🤖 MSFT $12M LEAP Call - Big Money Making a Year-Long Bet on Microsoft's AI Comeback!

📅 March 11, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $12 MILLION on MSFT calls expiring in March 2027 - that's a full-year LEAP bet that Microsoft AI and cloud will recover from its brutal post-earnings selloff! With MSFT trading at $402.70, down ~25% from its October 2025 all-time high of $539.83, this institution is making a high-conviction directional bet that the stock climbs at least 23% from here just to break even. Translation: smart money is betting the market has overreacted to Microsoft's AI spending concerns, and the real payoff comes when Azure growth and the M365 E7 launch prove the bears wrong.

📊 Company Overview

Microsoft Corporation (MSFT) is the world's second-largest company by market cap and arguably the most dominant platform in enterprise AI today:

- Market Cap: $3.01 Trillion

- Industry: Services - Prepackaged Software (NASDAQ)

- Current Price: $402.70 (down ~25% from ATH of $539.83 in October 2025)

- Primary Business: Windows OS, Microsoft 365, Azure cloud, Copilot/AI, Xbox gaming, LinkedIn, Dynamics 365 — they're basically in EVERY layer of enterprise technology

💰 The Option Flow Breakdown

📊 The Tape (March 11, 2026 @ 11:30:38)

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:30:38 | MSFT | BUY | CALL $460 | 2027-03-19 | $12M | $460 | 3,500 | 382 | 3,500 | $402.70 | $34.39 | MSFT20270319C460 |

- Strategy: Long Call (BTO)

- Z-Score: EXTREMELY_UNUSUAL

- Vol/OI Ratio: 9.16x (volume is over 9x the existing open interest — this is fresh, directional positioning)

🤓 What This Actually Means

This is a straight-up bullish LEAP bet on Microsoft's recovery story. Here's the breakdown:

- 💸 $12M premium paid: $34.39 per contract × 3,500 contracts × 100 shares = $12.04M out the door

- 🎯 $460 strike: That's 14% out-of-the-money from today's $402.70 spot — this is NOT a hedge, this is pure conviction

- 📅 March 2027 expiry: 373 days of runway — plenty of time to capture Q3 earnings (April 28), the M365 E7 GA launch (May 1), Microsoft Build 2026 (June 2-3), Q4 earnings (July), and beyond

- 📊 Vol/OI of 9.16x: Volume (3,500) is over 9 times the prior open interest (382) — someone opened this position fresh today, this isn't a close or a roll

- 🏦 Size matters: 3,500 contracts = 350,000 shares of exposure, equivalent to ~$141M in notional stock value — a massive directional bet

Breakeven math: $460 strike + $34.39 premium = $494.39 breakeven. That requires MSFT to rally ~23% from today's $402.70 just to start making money. The buyer needs a $91.69/share move in their favor. This is high conviction, long-duration speculation — not something you do lightly.

What's really happening here: This institution looked at MSFT's $625B commercial backlog (up 110% YoY), the upcoming M365 E7 launch at $99/user/month on May 1, and a stock trading at a forward P/E of just 21.3x (a massive discount to Apple at 32.7x and Alphabet at 27.2x) — and decided the market is pricing in too much doom. They're betting on Microsoft's AI/cloud monetization thesis playing out over the next 12 months.

Z-Score: EXTREMELY UNUSUAL — The 9.16x Vol/OI ratio and $12M single-ticket premium means this type of trade hits maybe a few times a year in MSFT. It's not routine institutional flow — this is a deliberate, sized, directional call on the stock at a meaningful time in the company's AI narrative arc.

