🦅 GTLB: $20M Deep ITM Put Sale - Institutional Player Bets on GitLab's Floor!

📅 March 12, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just SOLD $20 MILLION worth of deep in-the-money puts on GitLab this afternoon, collecting premium on 21,372 contracts of the $27.5 strike expiring January 2028! With GTLB trading at $22.77 — down roughly 39% year-to-date after a brutal post-earnings selloff — this institutional player is essentially writing a 2-year lease on the stock near all-time lows. Translation: Big money just committed $20M in premium to bet that GTLB doesn't stay this cheap for long.

📊 Company Overview

GitLab Inc. (GTLB) is the AI-powered DevSecOps platform competing to own the entire software development lifecycle in one application:

- Market Cap: ~$3.94 Billion (NASDAQ: GTLB)

- Industry: Services — Prepackaged Software

- Current Price: $22.77 (near 52-week low of $22.78)

- Primary Business: Integrated DevSecOps platform (source code management, CI/CD, security scanning, project management) targeting enterprise and regulated-industry customers. Competes head-to-head with Microsoft's GitHub + Copilot and Atlassian's toolchain, with a key differentiator being self-managed deployment for governments and financial institutions that cannot use public cloud SaaS.

GitLab crossed the $1 billion ARR milestone in Q4 FY2026 (reported March 3, 2026), yet the stock collapsed ~24.8% in February and sits near all-time lows as investors wrestle with a guided revenue growth deceleration from 26% to 15-17% in FY2027.

💰 The Option Flow Breakdown

📊 What Just Happened — The Tape (March 12, 2026 @ 14:12:37)

| Field | Detail |

|---|---|

| Time | 14:12:37 |

| Symbol | GTLB |

| Side | BID |

| Buy/Sell | SELL |

| Call/Put | PUT |

| Expiration | 2028-01-21 |

| Premium | $20M |

| Strike | $27.50 |

| Volume | 45,000 |

| OI | 7 |

| Size | 21,372 |

| Spot | $22.77 |

| Option Price | $9.30 |

| Option Symbol | GTLB20280121P27.5 |

| Strategy | Short Put (STO — Sell to Open) |

| OI Classification | STO (opening position) — Vol/OI ratio ~6,428x, EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a Short Put / Sell to Open — the institution SOLD 21,372 put contracts at the $27.50 strike with the stock trading at $22.77. Let that sink in: the strike is $4.73 above the current stock price, making these deep in-the-money puts.

Here's what actually happened and why it matters:

- 💸 $20M in premium collected: At $9.30 per contract × 21,372 contracts × 100 shares = roughly $20M in cash received upfront

- 📍 Strike above the stock price: The $27.50 strike with GTLB at $22.77 means these puts are ~20.7% in-the-money — this is NOT a far out-of-the-money lottery bet, it's a high-conviction structural position

- 🗓️ Nearly 2 years of runway: The 2028-01-21 expiration gives this institution roughly 22 months before the bet is settled

- 🏦 Effective cost basis: The seller collected $9.30, so if assigned shares at $27.50, their true cost basis is $27.50 - $9.30 = $18.20 per share — a 20% discount to today's already-beaten-down price

- 📊 Unusualness: Prior OI on this contract was just 7. Volume hit 45,000 on the day with a single block of 21,372 contracts. That's roughly ~6,400x the prior open interest — you'd typically see a trade of this character fewer than a handful of times per year on any single name

Two ways to read this trade:

Reading #1 — Cash-Secured or Covered Put Write: The institution already owns GTLB shares (or cash-secures the obligation) and is writing puts to generate $20M income while holding the position. They are FINE being assigned additional shares at $27.50 because their blended cost after the premium is $18.20 — which would represent a new multi-year low.

Reading #2 — Naked Premium Collection: The institution simply believes GTLB will not see $27.50 by January 2028 and collected $20M to express that view. The breakeven for the seller is $27.50 - $9.30 = $18.20 — meaning GTLB would have to fall another 20% from all-time lows before this position starts losing money.

Either way, the message is the same: sophisticated money at scale just bet $20M that $18.20 is a floor for GTLB over the next two years.

