💊 PFE: Someone Just Dumped $5.4M in Calls -- Capping Pfizer's Upside at $28!

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A single seller just unloaded 38,301 PFE $28 call contracts expiring 2026-09-18, collecting roughly $5.4M in premium in one shot -- executed at the mid price. With a z-score of 73.65 (about 73 standard deviations above average trade size), this is an extraordinarily rare trade you might see once or twice a year in PFE options. The $28 strike sits right at the analyst consensus target, and with volume running 8.5x open interest, this is a brand new position opening. Translation: a big player is betting Pfizer stays below $28 through September -- and getting paid handsomely to wait.

🏢 Company Snapshot

Pfizer Inc. (NYSE: PFE) -- One of the world's largest pharmaceutical companies with a $151.3B market cap and roughly 75,000 employees. Headquartered in New York City, Pfizer is classified under Pharmaceutical Preparations (SIC 2834) and generates annual revenue of roughly $60B from prescription drugs and vaccines. Top products include the pneumococcal vaccine Prevnar 13 and cardiology drugs Vyndaqel and Eliquis. International sales represent about 40% of the total, with emerging markets as a major contributor.

The stock currently trades around $26.49, deep in recovery mode after the post-COVID revenue cliff. The big story right now: Pfizer is pivoting hard into GLP-1/obesity (the hottest space in pharma) with its PF-3944 monthly injectable and the recent $10B Metsera acquisition, while also pushing an ambitious oncology pipeline.

💰 The Option Flow Breakdown

📊 The Tape

| Field | Detail |

|---|---|

| 🕐 Time | March 6, 12:17 PM ET |

| 📌 Ticker | PFE |

| 📞 Type | CALL $28 (Sold) |

| 🔻 Direction | SELL -- Premium collection |

| 🎯 Strike | $28 (5.7% above spot) |

| 📅 Expiration | 2026-09-18 (196 days out) |

| 📦 Size | 38,301 contracts |

| 💵 Premium Collected | ~$5.4M ($1.40 per contract) |

| 🏷️ Execution | MID price -- SELL to OPEN |

| 📊 Volume / OI | 85,000 / 10,000 (Vol/OI Ratio: 8.5x) |

| 🔢 Z-Score | 73.65 (Extremely Unusual) |

| 🧩 Strategy | Short Call / Covered Call -- Standalone, new position |

🤓 What This Actually Means

Let me break this down in plain English.

Someone walked up to the options market at 12:17 PM and sold over 38,000 call contracts on Pfizer in a single clip. At $1.40 per contract (times 100 shares each), they collected $5.4M in premium -- money that goes straight into their pocket as long as PFE stays below $28 by September 18.

A few things make this stand out:

✅ Size is off the charts -- This trade has a z-score of 73.65, meaning it is roughly 73x the standard deviation of normal PFE trade sizes. Volume ran at 85,000 contracts against just 10,000 in open interest -- that is an 8.5x Vol/OI ratio. This is not your neighbor selling a few covered calls on Robinhood.

✅ Executed at mid -- The seller hit the midpoint of the bid-ask spread, a hallmark of institutional negotiation. Patient, sophisticated execution.

✅ Sell-to-Open (new position) -- The 8.5x Vol/OI ratio confirms this is a fresh position, not closing an existing trade. Someone is initiating a bet that PFE's upside is capped.

✅ Strike at consensus target -- The $28 strike aligns almost perfectly with the analyst average price target of ~$27-$28. This seller is essentially saying: "I agree with the Street -- Pfizer isn't going much higher than $28 through September. Pay me to take that bet."

✅ Income math -- If this is a covered call against a long stock position (the most likely interpretation given the size), the $1.40 premium on a ~$26.49 stock generates roughly 5.3% income over 6 months, or about 10% annualized. That is attractive yield on a pharma stock already paying a ~6% dividend.

✅ Two likely scenarios:

- 🛡️ Covered call (most likely): The seller owns

3.83 million shares of PFE ($101M position) and is writing calls against it. They're happy to collect income and would sell at $28 if called away -- locking in a ~5.7% capital gain plus the $1.40 premium plus dividends. Total return target: ~17-18% annualized. Smart money income play. - 📉 Naked short call (less likely but possible): Pure premium collection bet that PFE stays below $28. Higher risk, but with the stock trading at a Hold consensus and limited catalyst upside before September, the trade has favorable odds.