📈 Technical Setup / Chart Check-Up

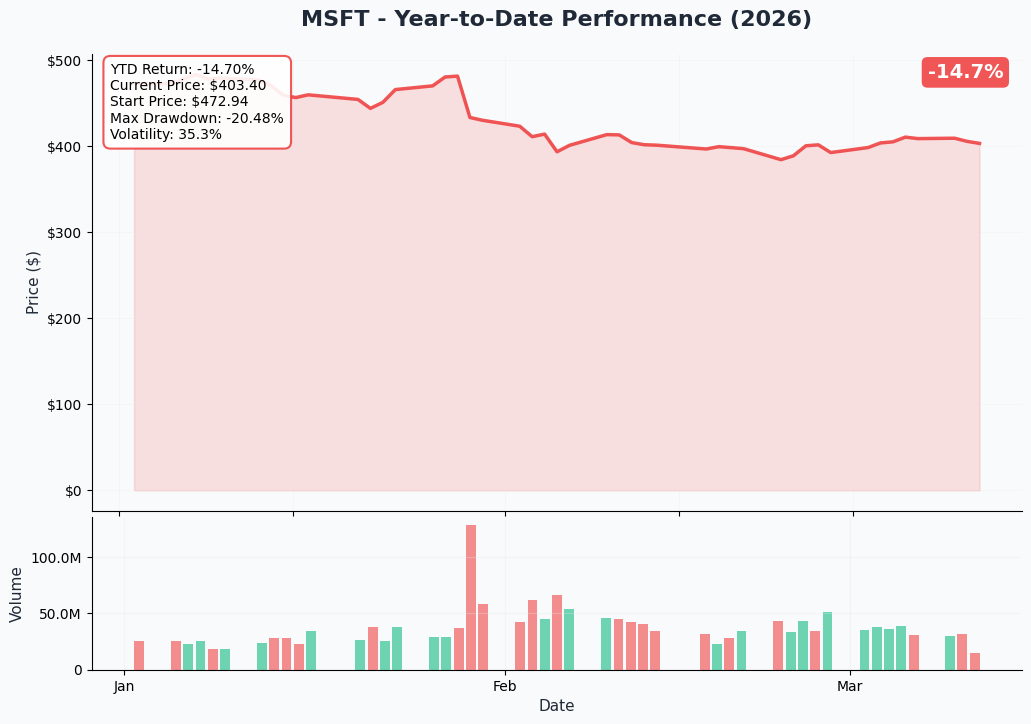

YTD Performance Chart

MSFT has had a rough ride in 2026. After hitting an all-time high of $539.83 in October 2025, the stock got crushed on Q2 FY2026 earnings on January 28 — Microsoft recorded its second-largest single-day market value loss in U.S. history, erasing $357B in market cap in a single session as investors punished the stock for decelerating Azure growth (39% vs. 40% the prior quarter) alongside a 66% surge in capex.

Key observations:

- 📉 Post-earnings crater: Dropped from ~$450 to below $400 after January 28 earnings — brutal one-day destruction

- 🔄 Consolidating: Stock has been basing in the $390-$415 range for over a month

- 📊 Valuation reset complete: Forward P/E of 21.3x is near 5-year lows relative to mega-cap peers

- 💡 Potential inflection: March 9 news of M365 E7 launch announcement is a fresh catalyst that had yet to move the stock meaningfully by today

- 🎯 Distance from ATH: -25.4% off peak is a meaningful discount for a company with $625B in commercial backlog

