🐋 ORCL: Someone Just Deployed a $43M Put Spread 4 Days Before Earnings!

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A massive $43M bull put spread just hit the Oracle tape -- selling 6,319 June $180 puts ($22M) and buying 18,543 June $135 puts ($21M) -- all in a single clip at 10:40 AM with the stock at $158. With z-scores of 15.05 and 8.88 (you might see trades this large a handful of times per year), someone is making a major pre-earnings bet that Oracle holds up through its Q3 report on March 10 -- just 4 days from now. This is not your neighbor's Robinhood account.

🏢 Company Snapshot

Oracle Corporation (NYSE: ORCL) -- The enterprise software giant that quietly became one of the biggest plays in the AI infrastructure boom. With a $445B market cap and 162,000 employees, Oracle is best known for its database business but has pivoted hard into cloud computing via Oracle Cloud Infrastructure (OCI). Classified under Prepackaged Software (SIC 7372), the company is now a key partner in OpenAI's $300B Stargate data center project and has cloud deals with Meta, Nvidia, xAI, and more. The stock trades at ~$158, down about 21% YTD from its December highs as investors weigh massive AI infrastructure spending against near-term margins.

💰 The Option Flow Breakdown

📊 The Tape

| Field | Leg 1 (Short Put) | Leg 2 (Long Put) |

|---|---|---|

| 🕐 Time | March 6, 10:40:03 AM ET | March 6, 10:40:03 AM ET |

| 📌 Ticker | ORCL | ORCL |

| 📞 Type | PUT $180 (Sell) | PUT $135 (Buy) |

| 🎯 Strike | $180 (13.8% above spot) | $135 (14.6% below spot) |

| 📅 Expiration | 2026-06-18 (104 days out) | 2026-06-18 (104 days out) |

| 📦 Size | 6,319 contracts | 18,543 contracts |

| 💵 Premium | $22M (received) | $21M (paid) |

| 🏷️ Execution | MID price -- Sell to Open | MID price -- Buy to Open |

| 📊 Volume / OI | 6,500 / 5,500 (Vol/OI: 1.18x) | 19,000 / 21,000 (Vol/OI: 0.91x) |

| 🔢 Z-Score | 15.05 (Extremely Unusual) | 8.88 (Extremely Unusual) |

| 💲 Option Price | $34.20 | $11.08 |

| 🧩 Strategy | Bull Put Spread -- Short leg | Bull Put Spread -- Long leg |

🤓 What This Actually Means

Let me break this down in plain English.

At exactly 10:40 AM, someone executed a two-legged put spread on Oracle -- selling $180 puts and buying $135 puts, both expiring June 18. The net effect is a bull put spread that collects roughly $1M in net credit (the $22M received from selling the 180 puts minus $21M paid for the 135 puts).

Here is why this trade is so remarkable:

✅ Absolutely massive size -- The short leg has a z-score of 15.05, meaning this trade is over 15 standard deviations above the average trade size. The long leg clocks in at 8.88x. Trades this large happen maybe a few times per year in ORCL options. This is institutional money, period.

✅ Both legs hit at the exact same second -- 10:40:03 AM on both sides. This is a structured spread, not two separate trades. The simultaneous execution and MID fills scream institutional execution desk.

✅ The timing is everything -- Oracle reports Q3 FY2026 earnings on March 10, after the close. That is 4 days away. This $43M spread is almost certainly pre-earnings positioning.

✅ Deep in-the-money short put -- The $180 strike is 13.8% above the current stock price of $158. Selling a deep ITM put at $34.20 means the trader is collecting substantial premium but also taking on significant assignment risk. They are effectively saying: "I am comfortable owning Oracle at $180 minus the premium collected."

✅ Wide $45 spread -- The distance between the $180 short put and the $135 long put creates a $45-wide spread. Max risk per spread is $45 minus the net credit. The $135 long put is a disaster insurance policy -- it caps losses if Oracle somehow craters below $135 (a 14.6% drop from here).

So what is the thesis?

