🎯 KLAC $6.7M Put Play - Big Money Hedges Ahead of Earnings! 💰

📅 October 13, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $6.7M on KLAC puts with the $1,000 strike expiring December 19th! This massive bearish bet comes 16 days before the company's October 29th earnings, suggesting institutional players are hedging against downside despite KLAC's stellar +61% YTD run. Translation: Smart money is buying insurance on this semiconductor rocket ship! 🚀🛡️

📊 Company Overview

KLA Corporation (KLAC) is the semiconductor industry's inspection and measurement king:

- Market Cap: $129.4 Billion

- Industry: Optical Instruments & Lenses (Semiconductor Equipment)

- Employees: 15,200

- Primary Business: Process control and yield management solutions - the tools that make sure chips are perfect

What they actually do: KLA makes the quality control equipment that checks every semiconductor chip during manufacturing. Think of them as the inspectors that ensure your iPhone's processor is flawless. They dominate this space with a commanding 56% market share in process control equipment.

💰 The Option Flow Breakdown

The Tape (October 13, 2025 @ 12:52:53):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:52:53 | KLAC | MID | BUY | PUT | 2025-12-19 | $6.7M | $1,000 | 1.2K | 161 | 1,150 | $1,031.17 | $58 |

🤓 What This Actually Means

This is a protective put purchase - sophisticated downside insurance! The trader:

- Paid $6.7M in premium to control 115,000 shares worth ~$118M

- Bought protection at the $1,000 strike, just 3.1% below current price

- Has 67 days until expiration (December 19th)

- Breaks even at $942 at expiration ($1,000 strike - $58 premium paid)

- Profits if KLAC drops below $942 by December

Unusual Score: 🌋 VOLCANIC (10/10) - This is 791x larger than average KLAC option trades! This happens maybe a few times per year for a stock this size. The z-score of 124.38 means this is statistically off the charts.

Translation: This isn't your neighbor Bob's Robinhood account. This is serious institutional money buying downside protection. Either someone's hedging a massive long position, or they know something the market doesn't about upcoming risks.

📈 Technical Setup / Chart Analysis

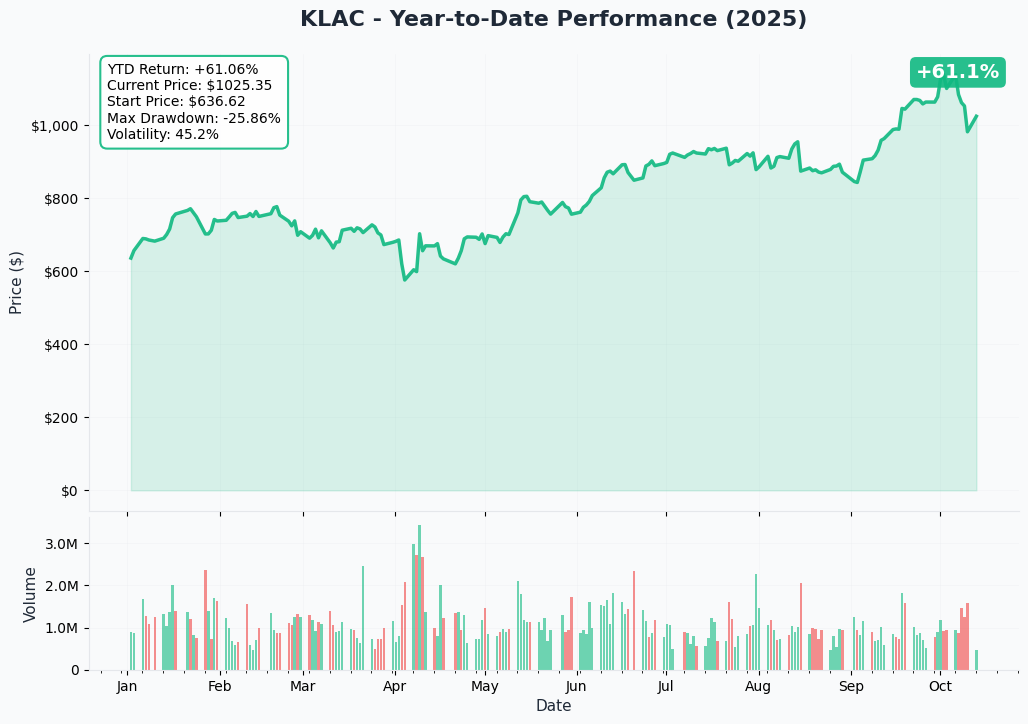

YTD Performance Chart

KLA Corporation is crushing it in 2025 with +61.1% YTD returns - nearly doubling from $636 to the current $1,025! But here's what stands out:

Key observations:

- Massive rally: From April lows around $580 to recent highs above $1,100 (89% move!)