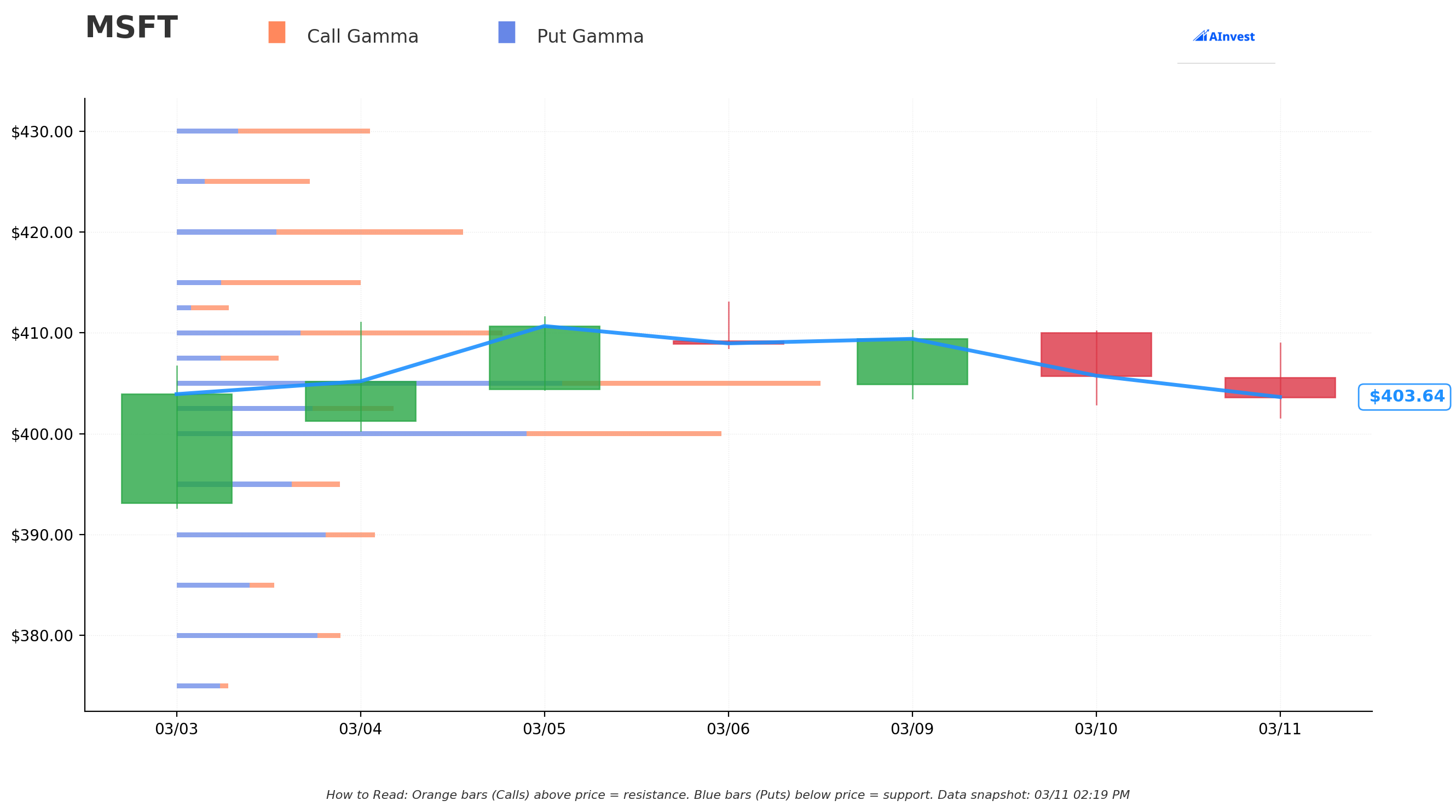

Gamma-Based Support & Resistance Analysis

Current Price: $403.65 (as of GEX snapshot at 14:20 ET)

The gamma exposure (GEX) map reveals the key price magnets and dealer-driven levels governing near-term price action in MSFT:

🔵 Support Levels (Put Gamma Below Price):

- $402.50 — Immediate support, 25.5B total gamma exposure, net GEX negative (-6.4B). Dealers buying dips here. This is the first line of defense — MSFT is almost sitting on top of it right now

- $400.00 — Strong structural floor with 64.4B total gamma. Net put bias (-18.6B) means dealers aggressively defend this round-number level. This is the critical support: break $400 and momentum accelerates lower

- $390.00 — Deep support at 23.5B gamma, the last meaningful floor before air pocket lower

🟠 Resistance Levels (Call Gamma Above Price):

- $405.00 — Nearest ceiling at 80.1B total gamma — the LARGEST single level in the entire chain. Net GEX negative (-15.9B) means there's mixed dealer hedging here but very heavy activity. This is the immediate wall to break

- $410.00 — Net positive GEX (+9.0B) at 40.1B total gamma, flips bullish — getting above $410 changes the character of the tape

- $415.00 — Clear call-dominant level (+11.5B net), 22.4B total gamma. Strong resistance but if cleared, momentum builds

- $420.00 — Net +10.5B GEX at 34.8B total — another step-resistance level

- $430.00, $440.00, $450.00 — Stacked resistance clusters with progressively lighter gamma. Getting through all of these is the setup required for this $460 call to come into play

What this means for traders: MSFT is pinned in a tight band right now — enormous support at $400 and massive resistance at $405. The $405 level (80.1B GEX) is the single largest gamma cluster in the near chain, creating significant dealer-induced friction on moves above that level. For the $460 LEAP call buyer, near-term pinning action is tolerable — they have 373 days for the levels to shift. The good news: net GEX bias overall is Bullish (376.1B call gamma vs. 306.7B put gamma), meaning the market structure ultimately leans toward upside over time.