📈 Technical Setup / Chart Check-Up

YTD Performance

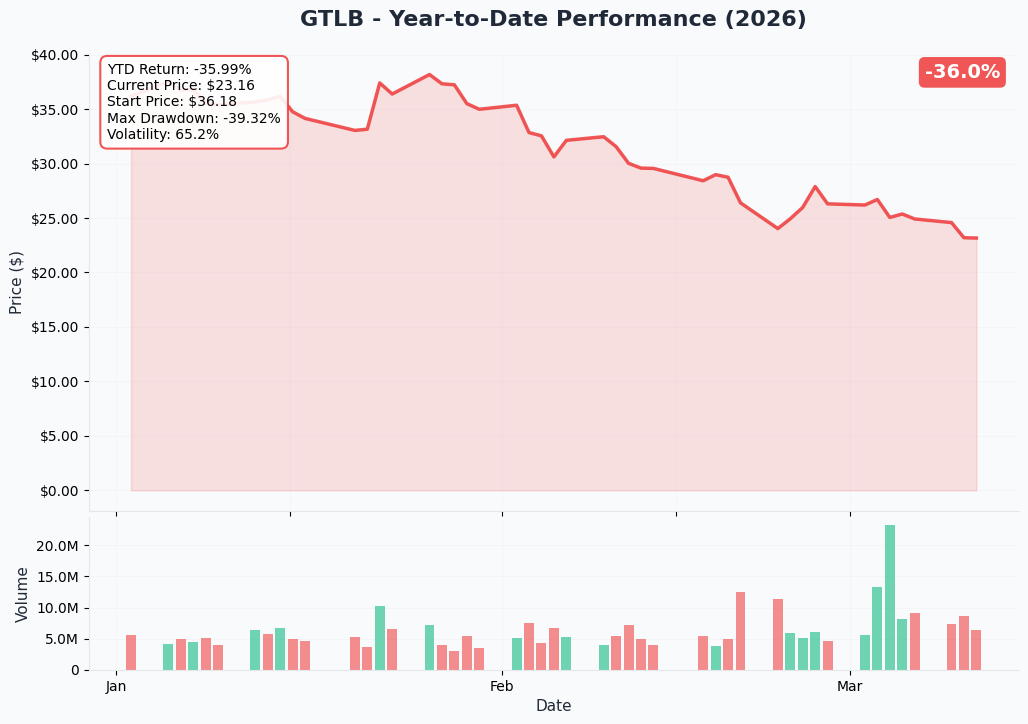

GTLB has had a brutal 2026, down roughly -39% year-to-date from the start of the year. The sharpest single-day drop came on March 4, 2026 — the day after Q4 FY2026 earnings — when the stock printed its all-time low near $22.78 as Piper Sandler downgraded from Overweight to Neutral with a $28 target (down from $55). The 52-week range tells the full story: $22.78 low to $54.61 high. As of today at $22.89, the stock is essentially sitting on the floor of a 12-month range.

Key observations:

- 📉 Parabolic decline: GTLB fell from ~$38 in early January to $22.78 in a single post-earnings gap — ~40% wipeout in under 10 weeks

- ⚠️ Near all-time lows: No historical support below current price; this is uncharted downside territory if selling resumes

- 📊 Volume surged on selloff: Heavy institutional distribution post-earnings (March 3-4) with volume multiples of average

- 🎯 Key recovery level: Reclaiming $28 would confirm stabilization; $35+ would signal real reversal thesis