📈 Technical Setup / Chart Check-Up

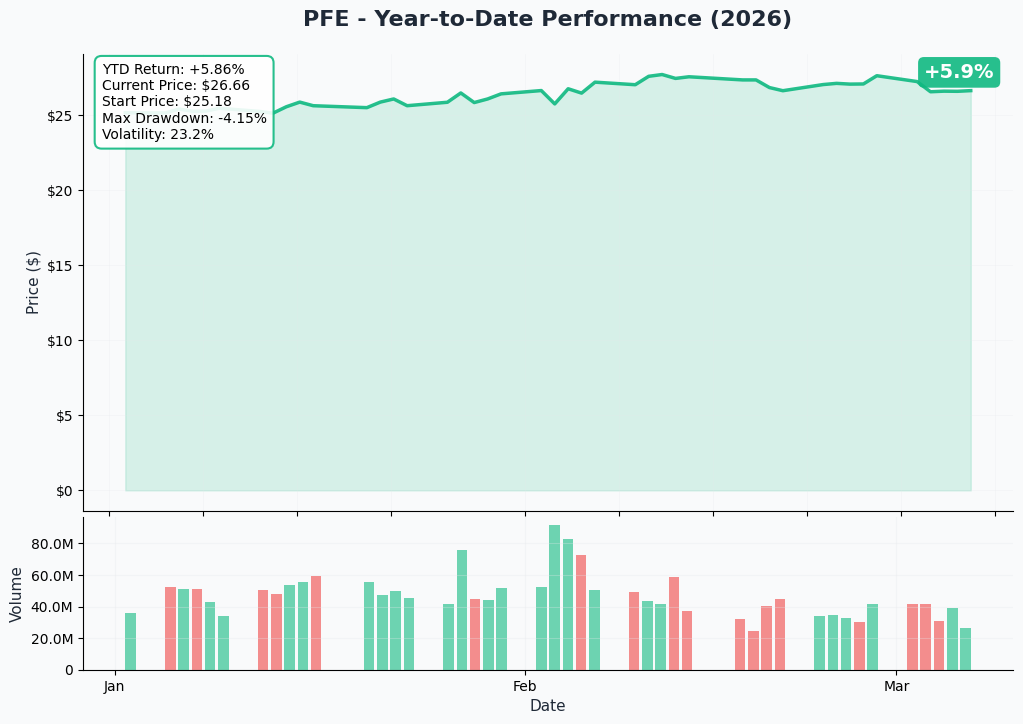

YTD Chart

PFE has been grinding sideways in a relatively tight range, trading between roughly $25 and $28 for most of the past year. The stock is up modestly from its 2025 lows but still well below the pre-COVID highs above $50. The narrative has shifted from COVID windfall decline to "show me the GLP-1 pipeline" -- and the market is waiting for proof.

Key technical levels to watch:

📈 Immediate resistance: $27-$28 -- This is the zone where the stock has repeatedly stalled. The $28 strike on today's massive call sell reinforces this as a ceiling.

📉 Immediate support: $26-$26.50 -- The stock is sitting right on this level. A break below opens the door toward $25.

📊 Trading range: $25-$28 -- PFE has been rangebound, and today's trade is a bet that this continues through September.