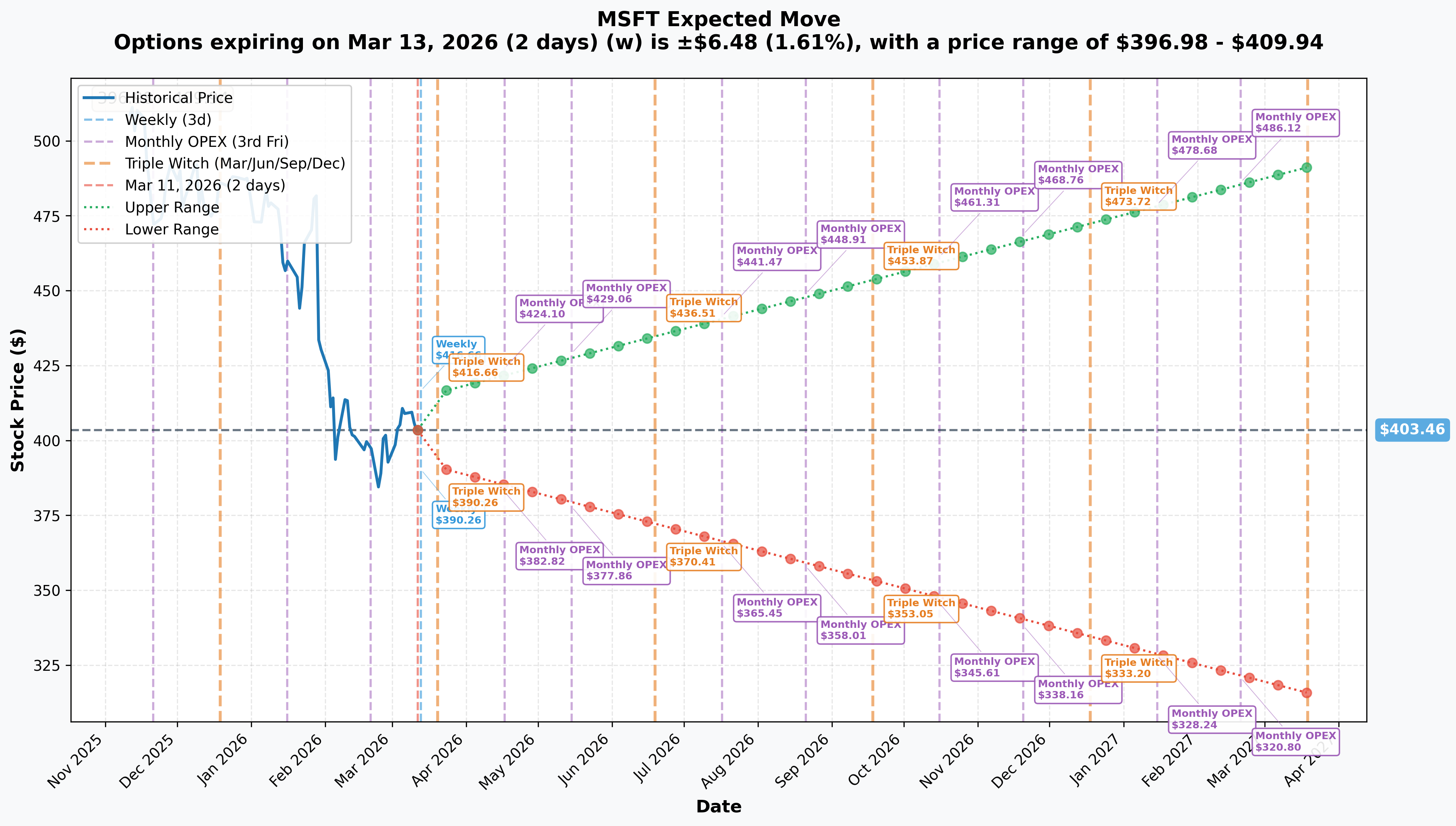

Implied Move Analysis

Options market pricing for upcoming expirations (from current $403.46 base):

- 📅 Weekly (March 13 — 2 days): ±$6.48 (±1.6%) → Range: $396.98 – $409.94

- 📅 Monthly OPEX / Triple Witch (March 20 — 9 days): ±$12.58 (±3.1%) → Range: $390.88 – $416.04

- 📅 April OPEX (April 17): Range $382.82 – $424.10

- 📅 May OPEX (May 15 — first M365 E7 data): Range $377.86 – $429.06

- 📅 June Triple Witch (June 19 — post-Build 2026): Range $370.41 – $436.51

- 📅 October OPEX (October 16): Range $345.61 – $461.31 ← $460 strike enters implied range by October

- 📅 LEAP Expiry (March 19, 2027 — 373 days): ±$87.83 (±21.8%) → Range: $315.63 – $491.29

Translation for regular folks: The market thinks MSFT could reasonably trade anywhere between $315 and $491 by the March 2027 LEAP expiry. The $460 strike sits just inside the upper band of the LEAP implied range at $491.29 — meaning the options market has assigned a non-trivial probability of MSFT reaching the buyer's target zone. By October 2026, the $461 level starts appearing in monthly implied ranges — this trade has a pathway.

Key insight: The LEAP buyer is betting the upper half of the market's own implied range comes to fruition. The breakeven at $494.39 is actually slightly above the LEAP implied upper range of $491.29 — the buyer needs a bit more than what the market implies is the one-standard-deviation move. That's aggressive, but not delusional.