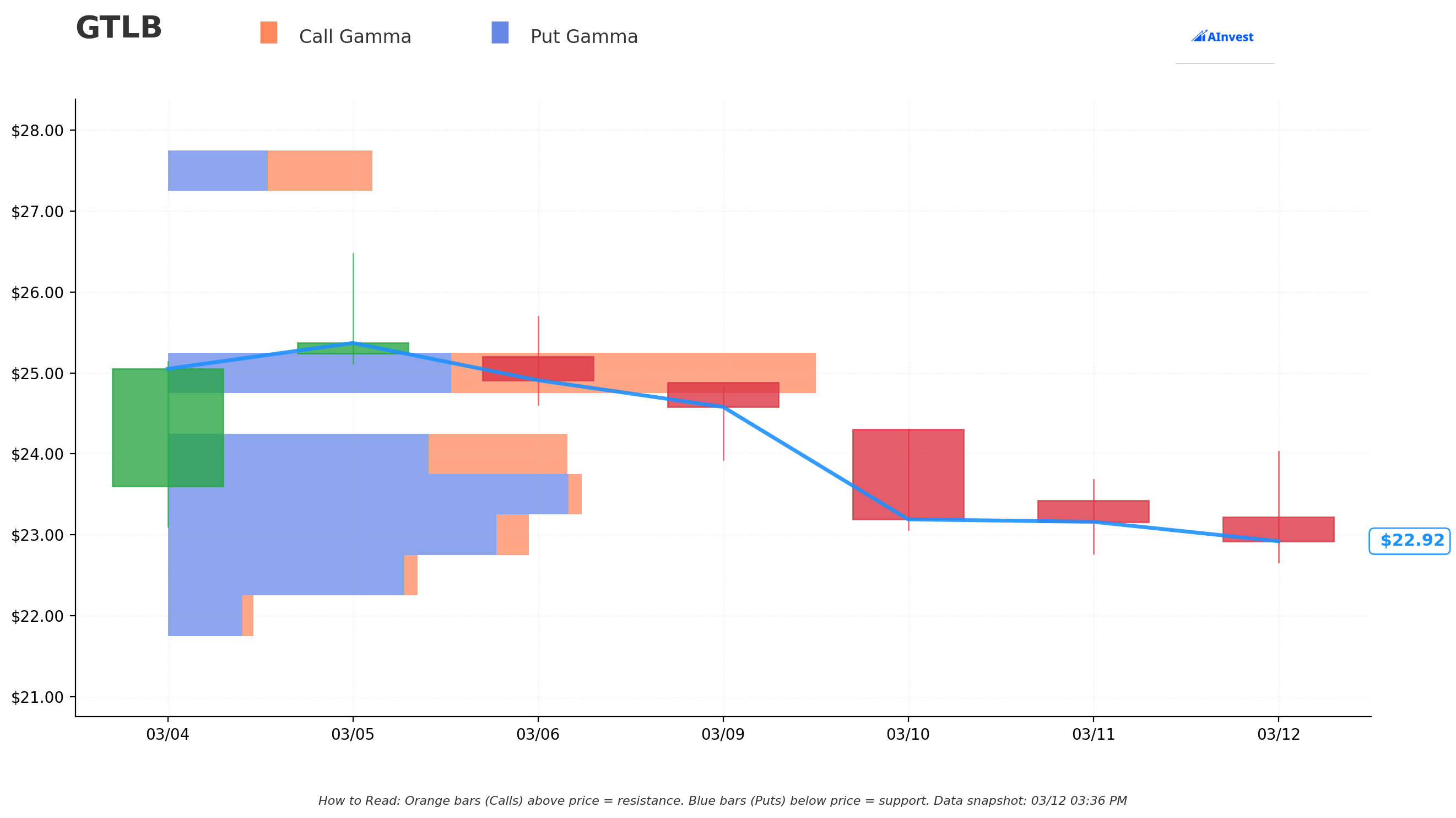

Gamma-Based Support & Resistance Analysis

Current Price: $22.89

The gamma exposure (GEX) map shows where options market makers are most concentrated — and therefore where they'll naturally buy and sell to stay hedged. These levels act as price magnets and walls:

🔵 Support Levels (Put Gamma Below Price):

- $22.50 — Strongest nearby put gamma support (0.53) — this is the first and most critical floor. If GTLB holds here, the path of least resistance could be sideways-to-up

- $22.00 — Secondary support zone; losing this level would put a test of sub-$22 in play

🟠 Resistance Levels (Call Gamma Above Price):

- $23.00 — First overhead resistance with 0.82 total GEX; small bounce attempts will likely stall here initially

- $23.50 — Stronger resistance at 0.93 GEX — the key short-term ceiling

- $24.00 — Moderate resistance at 0.90 GEX

- $25.00 — Major resistance at 1.46 GEX — this is the key level for bulls to reclaim; above $25 and momentum can shift materially

Net GEX Bias: Bullish — Call gamma (6.83) exceeds put gamma (6.00), suggesting the options market structure leans toward supporting price over the near term. This is a meaningful contrast to the bearish price trend.

What this means in plain English: GTLB is pinned between $22.50 support and $23.50 resistance in the near term. Any sustained rally needs to clear $25.00 — the biggest call gamma level — to signal that dealers are shifting from neutral to supportive. The $22.50 put gamma level is the critical line in the sand: hold it and the floor holds, break it and the next natural stopping point is down near $22.00.