This trade structure collects premium from selling rich pre-earnings implied volatility. The trader profits if Oracle stays anywhere above $135 by June 18, with maximum profit if the stock is above $180 at expiration. Given that ORCL is currently at $158, the stock would need to rally 14% just to reach the short strike -- but the trader still profits in a range of outcomes because they collected a net credit.

The real edge here: earnings IV crush. Options are expensive right now because of the March 10 earnings event. After earnings pass, implied volatility will collapse, and the spread's value drops -- which benefits the trader who sold it. This is a classic institutional premium-selling play ahead of a known catalyst.

📈 Technical Setup / Chart Check-Up

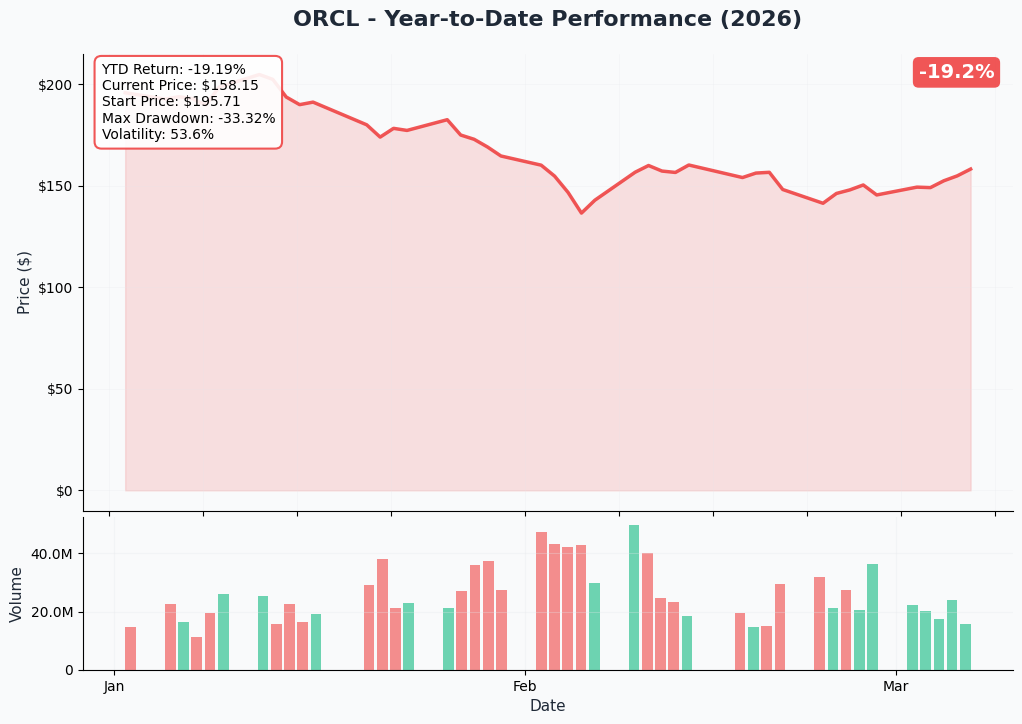

YTD Chart

Oracle has been through the wringer in 2026. The stock is down roughly 21% YTD from its December highs near $200, largely pressured by concerns over massive AI infrastructure spending (CapEx now expected at $50B for FY2026) and negative $10B free cash flow in Q2. Still, the pullback has brought the stock to a level where several analysts see deep value -- the consensus price target sits at ~$279, implying roughly 77% upside from current levels.

Key technical levels to watch:

📉 21% YTD drawdown -- The stock has been in a persistent downtrend since the December highs. Momentum is negative, and the stock is trading below major moving averages.

📈 $155-$158 current zone -- Oracle is sitting right at a potential inflection point. Earnings on March 10 will determine whether this becomes a floor or a trapdoor.

📉 $135-$140 as a worst-case floor -- This lines up with the long put leg of today's whale trade and major gamma support below.

📈 $170-$180 as the recovery target -- If earnings deliver, the stock could reclaim a chunk of its YTD losses. The $180 short put strike marks the trader's profit-maximization level.