🎪 Catalysts

✅ Recent Catalysts (Already Happened)

Q2 FY2026 Earnings — January 28, 2026 📊

The quarter that broke MSFT momentum. Revenue hit $81.3B (+17% YoY) and Microsoft Cloud crossed $50B for the first time in a single quarter, but the market focused on Azure growth decelerating to 39% (vs. 40% prior quarter) and a 66% YoY spike in capex to $37.5B. The stock got hit for one of the largest single-day market value destructions in U.S. history. But the same report showed commercial backlog exploding 110% to $625B — a number bulls are fixated on.

M365 E7 & Agent 365 Announcement — March 9, 2026 💡

Just two days ago, Microsoft announced M365 E7 at $99/user/month, launching May 1 — a $39/month premium over E5, bundling Copilot and Agent 365. At even 10% conversion of 400M commercial users, that's $4.8B in incremental annual revenue. Pricing has drawn some industry pushback, but the scale of the opportunity is hard to ignore.

Analyst Downgrades (Feb 2026):

Two rare MSFT downgrades in February created selling pressure:

- Stifel downgraded to Hold (Feb 5) with a new $392 target — citing Azure supply issues and Google/Anthropic competition

- Melius Research downgraded to Hold (Feb 9) with $430 target on similar capex/margin concerns

OpenAI Partnership Restructuring (Oct 2025 – Feb 2026):

Microsoft secured 20% of OpenAI's total revenue through 2032 and an incremental $250B of Azure services commitment from OpenAI. Despite Amazon, Nvidia, and SoftBank putting $110B into OpenAI in late February, Microsoft and OpenAI confirmed their partnership remains unaltered on February 27.

🚀 Upcoming Catalysts (Next 6 Months)

Q3 FY2026 Earnings — April 28-29, 2026 (48 DAYS AWAY!) 📊

This is THE binary event for the LEAP call thesis. Consensus expects revenue of $80.65B–$81.75B with Azure growth guided at 37-38%. The critical question: does Azure growth stabilize, or does the deceleration trend continue? If Azure holds at 37-38% and management gives confident forward guidance, this LEAP trade could reprice significantly within 48 days.

Key metrics to watch:

- 🔵 Azure growth CC: Is 37% the floor or still decelerating?

- 🔵 Cloud gross margin: Guided ~65% YoY compression — does it worsen?

- 🔵 Copilot paid seats: Currently 15M, watch for acceleration signal

- 🔵 Q4 FY2026 guidance: Will they signal H2 capex moderation?

M365 E7 / Agent 365 General Availability — May 1, 2026 💰

The most significant product packaging change for Microsoft in years. At $99/user/month, converting even 10% of the ~400M M365 commercial users to E7 would represent ~$4.8B in incremental annual revenue. Early adoption signals in Q3 earnings and post-May commentary will be a massive catalyst for the LEAP position.

Microsoft Build 2026 — June 2-3, 2026 (San Francisco) 🛠️

Microsoft confirmed Build 2026 dates with a "no-fluff" developer-focused event featuring Azure AI, Copilot platform updates, and developer tools. Historically a sentiment-moving event for the stock. This hits 3 months into the LEAP trade runway.

Q4 FY2026 Earnings — Late July 2026

Will capture first ~2 months of M365 E7 live data and full Build 2026 momentum. Critical for validating the AI capex ROI narrative that the market is demanding.

FTC Antitrust Probe (Ongoing, Timeline Uncertain) ⚠️

The FTC is conducting its broadest Microsoft antitrust investigation since the 1990s, examining cloud bundling, the OpenAI relationship, and potential undisclosed merger concerns. Formal charges typically take 12-18+ months — risk exists but is unlikely to crystallize within the LEAP window.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here are the scenarios through the March 19, 2027 LEAP expiry:

📈 Bull Case (30% probability)

Target: $480–$500+

How we get there:

- 💪 Q3 FY2026 earnings (April 28) — Azure growth stabilizes at 37-38% and management signals capex peaking; stock re-rates upward

- 🚀 M365 E7 early adoption exceeds expectations — any signal of enterprise uptake beyond 5% of commercial seats sends analysts scrambling to raise estimates

- 🤖 Copilot paid seat growth accelerates past 20M+ seats — proves monetization works

- 📊 $625B commercial backlog starts converting to revenue at higher rates — RPO velocity becomes the new bull narrative

- 📈 Multiple re-expansion back toward 27-28x forward P/E (from current 21.3x) — just getting to Apple's 32.7x P/E would put MSFT at $700+

- 🎯 Gamma resistance stacks at $430, $440, $450 gradually work off through monthly OPEXs — by October, $461 is within the monthly implied range