- Recent pullback: Dropped from October 6th peak of $1,143 to current $1,025 (10.3% correction)

- High volatility: 45.2% annualized - this stock moves fast in both directions

- Volume spikes: Increased institutional activity during breakouts and pullbacks

- Max drawdown: -25.86% earlier this year shows the downside potential

The chart shows a parabolic move that's now consolidating. Smart money often hedges after massive runs like this.

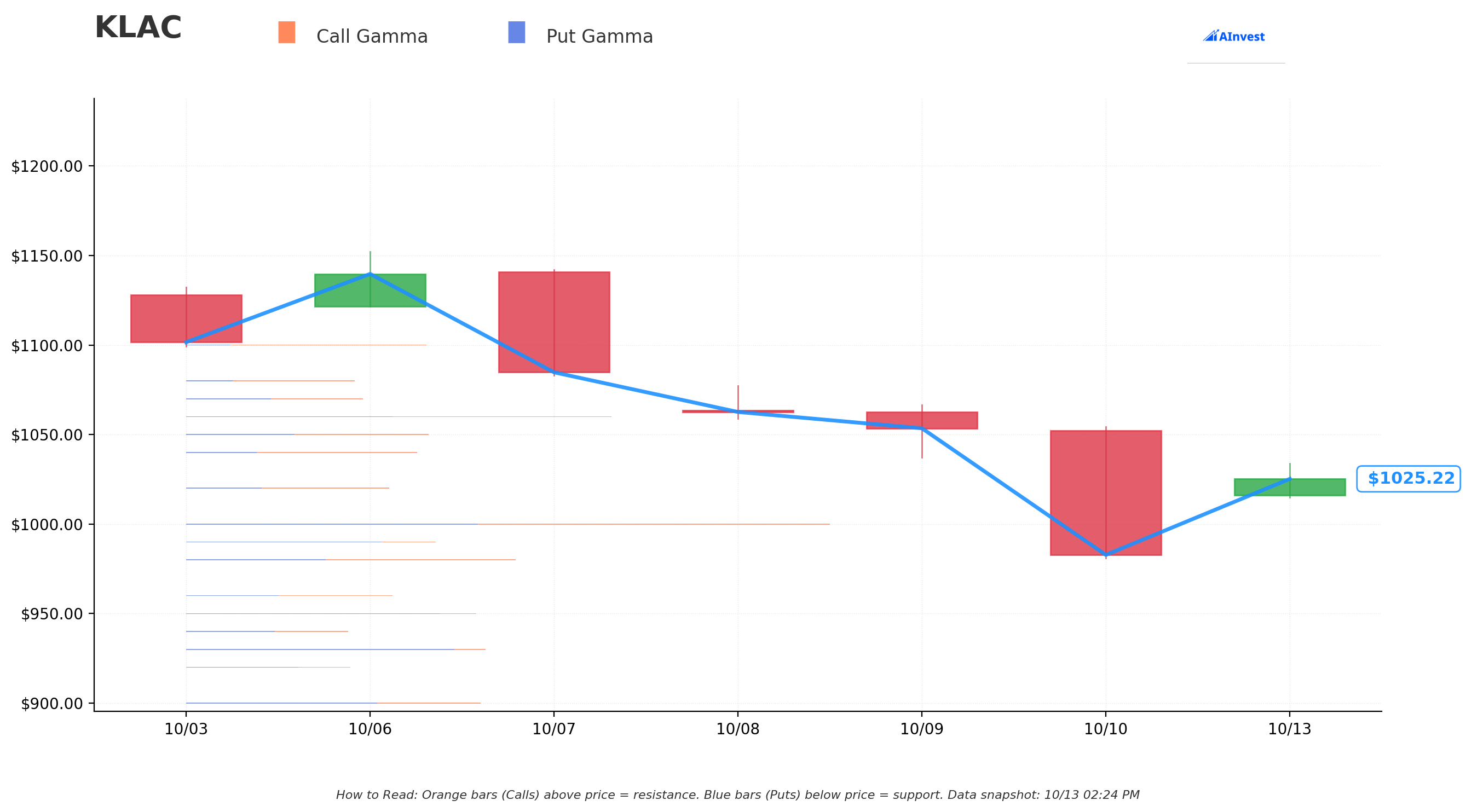

Gamma-Based Support & Resistance Analysis

Current Price: $1,025.64

The gamma landscape reveals critical battleground zones:

🔵 Support Levels (Put Gamma Protection):

- $1,000 - STRONGEST support with 0.49 total gamma (2.5% below) - This is why the put strike makes sense!