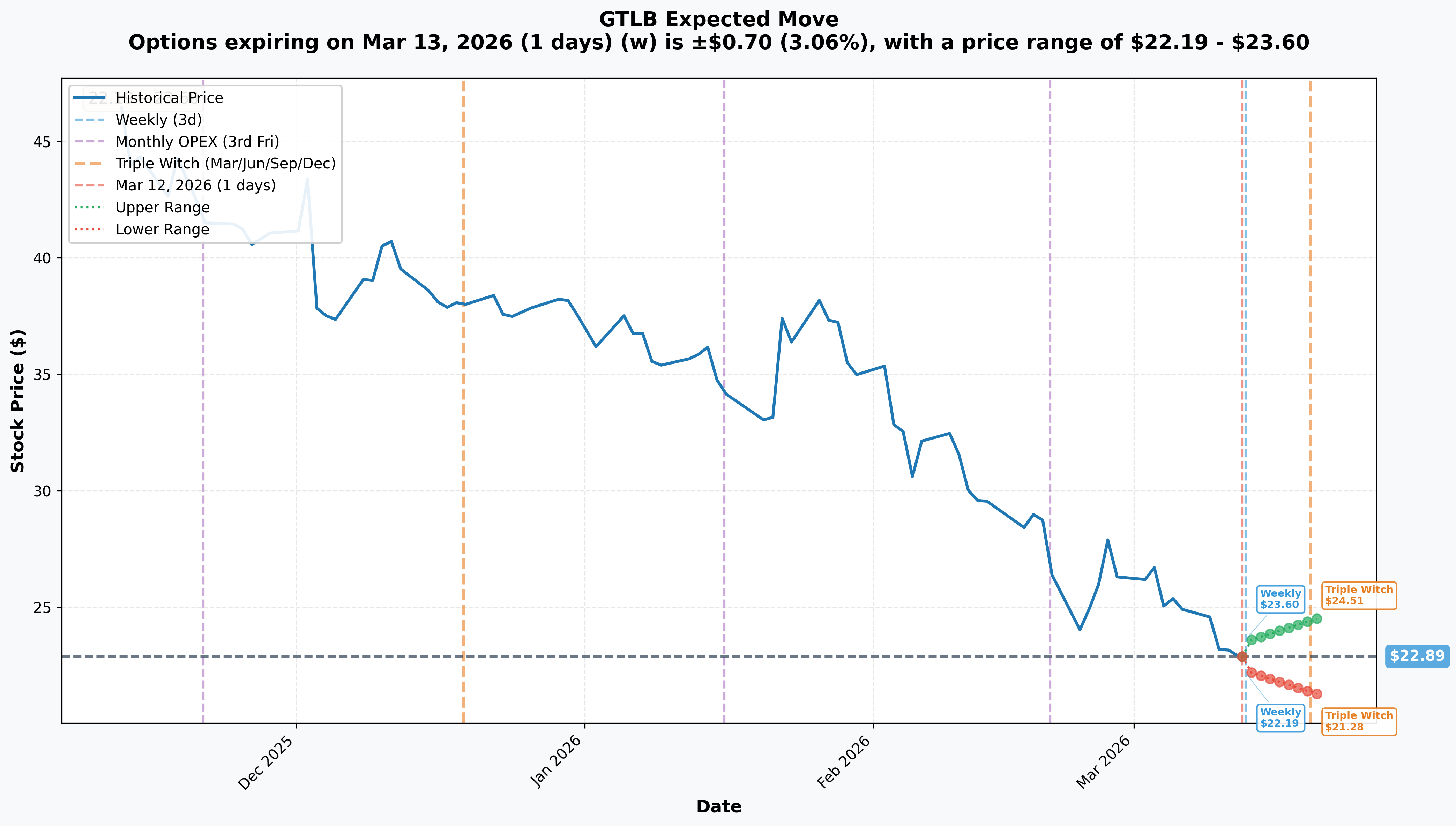

Implied Move Analysis

The options market is pricing these expected ranges for upcoming expirations:

- 📅 Weekly (March 13 — 1 day): ±$0.70 (±3.06%) → Range: $22.19 - $23.60

- 📅 Monthly OPEX (March 20 — Triple Witch): ±$1.61 (±7.05%) → Range: $21.28 - $24.51

Translation: Options traders expect GTLB to stay in a tight $22 - $24 range near-term. The March 20 Triple Witch OPEX represents the bigger uncertainty window — a 7% implied move in either direction. The bearish tail of that range ($21.28) sits below all visible gamma support, underscoring how unstable the current price level is.