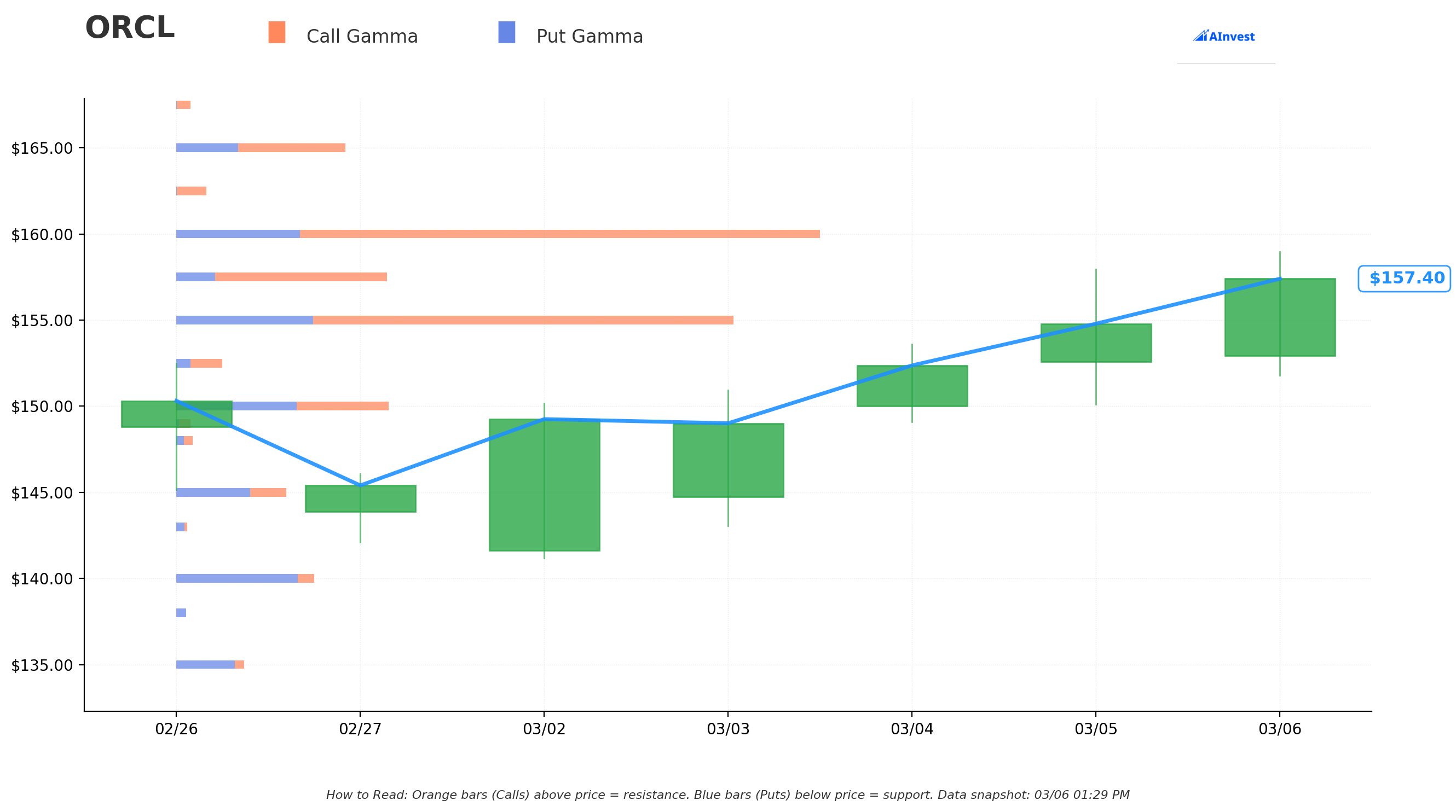

🔵🟠 Gamma-Based Support & Resistance

How to read this chart: The blue bars (put gamma) below the current price act as support floors -- heavy options activity that tends to slow down declines. The orange bars (call gamma) above the current price act as resistance ceilings -- strikes where hedging pressure can cap rallies. Bigger bars mean stronger levels.