- 📅 By Build 2026 (June), developer ecosystem wins and Azure AI wins drive momentum

LEAP P&L in Bull Case:

- Stock at $480 by March 2027: Call worth ~$20 (intrinsic $20 + minimal time value) — loss of ~$14.39/share from $34.39 cost

- Stock at $495 by March 2027: Call worth ~$35 (intrinsic $35) — roughly break-even

- Stock at $530 by March 2027: Call worth ~$70 — gain of ~$35.61/share (~104% ROI)

- Stock at $560 by March 2027: Call worth ~$100 — gain of ~$65.61/share (~191% ROI)

🎯 Base Case (45% probability)

Target: $420–$460 range (gradual recovery)

Most likely scenario:

- ✅ Q3 earnings in-line: Azure 37-38%, cloud margins steady, guidance neutral-to-slightly-positive

- 📊 M365 E7 launch generates early buzz but enterprise adoption takes time — "show me" quarter for investors

- 🔄 Stock gradually works from $403 toward $420-440 as quarterly beats compound and sentiment improves

- ⚖️ FTC probe noise creates periodic pullbacks but no formal action in the next 12 months

- 💤 LEAP expires with stock near $430-450 — option expires worthless or with small residual value (loss on the trade, ~50-80% of premium)

- 📈 Gamma staircase above $405 provides measured resistance; stock grinds higher through each level as quarters pass

Why 45% probability: Microsoft's fundamentals are strong (growing revenue, $625B backlog, AI platform positioning) but the near-term margin compression narrative and Azure deceleration keep a lid on multiple expansion. Recovery takes time, not reaching $494.39 breakeven by March 2027.

📉 Bear Case (25% probability)

Target: $360–$390 (retest lows)

What could go wrong:

- 😰 Q3 earnings disappoint again — Azure growth drops below 37%, margins worse than guided, capex guidance raised further — sentiment collapse

- 🚨 M365 E7 adoption fails — enterprises balk at $39/month premium uplift, conversion rate below 2%, narrative shifts to "Microsoft overpricing its AI"

- ⚖️ FTC formal action or consent decree materializes faster than expected — bundling restrictions would directly hit the E7/Copilot revenue strategy

- 🤖 Copilot conversion rate (currently 35.8% vs ChatGPT's 83.1%) worsens — enterprise AI tool monetization stalls

- 📉 Macro recession or enterprise IT budget freeze delays cloud migration and Copilot adoption

- 💸 DeepSeek-style competitive disruption proves the capex-heavy paradigm wrong — massive writedowns on short-lived GPU assets

- 🎯 Break below $400 gamma support triggers cascade toward $390 implied move floor; next support at $390 from GEX

LEAP P&L in Bear Case:

- Stock at $380 by March 2027: Call expires worthless — loss of $34.39/share, $12.04M total (100% loss)

- Stock at $400 by March 2027: Call expires worthless — full premium loss

💡 Trading Ideas

🛡️ Conservative: MSFT Stock on Pullback — "Sleep Well Strategy"

Play: Buy MSFT shares outright at $400-$405, targeting $440-$460 over the next 6-9 months

Why this works:

- 💰 At 21.3x forward P/E, MSFT is trading at a significant discount to its historical average and peer group (Apple at 32.7x, Alphabet at 27.2x)

- 📊 $625B commercial backlog provides revenue visibility most stocks can only dream about

- 🎯 Strong institutional net buying in Q4 2025 (+33M shares from Vanguard, UBS, SG Americas) shows smart money accumulating the dip

- 🛡️ No leverage, no expiry pressure — let the quarterly earnings cycle work in your favor

- 📅 Mark your calendar for April 28 Q3 earnings as the first key signal

Price targets:

- 🎯 First target: $420 (gap fill from earnings collapse, above $415 gamma resistance)

- 🎯 Second target: $440-$450 (implied move range for June OPEX, first M365 E7 adoption data)

- ⚠️ Stop loss: $388-$390 (break below major implied move support signals thesis is wrong)

Position size: Up to 5-10% of portfolio, scale into pullbacks toward $400

Risk level: Moderate | Skill level: Any level

⚖️ Balanced: April $415 Call Spread — "Earnings Catalyst Play"

Play: Buy MSFT April 17, 2026 $415 Call / Sell MSFT April 17, 2026 $430 Call

Why this works:

- 📅 Expires just before Q3 earnings on April 28 — but you're betting on pre-earnings drift as sentiment improves from M365 E7 announcement catalyst

- 💸 Defined risk spread — you know your max loss on day one

- 🎯 Targets $415-$430 resistance cluster in GEX, which aligns with the April OPEX implied upper range of $424.10

