)

- ⛏️ Iron ore drops to $90/t on Simandou mine launch, dragging Vale (10.79% of EWZ)

- 💸 BRL carry trade unwinds as rate cuts narrow yield advantage - currency drops back toward 5.50+

- 📉 Election-year spending temptation derails fiscal consolidation

- 🌏 China slowdown contagion hits commodity exporters (Brazil ships 37% of exports to China)

- 📊 Break below $38 gamma support (91.4B) triggers cascade toward $35-$36

Covered call trade P&L at $35: Seller keeps the full $7.4M premium, partially offsetting the ~$4.50/share loss on the underlying. The premium collected provides a $0.73/share cushion on 10.2M shares. Net loss on the position is reduced by $7.4M thanks to the premium. This is exactly why institutions sell covered calls - the premium provides downside protection.

In this scenario, the covered call seller is glad they sold the calls. The $7.4M cushion makes a painful drawdown slightly less painful.

💡 Trading Ideas

🛡️ Conservative: "Copy the Whale" - Covered Call Income Strategy

Play: Buy 100 shares of EWZ at ~$39.50, sell 1 June 18 $45 call for ~$0.73

Why this works:

- 💰 Collect ~$0.73/share in premium - that's a 1.8% yield in 4 months (5.6% annualized) on top of any price appreciation

- 🛡️ Downside cushion: Your effective cost basis drops from $39.51 to $38.78 - you absorb a 1.8% pullback before taking a loss

- 📈 Upside to $45: You participate in any rally up to $45 (+13.9%) PLUS the premium

- ⏰ Time is your friend: Theta decay works for you every single day as the $0.73 erodes

- 🎯 Max return if called away at $45: ($45 - $39.51 + $0.73) / $39.51 = 15.7% in 4 months

- 🏦 Mirrors the exact same strategy the $7.4M whale is running - just at retail scale

Position sizing: Allocate 5-10% of portfolio. 100 shares = ~$3,950 invested, collect ~$73 in premium. Start small and scale up if the thesis plays out.

Risk level: Low-Moderate (you own the stock, so you're exposed to downside below $38.78) | Skill level: Beginner-friendly

⚖️ Balanced: "Brazil Rate Cut Play" - Bull Call Spread

Play: Buy EWZ June 18 $40 calls, sell June 18 $43 calls

Structure: $40/$43 bull call spread, 4 months to expiration

Why this works:

- 🎯 Targets the $40-$43 zone where gamma resistance and the base case range overlap

- 💸 Defined risk: you can only lose the net debit paid (estimated ~$1.00-$1.30 per spread)

- 💰 Max profit: $3.00 per spread minus debit (~$1.70-$2.00 gain per spread) if EWZ above $43 at expiry

- 📈 The $40 strike is only 1.3% away - easy to get in-the-money on the first Copom rate cut

- ⏰ Captures 2-3 rate cut catalysts before expiration

- 🇧🇷 Benefits from the Supreme Court tariff ruling tailwind and continued EM inflows

- ⚖️ Risk/reward roughly 1.5:1 to 2:1

Position sizing: 20-50 spreads at ~$1.15 each = $2,300-$5,750 risk for $3,400-$8,500 max profit.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: "Rate Cut Rocket" - June $42 Calls

Play: Buy EWZ June 18, 2026 $42 calls outright

Why this works (and why it's risky):

- 💥 Directly bets on EWZ breaking through the $40 and $42 gamma resistance levels as rate cuts pile up

- 📊 $42 strike aligns with the 101.2B gamma level - a natural magnet once breached

- ⏰ 4 months captures March, May, and possibly July Copom rate cuts

- 🚀 If EWZ hits $45 (the whale's sold strike), these calls would be worth ~$3.00, roughly tripling a ~$0.90-$1.10 entry

- 📈 Ibovespa at 9.25x forward P/E has room for multiple expansion in a rate-cutting environment

- 🌎 Record EM inflows provide sustained demand

Why it could blow up:

- 💸 $42 strike is 6.3% above current price - needs a meaningful push higher

- ⚠️ The $40 gamma wall at 152.8B is the STRONGEST level on the entire board - getting through it is not guaranteed

- 📉 If EWZ stays below $42 by June expiration, you lose everything

- ⛏️ Iron ore weakness in H2 2026 could drag Vale and the broader index

- 🗳️ Election campaign noise could spook investors in the weeks before expiration

- 💵 BRL reversal from rate cuts narrowing the carry trade would create a headwind

Position sizing: Risk ONLY what you can afford to lose completely. 20-50 contracts at ~$1.00 each = $2,000-$5,000 at risk.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📈 EWZ is technically stretched: Trading 13.1% above its 50-day SMA and 22.7% above its 200-day SMA at a 52-week high. That's a lot of premium over the moving averages. A healthy pullback to the 50-day SMA at $35.03 would represent an -11.3% decline from current levels. After a 72% rally from the 52-week low, mean reversion risk is real.

-

🇧🇷 Fiscal sustainability is Brazil's Achilles' heel: Gross debt projected at 95% of GDP in 2026 - elevated for an emerging market. The 0.25% primary surplus target is widely seen as unachievable in an election year. The Lula administration has focused on revenue increases rather than spending cuts, weakening its own fiscal framework. A fiscal crisis would send BRL and EWZ sharply lower simultaneously.

-

⛏️ Commodity price headwinds for 22% of EWZ: Vale (10.79%) and Petrobras (11.36%) together make up over a fifth of the fund. Iron ore consensus for 2026 is $94/t (-7% vs 2025), with the Simandou mine threatening $90/t in H2. Oil could fall toward EIA's $58/bbl Brent forecast if geopolitical tensions ease. Both would compress earnings for EWZ's biggest holdings.