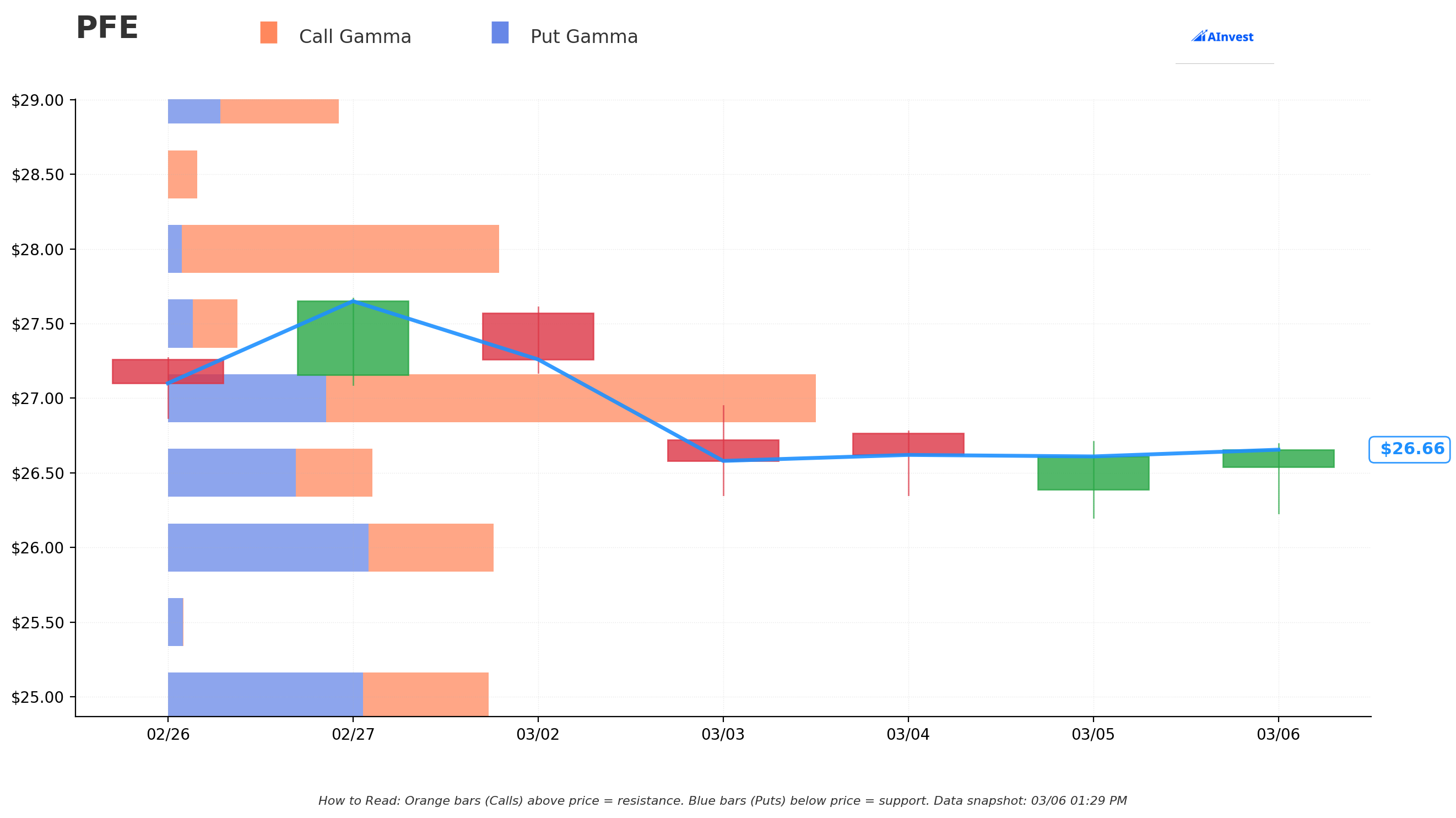

🔵🟠 Gamma-Based Support & Resistance

How to read this chart: The blue bars (put gamma) below the current price act as support floors -- heavy options activity that tends to slow down declines. The orange bars (call gamma) above the current price act as resistance ceilings -- strikes where hedging pressure can cap rallies. Bigger bars mean stronger levels.

Current Price: $26.63

🟠 Resistance Levels (Call Gamma Above Price):

- $27.00 -- Strongest resistance with a massive 131.7B total gamma exposure (just 1.4% overhead). This is a wall. Net GEX of +69.3 means dealer hedging will actively resist moves above $27. Getting through this level is the first challenge for any rally.

- $28.00 -- Secondary resistance at 67.8B total gamma (5.1% above). This is exactly where today's whale sold calls. The combination of call gamma resistance + 38,000 new short call contracts makes $28 a formidable ceiling.