- ⚖️ Selling the $430 call reduces cost and makes the breakeven more achievable than a naked call

- 📊 Net premium: Approximately $3-5 per spread depending on IV levels when entered

Estimated P&L:

- 💰 Max profit: ~$10-12 per spread if MSFT reaches $430+ by April 17 expiry

- 📉 Max loss: ~$3-5 net debit (the spread cost) — defined and limited

- 🎯 Breakeven: approximately $418-$420

- 📊 Risk/Reward: ~2.5:1

Entry timing:

- ⏰ Enter now or on any dip toward $400-$402 support zone

- 🎯 Only if MSFT holds $400 support — if it breaks cleanly, wait for stabilization

Position sizing: Risk only 2-4% of portfolio

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Mirror the LEAP — Scaled-Down $460 Call — "Big Picture Bet"

Play: Buy 5-10 contracts of MSFT March 19, 2027 $460 Call (same as the $12M whale trade, just retail-sized)

Why this could work:

- 🐋 You're literally copying the strategy of someone who just committed $12 MILLION to this exact thesis — they're not dumb with money that size

- 📅 373 days captures ALL the major catalysts: Q3 earnings (April 28), M365 E7 GA (May 1), Build 2026 (June 2-3), Q4 earnings (July), and beyond

- 🤖 The AI/cloud monetization thesis takes time — a LEAP gives it the runway to unfold instead of fighting weekly theta decay

- 📊 $460 strike sits just inside the LEAP implied upper range of $491.29 — the market's own pricing implies it's reachable

- 🎯 If MSFT re-rates back toward peers (Apple at 32.7x P/E), MSFT would trade at $700+; $460 is just a partial re-rating

Estimated P&L (5 contracts = $17,195 at risk):

- 💰 MSFT at $480 by March 2027: ~$20 intrinsic, lose ~$72% of premium

- 🚀 MSFT at $495 by March 2027: ~$35 intrinsic, roughly break-even

- 🔥 MSFT at $540 by March 2027: ~$80 intrinsic, gain ~$45.61/contract × 500 shares = $22,805 profit (133% ROI)

- 💀 MSFT below $460 at expiry: Lose entire $17,195 (100% loss)

CRITICAL WARNINGS:

- ⚠️ The breakeven of $494.39 requires a 23% rally — that's a meaningful move even for MSFT

- ⚠️ LEAPs are not magic — if MSFT drifts sideways to $430-450, you still lose most of your premium at expiry

- ⚠️ Time decay accelerates in the final 90 days — if thesis isn't playing out by December 2026, consider rolling or cutting

- ⚠️ The $12M buyer may have complex portfolio hedging needs or offsetting positions not visible on the tape — do not assume their exact circumstances match yours

- ⏰ Set a calendar reminder at 6 months (September 2026) to re-evaluate — don't hold blindly to expiry if the thesis is clearly broken

Position sizing: Maximum 2-3% of portfolio. This is a defined-risk speculative play, not a core position.

Risk level: High (can lose 100% of premium) | Skill level: Intermediate-Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Azure deceleration continues: Azure growth sliding from 40% → 39% → guided 37-38%. Stifel's Brad Reback warned that "consensus expectations for 2027 are too optimistic" and expects Azure gross margin compression to accelerate. If Azure drops below 35% CC, the entire bull thesis loses its anchor

-

💸 Capex growing faster than revenue: $100-120B+ in FY2026 capex vs. 17% revenue growth is a brutal ratio. Two-thirds of capex goes to short-lived GPU/CPU assets requiring replacement every ~3 years — the depreciation wave has barely started hitting the P&L

-

🤖 Copilot conversion problem: Workplace conversion rate of 35.8% vs. ChatGPT's 83.1% is a real concern. M365 E7 at $99/user/month needs enterprise buyers to believe in AI productivity — if adoption disappoints, the incremental revenue thesis collapses

-

⚖️ FTC antitrust overhang: The broadest Microsoft antitrust investigation since the 1990s is examining cloud bundling and the OpenAI relationship. If the FTC views the OpenAI partnership as an undisclosed merger, forced structural changes could directly undermine the AI revenue strategy

-

🇪🇺 EU/UK regulatory pressure: EU and UK CMA scrutiny of Microsoft's cloud licensing terms could force licensing changes that weaken Azure's competitive pricing in Europe

-

🏔️ $405 gamma wall is a real obstacle: The largest single GEX cluster in the chain sits at $405 (80.1B). Short-term, this is mechanical resistance that market makers will systematically sell into. Breaking through requires sustained institutional buying volume