-

🗳️ Election-year volatility ahead: The October 4 first round creates months of rising political uncertainty. Pre-election spending temptation could derail fiscal consolidation. Even Itau's management cited election-year volatility as a factor in their cautious 2026 credit guidance.

-

💵 BRL reversal risk from rate cuts: The Real's strength is partly driven by the 15% Selic carry trade. As rate cuts proceed toward 12.25% year-end target, the carry advantage narrows. If BRL weakens from 5.15 back toward 5.50-6.00, EWZ faces a headwind where there was a tailwind. The 11.22% BRL appreciation over 12 months may already price in much of the good news.

-

🇨🇳 China dependency: Brazil ships 37% of exports to China. Chinese steel demand stagnation is the primary driver of iron ore price weakness. Any China hard-landing scenario would simultaneously crush Vale, soy exporters, and indirectly Petrobras - hitting multiple EWZ top holdings at once.

-

🏗️ Concentration risk: The top 3 holdings (Nu, Vale, Itau) account for >30% of fund weight. Petrobras common + preferred combined at 11.36% is effectively the largest single-company exposure. A bad quarter from any one of these names can drag the entire ETF.

-

🌍 EM flow reversal risk: The 18-week inflow streak at $50.6B is 238% above the historical 80th percentile. Flows this far above trend are inherently unsustainable. A reversal in global EM sentiment - triggered by a dollar rally, US recession fears, or geopolitical shock - would create a crowded exit problem.

🎯 The Bottom Line

Here's the deal: An institution just collected $7.4 MILLION selling 102,000 June $45 calls on EWZ - and the logic is straightforward. EWZ has rallied 72% from its 52-week low, just hit a new high, and is trading well above every major moving average. The good news (tariff relief, rate cuts, EM inflows, strong BRL) is largely priced in at $39.51. Can EWZ get to $45 by June? It's possible, but it requires breaking through four gamma resistance levels ($40, $41, $42, $45) while already stretched above moving averages during an election year with commodity headwinds building.

What this trade tells us:

- 🎯 Smart money sees limited upside beyond 13.9% from here through mid-June

- 💰 They prefer collecting $7.4M in certain income over chasing a further rally

- ⚖️ The $45 strike choice (far OTM, above all major gamma levels) signals confidence that the rally moderates - not that it reverses

- ⏰ The June 18 expiration captures the initial rate cuts but expires BEFORE peak election volatility - clever timing

This is NOT a bearish signal - it's an "the rally has been great, now let me get paid to wait" signal.

If you're bullish on EWZ:

- ✅ Consider a covered call overlay like the institutional trade - collect premium while holding shares

- 📊 Watch the $40 gamma resistance level closely - a sustained break opens the door to $42-$43

- 📅 Mark March 17-18 (Copom rate decision) as the next major catalyst

- 🎯 Use the $38 gamma support (91.4B) as your risk management line

If you're watching from the sidelines:

- ⏰ A pullback to $35-$37 (near the 50-day SMA at $35.03) would offer a much better entry

- 📈 The rate-cutting cycle has barely begun - there will be opportunities to participate at better prices

- 🇧🇷 Long-term thesis remains intact: rate cuts from 15% to 12%, cheap forward P/E of 9.25x, tariff relief, record inflows

- ⚠️ But buying after a 72% rally at all-time highs is chasing - and the covered call seller just told you they think the easy money is behind us

If you're cautious:

- 📊 First support at $39, major floor at $38 (91.4B gamma), deeper support at $36-$37

- 🛡️ Consider mimicking the whale: own EWZ shares and sell covered calls for income while staying protected by the premium cushion

- 📉 A break below $38 gamma support would change the technical picture significantly

- 🗳️ Keep position sizes moderate ahead of October 4 election risk

Key dates to mark:

- 📅 February 27, 2026 - Weekly OPEX (implied range $38.80 - $40.22)

- 📅 March 17-18, 2026 - Copom meeting (expected first rate cut from 15% to 14.50%)

- 📅 March 20, 2026 - Monthly OPEX / Triple Witch (implied range $37.48 - $41.54)

- 📅 March 27, 2026 - Petrobras dividend payment date

- 📅 May 2026 - Second Copom rate cut expected + Q1 earnings season

- 📅 June 18, 2026 - THIS TRADE EXPIRES - Triple Witch, moment of truth for the $7.4M covered call

- 📅 October 4, 2026 - Brazilian presidential election first round

Final verdict: This $7.4M covered call sale is a masterclass in institutional income generation. The seller is sitting on a massive EWZ position that's already up big, riding the Brazil rate-cut and tariff-relief tailwinds, and now harvesting premium at a strike that's almost certainly safe. For retail traders, the lesson is clear: you don't have to bet on explosive moves to make money in options. Sometimes the smartest play is the boring one - sell premium, collect income, and let the probabilities work in your favor. If you're bullish on Brazil (and the macro setup is genuinely compelling right now), consider playing this through defined-risk spreads or covered calls rather than chasing at 52-week highs.

The whale collected $7.4M for promising to sell at $45. That's not a bet against Brazil - it's a bet on patience and discipline. Follow the smart money. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Selling calls (even covered) limits your upside potential, and naked calls carry unlimited risk. ETFs are subject to currency risk, emerging market risk, and concentration risk. Always do your own research and consider consulting a licensed financial advisor before trading.

About iShares MSCI Brazil ETF (EWZ): The iShares MSCI Brazil ETF tracks the MSCI Brazil 25/50 Index, providing exposure to large and mid-cap Brazilian equities across financials, energy, mining, and consumer sectors. With 54 holdings and ~$9.3B in assets under management, it is the most liquid and widely-traded vehicle for gaining exposure to the Brazilian equity market, listed on NYSE Arca with an expense ratio of 0.59%.