Current Price: $158.11

🔵 Support Levels (Below Price):

- $157.50 -- Immediate support just 0.4% below, with $14B total gamma exposure. This is the nearest floor and is holding right now.

- $155 -- Strong support at $30B total gamma (2% below). A meaningful concentration of put open interest lives here.

- $150 -- Secondary floor at $11.3B gamma (5.1% below). Psychological round number with put gamma exceeding call gamma here (net negative GEX = dealers sell into declines, creating gravity).

- $140 -- Deep support at $9B gamma (11.5% below). This is the "worst-case pre-earnings" floor.

🟠 Resistance Levels (Above Price):

- $160 -- First and strongest resistance at a massive $51.7B total gamma. This is THE level to watch. Just 1.2% overhead. A breakout above $160 could trigger dealer hedging flows that accelerate the move.

- $165 -- Secondary resistance at $11.5B gamma (4.4% above).

- $170 -- Significant resistance at $18.9B gamma (7.5% above). Getting through this zone would signal a real recovery.

- $175 -- Lighter resistance at $8B gamma (10.7% above).

- $180 -- Notable resistance at $18.1B gamma (13.8% above). This aligns perfectly with the whale's short put strike.

Net GEX Bias: Bullish (Total call gamma $172.1B vs put gamma $105.0B). Overall dealer positioning leans bullish, suggesting the path of least resistance is higher if the stock can clear $160.

Note: Gamma levels are dynamic and shift as new trades open and close. These represent the current snapshot.