- $29.00 -- Extended resistance at 35.0B gamma (8.9% above).

- $30.00 -- Far resistance at 45.2B gamma (12.7% above). Breaking here would require a major catalyst like a GLP-1 data blowout.

🔵 Support Levels (Put Gamma Below Price):

- $26.50 -- Immediate support with 43.6B total gamma (less than 0.5% below -- very tight floor!).

- $26.00 -- Strong support at 68.1B total gamma (2.4% below). The highest absolute gamma concentration below price.

- $25.00 -- Major structural support at 66.1B gamma (6.1% below). This is the line in the sand.

- $24.00 -- Extended floor at 13.2B gamma.

Net GEX Bias: Bullish -- Total call gamma (351.4B) exceeds total put gamma (221.2B), which means dealer positioning supports the stock staying near current levels or grinding modestly higher. However, the dominant $27 call gamma wall suggests the upside is capped in the near term -- perfectly aligned with the short call thesis.

What this means: PFE is boxed in between strong support at $26 and heavy resistance at $27-$28. The gamma profile supports a rangebound outcome -- which is exactly what the $5.4M call seller is betting on.

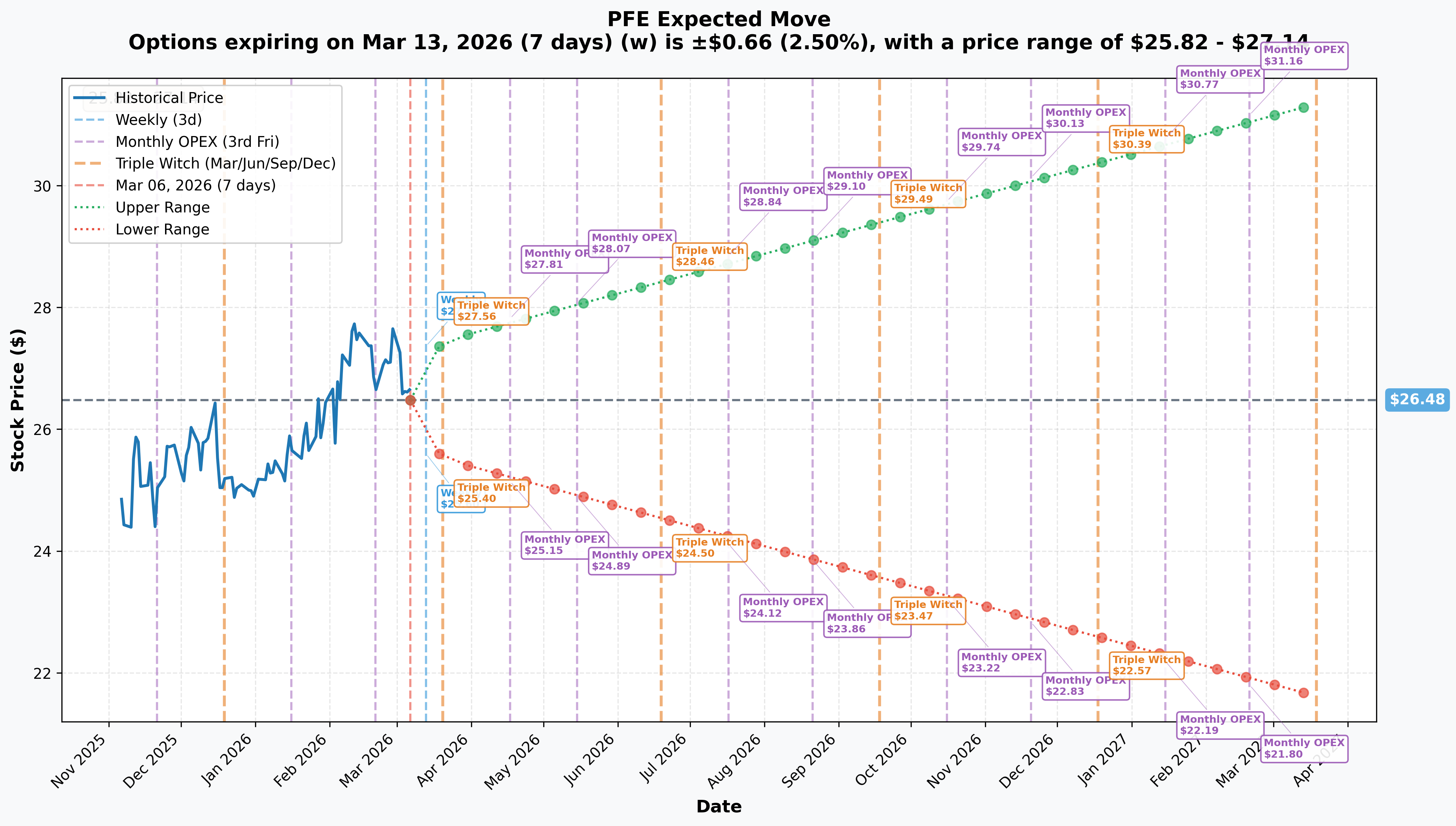

📐 Implied Move Analysis

The options market is pricing in the following expected ranges based on implied volatility:

| Timeframe | Expiration | Expected Range | Move % |

|---|---|---|---|

| 📅 Weekly | 2026-03-13 | $25.82 - $27.14 | +/- 2.5% |

| 📅 Triple Witch | 2026-03-20 | $25.51 - $27.45 | +/- 3.7% |

| 📅 Monthly OPEX | 2026-04-17 | $25.15 - $27.81 | +/- 5.0% |

| 📅 May OPEX | 2026-05-15 | $24.89 - $28.07 | +/- 6.0% |

| 📅 Sep Triple Witch | 2026-09-18 | $23.47 - $29.49 | +/- 11.4% |

| 📅 Yearly LEAPs | 2027-03-19 | $21.61 - $31.35 | +/- 18.4% |

For the September 18 expiration (the one on today's trade):

📈 Implied upside: $29.49 -- The options market sees PFE's upper range at roughly $29.50 by September. The $28 call strike that was sold sits inside this range, meaning it's achievable but not the expected midpoint.