Key insight for the short put seller: By selling 2028-01-21 puts, this institution completely avoids near-term event volatility (weekly and OPEX). They have 22 months of time value working in their favor — short-term swings to $21-22 are noise relative to their $18.20 breakeven.

🎪 Catalysts

✅ Recent / Already Happened

Q4 FY2026 Earnings — March 3, 2026 (JUST REPORTED)

GitLab beat consensus on both revenue and EPS for Q4, but the stock sold off hard on guidance:

- Q4 Revenue: $260.4M vs $252M expected (+3.3% beat); +23% YoY — per Business Wire earnings release

- Q4 Non-GAAP EPS: $0.30 vs $0.23 consensus (+30.4% beat)

- FY2026 Full-Year Revenue: $955M (+26% YoY); crossed $1B ARR milestone — per GitLab IR

- Free Cash Flow: $220M for FY2026 (+83% YoY); $1.26B total liquidity

- NRR: 118% — per Yahoo Finance earnings highlights

- FY2027 Revenue Guidance (THE PROBLEM): $1.099B - $1.118B = 15-17% growth vs 26% prior year — per Seeking Alpha

- Q1 FY2027 Revenue Guidance: $253M - $255M; midpoint slightly below the $256.69M prior consensus — per Ticker Report

$400M Share Repurchase Authorization — March 3, 2026

GitLab's board authorized its inaugural $400M buyback program alongside Q4 results — roughly 10% of the current market cap at today's prices. CFO Jessica Ross called it a confidence signal. At $22-25 per share, the company could theoretically retire ~16-17 million shares (nearly 10% of float) before the authorization is exhausted.

Piper Sandler Downgrade — March 4, 2026

Piper Sandler's Rob Owens cut GTLB from Overweight to Neutral with a $28 target (down from $55), framing FY2027 as a "transition year." DA Davidson maintained Neutral with a $30 target (cut from $45) — per Benzinga.

GitLab Duo Agent Platform GA — January 15, 2026

GitLab formally launched its Duo Agent Platform to general availability on January 15, 2026 — only 7 weeks before the Q4 earnings call. The platform introduces autonomous AI agents across the full SDLC, with native integrations for Anthropic Claude Code and OpenAI Codex, plus custom/external agent support. Premium tier customers get $12/user/month in credits; Ultimate customers get $24/user/month — per about.gitlab.com launch blog. This is the core bet management expects to drive re-acceleration.

MSP Partner Program Expansion — February 26, 2026

GitLab expanded its Managed Service Provider program to embed agentic AI into enterprise DevSecOps delivery through channel partners, targeting regulated industries with data sovereignty requirements — per Business Wire announcement.

🔥 Upcoming Catalysts

Q1 FY2027 Earnings — Expected June 9, 2026

This is THE binary event for the next 90 days. Wall Street wants to see whether Duo Agent pilots are converting to production, whether NRR of 118% is holding, and whether gross margins are tracking within the 85-87% guided band. Any upward revision to the $1.099B-$1.118B FY2027 revenue envelope would be the primary catalyst for re-rating — MarketBeat earnings calendar here.

Key metrics to watch on June 9:

- 🎯 Revenue vs $253M-$255M Q1 guidance: beat or miss?

- 🤖 Duo Agent adoption: credit consumption, pilots converting to production

- 📈 NRR trajectory: hold at 118% or start decelerating?

- 💰 Buyback execution: how much of the $400M has been deployed?

$400M Buyback Execution (Ongoing)

At current prices, buyback deployment represents a meaningful floor catalyst. Management has discretion on timing — if they begin purchasing materially in Q1 FY2027, it signals confidence in the floor at current price levels — per GitLab IR.

Duo Agent Monetization Ramp (Q1-Q2 FY2027)

Management guided for "minimal revenue contribution" from Duo Agent in FY2027 because the platform had been live for only 7 weeks at the time of the earnings call. The rate at which enterprise customers exhaust included credits and purchase overages is the leading indicator of eventual re-acceleration — per Seeking Alpha Duo Agent analysis.