- $990 - Secondary floor with 0.18 gamma (3.5% below)

- $980 - Moderate support at 0.25 gamma (4.4% below)

- $950 - Major support shelf at 0.22 gamma (7.4% below)

- $930 - Deep support at 0.23 gamma (9.3% below)

🟠 Resistance Levels (Call Gamma Ceilings):

- $1,040 - Nearest resistance with 0.17 gamma (1.4% above) - immediate ceiling

- $1,050 - Secondary wall at 0.18 gamma (2.4% above)

- $1,060 - HEAVIEST resistance with 0.32 gamma (3.4% above)

- $1,100 - Major ceiling at 0.18 gamma (7.3% above)

What this means: The $1,000 level isn't random - it's the strongest support zone with massive put gamma. If KLAC breaks below $1,000, market makers will have to sell aggressively, potentially accelerating downside to $980-$950. The net gamma bias is bearish (more put gamma than call gamma), meaning the market is positioned defensively.

🎪 Catalysts

Upcoming Events

Q1 2026 Earnings - October 29, 2025 ⚡

- Wall Street expects EPS of $8.47 (up 15.6% YoY) (Yahoo Finance consensus)

- Revenue guidance: $3.0B - $3.3B (midpoint $3.15B) (Investing.com report)

- Key focus areas:

- Advanced packaging revenue growth (targeting $925M for full 2025)

- China exposure impact (~30% of revenue vs 41% last year)

- Tariff margin pressure (50-100 basis points impact)

- AI-driven semiconductor demand sustainability

Advanced Packaging Market Surge 🚀

- Revenue projected to surge 85% YoY with raised guidance to $925M

- High-Bandwidth Memory (HBM) demand for AI applications driving growth

- 2.5D and 3D chip integration creating powerful AI flywheel for KLA's inspection tools

Analyst Price Target Updates 📊

- Recent upgrades: Goldman Sachs to $1,120, Morgan Stanley to $1,093, Stifel to $1,050

- Median target: $950 (7.5% downside from current)

- Range: $750 to $1,120

Recently Completed

Fiscal 2025 Record Results 🎉

- Revenue: $12.16B (up 24% YoY)

- Net Income: $4.06B (up 47% YoY)

- EPS: $30.37 (up from $20.41)

- Profit Margin: 33% (improved from 28%)

- Q4 2025 beat expectations with EPS of $9.38 vs $8.54 estimate

Market Share Expansion 📈

- Maintained 56% market share in process control equipment

- Gaining share in advanced packaging technologies

- Process control intensity rising from 1% to 5-6% of manufacturing costs

🎲 Price Targets & Probabilities

Using gamma levels, catalyst timeline, and technical analysis:

🚀 Bull Case (30% chance)

Target: $1,100-$1,150

Why it works:

- Earnings beat on advanced packaging growth (85% YoY surge)

- AI semiconductor demand exceeds expectations

- China risk proves manageable

- Breaks above $1,060 gamma resistance

- Analyst upgrades accelerate momentum

Catalysts: Better-than-expected guidance, memory market recovery confirmation, new AI chip design wins

😐 Base Case (45% chance)

Target: $950-$1,050 range

Why it works:

- Mixed earnings with solid results but cautious China guidance

- Stays within current gamma bands

- Consolidation after parabolic run makes sense

- Tariff impact weighs on margins as expected

- Market digests valuation at 27.85x forward P/E

Catalysts: In-line earnings, stable guidance, sector rotation dynamics

The put position profits if we're toward the lower end of this range

😰 Bear Case (25% chance)

Target: $900-$950

Why it works:

- China restrictions worse than anticipated ($500M+ revenue impact)