-

🎰 Pure speculation at $460 strike: The $460 target requires a 14% OTM move just to reach the strike, plus another 8%+ to reach breakeven — 23% total. If the stock ends anywhere below $460 at March 2027 expiry, the option expires worthless. This is a defined-risk, high-conviction bet where "mostly right" still means "full loss"

-

📊 Insider selling trend: CEO Satya Nadella, Vice Chair Bradford Smith, and CEO Commercial Judson Althoff all sold shares in recent months. Insider selling doesn't guarantee stock decline, but it's a data point worth monitoring

🎯 The Bottom Line

Real talk: Someone just committed $12M to a year-long call on Microsoft at a 14% OTM strike, with a $494.39 breakeven. That's not a bet you make unless you have strong conviction in the AI/cloud monetization story playing out over the next 12 months. And the case is legitimate — MSFT is trading at a 5-year relative low in valuation terms (21.3x forward P/E), sitting on $625B in commercial backlog, with multiple major catalysts stacked between now and March 2027.

What the $12M trade is telling us:

- 🎯 Sophisticated buyer sees Q3 earnings (April 28), M365 E7 GA (May 1), and Build 2026 (June 2-3) as the catalyst sequence that breaks MSFT out of its post-earnings malaise

- 💰 At $34.39/contract vs. $402.70 stock, they're paying 8.5% of stock price for 373 days of call exposure — and they chose LEAP over stock, meaning they want maximum leverage on the recovery move

- 📊 The Vol/OI ratio of 9.16x confirms this is FRESH positioning — they opened this today with conviction, not rolling an existing position

- 🏔️ The $460 strike is just inside the LEAP market-implied range — this is aggressive but not irrational

If you're bullish on MSFT:

- ✅ Stock position (most conservative): Buy shares at $400-$403, target $440-$460, stop $388

- 📊 April spread (tactical): $415/$430 call spread captures the April pre-earnings drift

- 🚀 LEAP copy (aggressive): 5-10 contracts of the March 2027 $460 call for a scaled-down version of the whale trade

If you're waiting on the sidelines:

- ⏰ April 28-29 is your first major decision point — Q3 earnings will make or break the near-term narrative

- 📅 May 1 M365 E7 launch data starts flowing — watch for early enterprise adoption signals

- 🎯 If MSFT tests $400 again and holds, that's historically strong gamma support — it's been a reliable floor

If you're skeptical:

- 🐻 Don't short into $400 gamma support — that's fighting market maker positioning

- 📉 Better bear setup: If MSFT breaks $398-$399 with volume, THEN consider April puts targeting $390, tight stop $408

- ⏰ The real bear case needs Azure growth to drop below 35% — watch April earnings for that signal

Mark your calendar:

- 📅 March 20, 2026 — Triple Witch OPEX (±$12.58 implied move, stock range $390.88–$416.04)

- 📅 April 17, 2026 — Monthly OPEX

- 📅 April 28-29, 2026 — Q3 FY2026 Earnings (THE big event for this trade)

- 📅 May 1, 2026 — M365 E7 / Agent 365 General Availability

- 📅 June 2-3, 2026 — Microsoft Build 2026, San Francisco

- 📅 March 19, 2027 — LEAP expiration

Final verdict: This is a high-conviction, patient bet on Microsoft's AI and cloud monetization narrative — made by someone sizing up at what may be the cheapest MSFT has been relative to its peers in years. The trade is aggressive. The $460 strike needs 23% just to start paying off. But 12 months is a long time, and between Q3 earnings, M365 E7 adoption, and Build 2026, the catalyst calendar is stacked. The risk is real — miss the catalysts or see Azure growth crater, and the option expires worthless. But if Microsoft executes, this LEAP could return multiples on its premium.

Be patient. Size right. Watch the April earnings carefully.

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. The EXTREMELY_UNUSUAL z-score and 9.16x Vol/OI ratio reflect this specific trade's size relative to recent MSFT option history — it does not imply the trade will be profitable or that you should replicate it. LEAP options can expire completely worthless if the underlying stock does not reach the strike price by expiration. Always conduct your own due diligence and consider consulting a licensed financial advisor before making any investment decisions. Options strategies involve complex risks including, but not limited to, the potential for 100% loss of premium paid.

About Microsoft Corporation: Microsoft develops and licenses consumer and enterprise software, operating systems, cross-device productivity applications, and cloud services. Known for Windows, Microsoft 365, Azure cloud, Copilot AI, Xbox gaming, and LinkedIn. Market cap: $3.01 Trillion, traded on NASDAQ.