AWS Partnership Milestones (H2 2026)

The 3-year AWS strategic collaboration (August 2025) includes milestones around GitLab Dedicated for regulated industries. New wins in healthcare, financial services, and the U.S. federal government via the AWS channel are incremental upside not yet in consensus models — per Yahoo Finance partnership coverage.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here are the key scenarios through the 2028-01-21 expiration — and the nearer-term setup:

📈 Bull Case — ~25% Probability

Target: $32 - $46 (12-24 month horizon)

How we get there:

- ✅ Q1 FY2027 earnings (June 9) shows Duo Agent credit consumption accelerating and NRR holding or improving, triggering re-rating toward analyst consensus average of $46.13 — per public.com analyst consensus

- 🚀 Duo Agent monetization ramp in H2 FY2027 proves the "transition year" thesis was correct; Q2 or Q3 guidance raised

- 💰 $400M buyback actively deployed at $22-25, reducing share count by 8-10% and providing ongoing bid

- 🤝 AWS channel wins in regulated industries show up in $100K+ ARR customer additions (currently 1,456, up 18% YoY)

- 📈 Sector re-rating: Enterprise software P/S multiple expands back toward 6x peer average from current 4.1x-4.4x — per Simply Wall St valuation analysis

- 🛡️ Emirates Airlines-type wins show GitLab Duo beating GitHub Copilot in head-to-head enterprise evaluations

- Short put outcome: Expires worthless for the seller — all $20M premium pocketed

🎯 Base Case — ~55% Probability

Target: $24 - $32 (sideways-to-gradual recovery)

Most likely scenario:

- 📊 GTLB stabilizes near current lows, trades in a choppy $22-$28 range for 6-12 months as the market waits for Duo Agent proof points

- 💤 Q1 FY2027 earnings in-line with guidance ($254M midpoint), no meaningful guide-up yet, but no disaster

- 🔄 Buyback provides floor support; stock slowly grinds toward $28-32 as the buyback consumes supply

- 📈 Duo Agent adoption slow but not zero — management shows credit consumption growing and a handful of enterprise production deployments

- 🎢 Gross margins track at the 85-87% guided floor, no downside surprise to AI infrastructure costs

- Short put outcome: The seller holds through volatility and eventually closes or rolls at a gain as time decay works in their favor; $18.20 breakeven never seriously threatened

📉 Bear Case — ~20% Probability

Target: $16 - $21 (significant downside)

What could break the trade:

- 😰 Q1 FY2027 earnings miss AND Q2 guide-down, signaling Duo Agent monetization is failing entirely — stock could retest sub-$20 levels not seen since the 2022 post-IPO washout

- 🚨 AI disruption thesis plays out — GitHub Copilot bundled "free" into enterprise Azure agreements compresses GitLab's per-seat pricing power faster than expected

- ❗ Gross margins undershoot the 85% floor as Duo Agent compute costs run hot without proportional revenue; profitability story cracks — per Seeking Alpha deceleration analysis

- 📉 Macro deterioration forces enterprise IT budget cuts; NRR drops below 110%

- 💸 For the short put seller: below $18.20 effective breakeven, they begin losing money. At $15 stock price, they're down ~$3.20/share × 21,372 contracts × 100 = ~$6.8M unrealized loss — though they still own shares at a 34% discount to today's price

💡 Trading Ideas

🛡️ Conservative: The Patient Floor Play

Play: Wait for consolidation confirmation, then buy GTLB shares (or go long calls) with a thesis that the $400M buyback and all-time-low valuations provide downside protection

Why this works:

- 💰 GTLB at 4.1x trailing revenue is trading below the 3.4x US software industry average in some comps — Simply Wall St notes it looks undervalued vs peers

- 🛡️ $1.26B total liquidity with zero debt = no solvency risk at any plausible stock price

- 📊 $400M buyback at $22-25 prices theoretically removes ~9% of float — ongoing mechanical floor bid

- 🎯 Wait for a weekly close above $23.50 gamma resistance to confirm near-term stabilization before entering

Entry: $22.50 - $23.50 (current range; buy into weakness near $22.50 gamma support)

Target: $28 - $32 (Piper Sandler's current target of $28 represents the first meaningful recovery level)