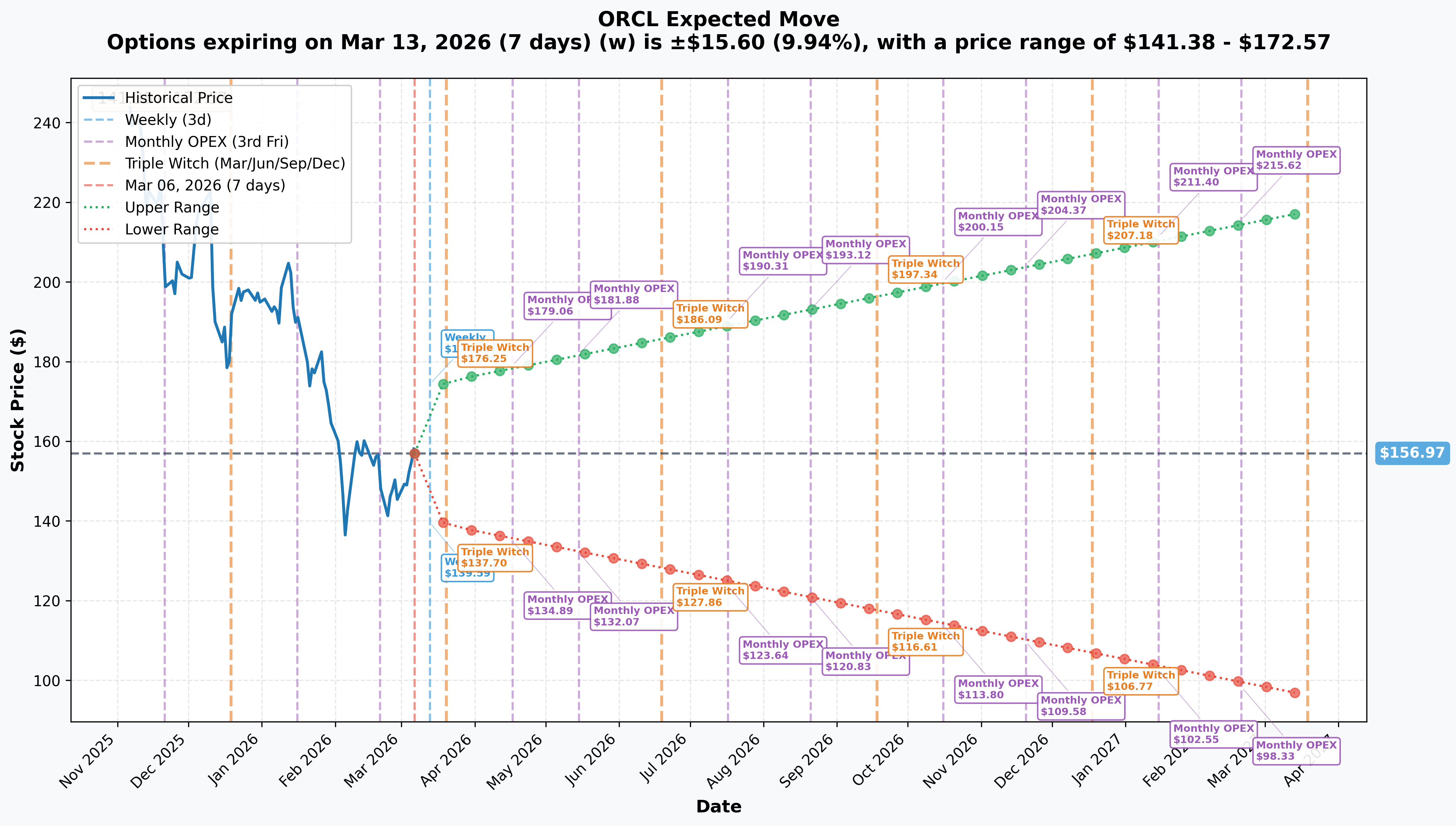

📐 Implied Move Analysis

The options market is pricing in some serious fireworks around earnings. Here is what the implied move data tells us:

| Timeframe | Expiration | Expected Range | Move % |

|---|---|---|---|

| 📅 Weekly (Earnings!) | 2026-03-13 | $141.38 - $172.57 | +/- 9.9% |

| 📅 Monthly OPEX / Triple Witch | 2026-03-20 | $138.87 - $175.08 | +/- 11.5% |

| 📅 April OPEX | 2026-04-17 | $134.89 - $179.06 | +/- 14.1% |

| 📅 June Triple Witch (THIS TRADE!) | 2026-06-19 | $127.86 - $186.09 | +/- 18.6% |

Translation for us regular folks:

The market expects Oracle could swing nearly 10% in either direction just from the earnings report alone. That is a roughly $15.60 move from the current $157 level, putting the one-week range at $141 to $173.

For the June 19 expiration (the closest standard expiry to this trade's June 18 date):

📈 Implied upside: $186.09 -- The whale's short put at $180 sits within the implied upper range. The options market says reaching $180 by June is totally plausible.

📉 Implied downside: $127.86 -- Even the worst-case implied scenario sits below the $135 long put protection. The whale's downside hedge at $135 captures the vast majority of the expected distribution.

Key insight: The weekly 9.9% implied move is elevated because of earnings on March 10. Once earnings pass and IV crushes, the June spread should benefit significantly -- exactly how an institutional premium-selling trade is designed to work.

🎪 Catalysts

📅 Upcoming (The Big Ones)

| Date | Event | Why It Matters |

|---|---|---|

| March 10 🔥 | Q3 FY2026 Earnings (after close) | THE catalyst. Consensus: revenue $16.9B (+20% YoY), EPS $1.71. Cloud growth guided 37-41% CC. This report determines everything. |

| March 10, 4 PM CT | Q3 Earnings Conference Call | Focus on cloud bookings, AI infrastructure capacity ramp, RPO growth, and FY2026 guidance update |

| March 17-18 | FOMC Meeting | Fed expected to hold rates. Macro sentiment driver for all tech |

| March 20 | Triple Witching OPEX | Massive options expiration event -- could amplify post-earnings moves |

| June 18 | THIS TRADE EXPIRES | 104 days for the thesis to play out |

✅ Already Happened (Recent)

📊 Q2 FY2026 Results (December 10, 2025) -- Mixed bag: Non-GAAP EPS $2.26 crushed the $1.50 consensus (beat by 37.8%), but revenue of $16.1B came in slightly below expectations. Cloud revenue surged 33% to $8B. The stock initially rallied but has given it all back and then some.