- Tariff margin pressure exceeds 100 bps

- Memory market recovery stalls

- Breaks $1,000 support, triggering gamma unwind to $980-$950

- Broader semiconductor correction

Catalysts: Disappointing guidance, increased export restrictions, customer capex cuts

The put trade is positioned perfectly for this scenario - profits accelerate below $942

💡 Trading Ideas

🛡️ Conservative: Follow the Hedge

Play: Buy protective puts at $1,000 strike (Dec 19th)

Buy $1,000 puts for ~$58-60 per contract

Risk: Premium paid (~5.6% of stock price) Reward: Protection against any drop below $942 Why this works: You're literally copying institutional money. If they're hedging at $1,000, there's a reason. Protects your KLAC longs through earnings and year-end volatility.

Position sizing: For every 100 shares you own, buy 1 put contract. Example: Own 200 shares? Buy 2 puts for ~$11,600 total insurance cost.

⚖️ Balanced: Put Spread for Lower Cost

Play: Bear put spread (Dec 19th expiration)

Buy $1,000 puts, sell $950 puts

Risk: Net premium paid (roughly $35-40 per spread) Reward: $50 max profit per spread if KLAC drops below $950 Why this works: Reduces hedging cost by 40% while still protecting the most likely downside zone. Maximum profit if the bear case plays out.

Breakeven: Around $960-965 depending on execution

🚀 Aggressive: Fade the Hedge (Contrarian)

Play: Sell cash-secured puts at $950 (Dec 19th)

Sell $950 puts for ~$25-30 premium

Risk: Obligated to buy KLAC at $950 if assigned Reward: Keep premium if KLAC stays above $950 Why this works: If you believe the hedge is excessive and want to buy KLAC cheaper, sell puts at the major gamma support. Either you collect premium or you buy a great company at a 7.4% discount.

Net cost if assigned: $950 - premium collected = ~$920-925 effective entry

⚠️ Risk Factors

China Export Restrictions 🇨🇳

- 30% revenue exposure down from 41%, but still significant

- Estimated $500M revenue reduction in 2025 from export controls

- Further restrictions could accelerate under current administration

Tariff Margin Pressure 💰

- 50-100 basis point impact on gross margins expected

- Could worsen if trade tensions escalate

- Competitors face similar pressures

Cyclical Semiconductor Market 🔄

- Despite AI tailwinds, memory and logic segments remain cyclical

- Customer capex cycles can shift quickly

- Inventory corrections in semiconductor supply chain

Valuation at Stretched Levels 📊

- Trading at 27.85x forward P/E vs historical average

- Expectations for continued growth are high

- Any guidance miss could trigger multiple compression

Earnings Execution Risk 🎯

- October 29th results could disappoint on China impact

- Advanced packaging growth expectations are aggressive (85% YoY)

- Market may be pricing in perfection

🏁 The Bottom Line

Real talk: This $6.7M put purchase isn't random - it's calculated risk management ahead of a binary event (earnings on October 29th). Someone with serious money is buying insurance on a stock that's up 61% YTD, currently sitting near $1,025, with the $1,000 strike representing the strongest gamma support level.

If you own KLAC: Consider hedging through earnings. The risk/reward has shifted after the massive run. A 5-6% insurance cost (buying $1,000 puts) is reasonable given China risks and valuation.

If you're watching: Wait for post-earnings clarity. The setup suggests volatility into October 29th. Either buy the dip if it breaks $1,000 support, or wait for confirmation above $1,060 resistance.

If you're bearish: The $1,000 put strike makes technical sense at the gamma support level. If earnings disappoint, the unwind to $950-980 could be swift.

Mark your calendar:

- October 29, 2025 - Q1 2026 earnings call (IR announcement)

- December 19, 2025 - Put expiration date

The trade thesis: After a parabolic 61% YTD run, smart money is hedging downside risk through the critical earnings catalyst. Whether you follow the hedge or fade it depends on your conviction in KLA's AI semiconductor dominance versus near-term China/tariff headwinds.

Disclaimer: Options trading involves substantial risk. This analysis is for educational purposes only and not financial advice. The unusual score calculation is based on recent trading patterns and may not reflect all market conditions. Past performance doesn't guarantee future results.

About KLA Corporation: KLA is the global leader in process control and yield management solutions for semiconductor manufacturing with a $129.4 billion market cap. The company specializes in inspection and metrology equipment that ensures chip quality, holding a dominant 56% market share in its core segment.