Stop: Close below $21.50 sustained for more than 2 days — would signal structural selling pressure overcoming buyback

Risk level: Low-Moderate (stock position, defined stop) | Skill level: Beginner-friendly

⚖️ Balanced: The Pre-Earnings Setup

Play: Buy GTLB call spreads expiring in late June 2026 to capture the Q1 FY2027 earnings catalyst on June 9

Structure: Buy $25 calls / Sell $30 calls (June 2026 expiration)

Why this works:

- 📅 The June 9 earnings date falls within June expiration — you're buying defined upside into the catalyst with limited premium at risk

- 🎯 The $25 strike sits right at the major call gamma resistance level — a close above $25 signals momentum shift

- 📊 Risk is capped at the spread premium paid; no naked exposure if guidance disappoints again

- 💡 Even with implied volatility compressed post-earnings selloff, a beat-and-raise scenario could push GTLB from $22 to $28-30 quickly, making a $25/$30 spread a solid risk/reward setup

Estimated cost: ~$1.50 - $2.00 per spread (estimate; verify actual prices)

Max profit: ~$3.00 - $3.50 per spread if GTLB closes above $30 at June expiration

Max loss: Premium paid (~$1.50-$2.00 per spread) — entirely defined risk

Risk level: Moderate (defined risk, binary catalyst bet) | Skill level: Intermediate

🚀 Aggressive: Copy the Whale (Scaled Down)

Play: Sell cash-secured puts at the $20 strike expiring December 2026 — mirroring the institutional trade's structure at a more retail-accessible strike below the current price

Structure: Sell GTLB $20 puts expiring December 2026

Why this works:

- 💸 GTLB at $22.77 means the $20 strike is ~12% out-of-the-money — you collect premium for promising to buy GTLB at $20 if it falls there

- 🎯 $20 puts give you a breakeven near $17-18 after premium collection — pricing in a further catastrophic decline from an already multi-year low

- 📊 If GTLB holds $20 (which includes all the buyback support levels), you keep the full premium with zero obligation

- 🤝 You're aligning with the institutional bet — they sold $27.50 strike puts to collect at higher premium; you're selling $20 strike puts for smaller but proportional income with more safety margin

Key risks of this trade:

- ⚠️ You must be prepared to BUY GTLB at $20 if assigned — have cash ready

- 📉 In a bear case scenario, you could end up owning GTLB at $20 while it trades at $15-17 — that's a real loss

- 🎰 This is NOT a low-risk trade — never sell naked puts unless you genuinely want to own the shares at the strike price

Estimated premium: ~$1.50 - $2.50 per contract (estimate; verify actual market prices before trading)

Breakeven: ~$17.50 - $18.50 (premium-adjusted)

Risk level: High (obligation to buy shares if assigned) | Skill level: Advanced — Requires sufficient cash collateral and comfort owning GTLB at $20

⚠️ Risk Factors

Don't ignore these real risks:

-

🤖 AI disruption to the DevSecOps model (HIGH): The single biggest bear argument. If AI coding agents commoditize software development and enterprises reduce developer headcount by 30-50%, GitLab's seat-count-driven revenue model faces structural headwinds that no buyback or Duo Agent upsell can fully offset. This is the same "AI kills the category" concern that drove the stock to all-time lows in early March — per Motley Fool analysis of the selloff

-

📉 Revenue growth deceleration (HIGH): The move from 26% FY2026 growth to 15-17% FY2027 guided is not a rounding error — it's a structural signal. If Duo Agent monetization fails to re-accelerate growth toward 20%+ by FY2028, the stock's current ~4x revenue multiple could compress further toward 2-3x as the growth premium evaporates — per SignalBloom deceleration analysis

-

💸 Gross margin compression (MEDIUM): The FY2027 guidance implies gross margins dropping from 89% to 85-87% to support Duo Agent infrastructure. If customers use included credits heavily without purchasing overages, GPU compute costs could push margins below the 85% floor — creating a scenario where revenue grows but profits don't — per Seeking Alpha guidance coverage

-

⚖️ Microsoft / GitHub competitive pressure (HIGH): Microsoft's ability to bundle GitHub Copilot into enterprise Azure agreements at little or no incremental cost creates a structurally unfair pricing dynamic. GitLab's per-seat premium faces sustained compression in competitive deals where the "free" GitHub option is on the table. Analysts have flagged GitLab's AI pricing strategy as a potential monetization ceiling