🏗️ CapEx Explosion -- Oracle now expects CapEx of ~$50B in FY2026, up $15B from prior guidance, as it races to build AI data center capacity. Free cash flow swung to negative $10B in Q2 -- and that is what spooked investors.

📈 Q3 Guidance Was Actually Strong -- Management guided Q3 revenue to $16.8-$17.1B vs $16.2B Street consensus, and EPS $1.70-$1.74 vs $1.50 consensus. Cloud revenue growth guided to 37-41% in constant currency. The company basically told the Street: "We're going to beat your numbers."

🤝 Stargate Partnership -- Oracle is a key infrastructure partner in OpenAI's $300B Stargate project, building 4.5 GW of data center capacity with construction underway in Texas, New Mexico, Wisconsin, and Michigan.

📊 RPO Surged to $523B -- Remaining performance obligations jumped $68B sequentially in Q2, driven by new commitments from Meta, Nvidia, and others. This massive backlog is future revenue waiting to be recognized.

📉 Analyst Target Cuts -- RBC Capital lowered its target to $160 (Hold) on March 4. Evercore ISI cut to $220 from $275 (Outperform) on March 5. Morgan Stanley slashed to $213 from $320 (Equal-Weight). The Street is recalibrating for the CapEx-heavy reality.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, the catalyst calendar, and analyst targets, here are the scenarios through the June 18, 2026 expiration:

🚀 Bull Case: $175 - $186 (+11% to +18%)

How we get there:

- 📊 Q3 earnings on March 10 deliver on the strong guidance -- revenue above $17B, cloud growth 37%+ in CC, and RPO continues to climb

- 📈 Market re-focuses on the $523B RPO backlog and OCI growth trajectory rather than near-term CapEx drag

- 🤝 Management provides upbeat FY2027 commentary on the Stargate ramp and new cloud customer wins

- 📈 Stock breaks through $160 gamma resistance, triggering dealer hedging flows that push it toward $170, then $175-$180

- 📊 The implied move upper range for June sits at $186.09 -- achievable with sustained positive sentiment

What this means for the whale trade: Maximum profit. The $180 short puts expire worthless (or near it), the $135 long puts are deep OTM, and the entire net credit is kept. Full win.

Probability: ~30% -- Requires earnings to meet or beat the already-raised guidance and macro cooperation.

⚖️ Base Case: $150 - $170 (-5% to +8%)

Most likely scenario:

- ✅ Earnings meet consensus but do not blow away expectations -- revenue ~$16.9B, EPS ~$1.71

- 📊 Cloud growth is solid but investors remain focused on free cash flow burn and $50B CapEx

- 🔄 Stock bounces modestly post-earnings, grinds in the $155-$170 range as the market digests the numbers

- ⚖️ Analyst upgrades trickle in slowly as the discount to the $279 average price target becomes harder to ignore

- 📈 Gamma support at $155-$157 holds on any post-earnings dip

What this means for the whale trade: Still profitable. As long as Oracle stays above $135 by June 18, the long puts expire worthless and the trade works. Even if the stock is at $155, the $180 short puts have significant intrinsic value but the post-earnings IV crush reduces the spread's mark-to-market cost, allowing the trader to potentially close at a profit before expiration.

Probability: ~45% -- The most likely path. Oracle delivers decent numbers, the stock stabilizes, and the premium-selling trade benefits from time decay and IV crush.