-

📊 No technical support below $22.50: GTLB is at all-time lows. There is no historical support structure below the current price. Any negative news — macro shock, guide-down, competitive loss — could push the stock below $20 with no obvious floor until much lower levels

-

🌍 Macro / geopolitical headwinds (MEDIUM): In March 2026, GTLB's decline was amplified by U.S. payroll weakness (-92,000 in February vs. expectations) and Middle East tensions. Enterprise software budgets contract in recessions — and GTLB at 4x revenue still requires a premium to fair value for a decelerating grower if macro conditions worsen — per Motley Fool macro context

-

🎯 Short put assignment risk: If the institutional seller is assigned shares, they'd own GTLB at an effective $18.20 cost basis. That's great vs today's price but not great vs a $15 stock in a prolonged bear scenario. For retail traders considering similar short put strategies, assignment risk is real and requires cash reserves

🎯 The Bottom Line

Real talk: Someone just deposited $20 million into their account by selling deep in-the-money puts on one of tech's most beaten-down stocks. This isn't a panicky move — it's a calculated, long-duration bet that GitLab at $22.77 represents a price so dislocated from fundamental value that the $18.20 breakeven (after premium) is nearly impossible to breach over 22 months.

What this trade signals:

- 🎯 Institutional conviction that the post-earnings selloff is overdone — they're not buying calls (speculative) or stock (obvious), they're SELLING downside protection at a price that prices in catastrophe

- 💰 The $27.50 strike being so deeply in-the-money (20%+ ITM) means they're comfortable being assigned at effective $18.20 — a price that implies GitLab's $955M in FY2026 revenue plus $1.26B in liquidity is worth less than $3B total

- 📅 The 2028-01-21 expiration captures both Q1 FY2027 earnings (June 2026) AND Q2 FY2027 earnings (September 2026) — this institution believes the Duo Agent monetization story has at least 18 months to play out

Action plan depending on your situation:

If you're bullish on the AI DevSecOps thesis:

- ✅ Consider initiating a starter position in GTLB near $22.50 gamma support, sized for the reality that all-time-low stocks can still make new all-time lows

- 📅 Mark your calendar for June 9, 2026 — Q1 FY2027 earnings is the most critical near-term event; if Duo Agent adoption data impresses, the stock could re-rate quickly toward $28-32

- 🛡️ Use the $22.50 gamma level as your stop guide — a sustained breakdown below $22 removes the near-term floor thesis

- 💡 The analyst consensus target of $46 with 23 of 29 analysts maintaining Buy-equivalent ratings suggests significant mean-reversion upside IF the transition year thesis holds

If you're waiting for confirmation:

- 👀 Watch for volume-confirmed reclaim of $25 resistance — that's the gamma level where call exposure becomes dominant and market makers shift from neutral to supportive

- ⏰ The $400M buyback is an ongoing quiet bid — check quarterly filings for execution progress

- 📊 Key sign of Duo Agent traction: any analyst commentary on rising credit consumption or first enterprise "production" deployment case studies before the June earnings call

If you're bearish:

- 📉 The $21.28 lower bound of the March OPEX implied move is the near-term downside target — a close below that triggers a potential test of $20 and then uncharted territory

- ⚠️ But fighting a $400M buyback authorization at all-time lows with $1.26B in company cash is a dangerous short — be aware of squeeze risk if any positive Duo Agent news surfaces

The bottom line verdict: GitLab is either a 4x revenue value trap heading toward the low teens as AI eats its market — or it's a beaten-down category leader setting up for a significant mean reversion as the Duo Agent platform proves out. The institutional player who just sold $20M in puts is firmly in Camp #2, and they're putting real money behind that conviction at what they believe is effectively a 20%-discounted floor entry.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results. The ~6,400x Vol/OI ratio reflects the unusualness of this specific trade relative to prior open interest on this contract — it does not imply the trade will be profitable or that retail traders should replicate it. Short put strategies require sufficient capital to take delivery of shares and can result in significant losses if the underlying stock declines substantially. Always conduct your own due diligence and consult a licensed financial advisor before trading. The institutional seller's objectives, risk tolerance, and portfolio context may be entirely different from yours.