🐻 Bear Case: $135 - $150 (-15% to -5%)

What could go wrong:

- 😰 Q3 earnings miss on revenue or cloud metrics -- even a slight miss after the strong guidance would be punishing

- 📉 Management lowers FY2026 or FY2027 guidance due to data center construction delays or customer pushback

- 💸 Free cash flow remains deeply negative, spooking investors about balance sheet sustainability

- 📉 Broader tech selloff or tariff escalation compounds the damage

- 📊 Stock breaks below $155 gamma support, testing $150, with $140 as the next major floor

What this means for the whale trade: Painful but contained. The $135 long put caps the maximum loss. If Oracle drops to $140, the spread is taking a significant hit but the loss is defined by the spread width ($45) minus the net credit collected.

Probability: ~25% -- Would require an earnings miss on a quarter where management pre-guided above consensus, plus negative macro. Possible but not the base case.

💡 Trading Ideas

🛡️ Conservative: "The Post-Earnings Premium Collector" -- Bull Put Spread

Structure: Sell ORCL $145 put / Buy ORCL $135 put, 2026-04-17 expiration

Why this works: You wait until after March 10 earnings to enter. Once the report is out and the dust settles, you sell a put spread below the gamma-supported levels. The $145 strike sits below the $150 gamma support and the implied move lower range ($138.87 for monthly OPEX). You are betting Oracle does not crater below $145 after earnings -- a level that would require a 8%+ decline from current prices in addition to whatever the earnings move brings.

📊 Estimated credit: ~$1.50-$2.00 per spread 📊 Max risk: ~$8.00-$8.50 per spread 📊 Max profit: Premium collected (if ORCL stays above $145) 📊 Win probability: ~70-75% 📊 Best for: Traders who want exposure to Oracle's post-earnings stabilization without taking directional risk into the report

Pro tip: Enter this trade on March 11 (the day after earnings) once you see the stock's reaction. If Oracle gaps higher, you can sell even more aggressively. If it gaps lower, reassess the strikes.

⚖️ Balanced: "Ride the Recovery" -- Call Debit Spread

Structure: Buy ORCL $160 call / Sell ORCL $175 call, 2026-06-18 expiration

Why this works: This mirrors the bullish thesis behind the whale trade but uses calls instead of puts to participate in the upside. The $160 strike sits right at the strongest gamma resistance -- if Oracle breaks through post-earnings, dealer hedging flows could accelerate the move. The short $175 call caps your risk at a $15-wide spread while targeting the upper gamma zone.

📊 Estimated cost: ~$4.50-$6.00 per spread 📊 Max profit: ~$9.00-$10.50 per spread (at $175+) 📊 Breakeven: ~$164.50-$166 📊 Risk/reward: Roughly 1:2 📊 Best for: Traders who believe earnings will be the catalyst for Oracle to start recovering from its 21% YTD decline. The June expiration gives 104 days -- plenty of time for the recovery to develop.

🚀 Aggressive: "The Earnings Lotto" -- Long Call

Structure: Buy ORCL $165 call, 2026-03-20 expiration (14 days)

Why this works (and why it is risky): Pure directional bet on a strong earnings reaction. The weekly implied move is 9.9% -- that translates to roughly $173 on the upside. If Oracle crushes earnings and the stock gaps above $165 (only a 4.3% move), this call could double or triple overnight. The March 20 Triple Witch expiration captures the earnings event plus one week of follow-through.

📊 Estimated cost: ~$3.00-$4.00 per contract 📊 Breakeven: ~$168-$169 📊 Max profit: Unlimited (but realistically $175-$180 would yield $10-$15 per contract) 📊 Risk: 100% of premium if ORCL stays below $165 after earnings 📊 Best for: Traders with high conviction that the pre-guided Q3 results will trigger a significant re-rating. Only risk what you can afford to lose completely. This is not a "sleep well at night" trade.

Real talk: With the stock already down 21% YTD and management having guided Q3 above consensus, the bar for a positive reaction is not impossibly high. But options are pricing in a 10% move -- so the market already expects fireworks. You need a move beyond expectations to profit, not just a good quarter.

⚠️ Risk Factors

❗ Earnings Are 4 Days Away -- This Is a Binary Event -- Oracle reports March 10 after the close. Any position you take right now is essentially an earnings bet. Even the June-dated whale trade will see a massive mark-to-market swing on March 11. If you cannot stomach a 10%+ gap in either direction, wait until after the report.

❗ $50B CapEx and Negative Free Cash Flow -- Oracle's AI infrastructure buildout is burning cash at an alarming rate. Free cash flow was negative $10B in Q2. The company plans to raise $45-50B in debt and equity in 2026 to fund this. If investors lose confidence in the ROI on this spending, the stock could drop further regardless of revenue growth.

❗ Cloud Competition Is Fierce -- Oracle remains a distant #4 in cloud behind AWS, Azure, and GCP. While OCI is growing fast (cloud infrastructure revenue up 68% in Q2), maintaining this growth rate against entrenched competitors requires flawless execution.

❗ Analyst Downgrades Are Piling Up -- Morgan Stanley cut to $213, RBC to $160, Evercore ISI to $220. Three target cuts in three days heading into earnings is not a great look. Even though the average target is still far above the stock price, the direction of revisions matters.

❗ Negative Momentum -- The stock is down 21% YTD and trading well below moving averages. Stocks in sustained downtrends can continue falling even after decent earnings reports. The market may need several quarters of proof before re-rating Oracle higher.

❗ Customer Concentration Risk -- Oracle's cloud growth is heavily dependent on a handful of mega-customers (OpenAI, Meta, Nvidia, xAI). If any of these relationships cool or deployment timelines slip, the revenue impact could be significant.

❗ Macro and Tariff Headwinds -- Broader tech has struggled in 2026 amid tariff uncertainty and rotation concerns. Oracle is not immune to these macro forces, which could dampen even a strong earnings reaction.

🎯 The Bottom Line

Here's the deal: An institutional player just put $43M to work on a bull put spread in Oracle, 4 days before one of the most important earnings reports the company has had in years. The structure is classic institutional premium-selling -- collect rich pre-earnings IV, let time decay and IV crush do the heavy lifting, and define the risk with a wide protective put below.

The timing is not random. Oracle's management told the Street that Q3 would come in above consensus (revenue $16.8-$17.1B vs $16.2B, EPS $1.70-$1.74 vs $1.50). Cloud revenue growth was guided at 37-41% in constant currency. The RPO backlog surged to $523B. And the stock is 21% cheaper than where it started the year, trading at a massive discount to the $279 average analyst target.

If you are bullish on Oracle: Mark your calendar for March 10 after the close. If Oracle delivers on the pre-guided Q3 numbers, watch whether the stock can break through the $160 gamma resistance wall. A confirmed close above $160 is your green light. The call debit spread ($160/$175, June expiration) is the most sensible way to play the recovery thesis.

If you are on the sidelines: Wait for the earnings report. Do not guess. Oracle has guided above consensus, but the stock is down 21% for a reason -- $50B CapEx and negative free cash flow are real concerns. Let the market tell you how it feels about Q3 results before committing capital.

If you are bearish: The $155 gamma support and $150 round number are your levels to watch. A post-earnings break below $150 would signal the market needs more time (and lower prices) to get comfortable with Oracle's infrastructure spending. Put spreads below $145 give you defined-risk downside exposure.

The whale trade tells us one thing clearly: Sophisticated money believes Oracle at $158, with a $523B backlog, 37-41% cloud growth guidance, and earnings that management already pre-guided above consensus, is not going to collapse. They are selling premium, collecting the credit, and betting on mean reversion. Whether they are right depends on what we hear on March 10.

Four days. $43 million. The clock is ticking. 👀

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Options trading involves significant risk of loss. Always do your own research and consider your risk tolerance before entering any trade. Past unusual options activity is not a reliable predictor of future stock price movement.

About Oracle Corporation: Oracle Corporation delivers enterprise applications and cloud infrastructure offerings, including Oracle Cloud Infrastructure (OCI) for AI workloads. Founded in 1977, headquartered in Austin, TX, with a market cap of $445B and 162,000 employees in the Prepackaged Software industry.