📉 Implied downside: $23.47 -- If things go south, a drop to the low $23s is within the expected distribution. COVID revenue declines and pipeline setbacks could drive this scenario.

Key insight: The seller at $28 is positioning in the upper half of the implied range but below the max expected move. They're betting PFE ends somewhere in the $25-$28 zone -- which is exactly where the stock has been trading. The implied move data shows $28 is reachable but not the base case, making this a high-probability premium collection trade.

🎪 Catalysts

✅ Already Happened (Recent)

📊 FY2025 Earnings (February 3, 2026) -- Pfizer reported solid results and reaffirmed 2026 revenue guidance of $59.5-$62.5B. The Street was reassured by the company maintaining its outlook despite continued COVID product revenue headwinds.

📈 Argus Upgrade to Buy -- Argus Research upgraded PFE to a Buy rating, highlighting the strength of Pfizer's GLP-1 and oncology pipeline as key growth drivers.

💊 PF-3944 Positive Phase 2b Obesity Data -- Pfizer's monthly GLP-1 injectable showed up to 12.3% placebo-adjusted weight loss in Phase 2b trials. This is competitive data in the red-hot obesity space currently dominated by Novo Nordisk and Eli Lilly.

🏥 PADCEV + Keytruda Phase 3 EV-304 Results -- Positive data in muscle-invasive bladder cancer in partnership with Astellas, expanding Pfizer's oncology franchise.

✅ BRAFTOVI Full FDA Approval -- Secured full approval, strengthening Pfizer's oncology market position.

💰 Metsera Acquisition ($10B) -- Pfizer acquired Metsera for up to $10B to bolster its GLP-1/obesity pipeline, signaling management's all-in commitment to the obesity market.

📅 Upcoming

| Date | Event | Why It Matters |

|---|---|---|

| Early-Mid 2026 | Phase 2 danuglipron data (once-daily oral GLP-1) | Could be a game-changer -- an oral GLP-1 is the holy grail vs. injectables. Strong data could break PFE out of its range |

| Mid 2026 | PF-3944 Phase 3 initiation timing | Monthly GLP-1 injectable -- Phase 3 start confirms pipeline progression |

| May 5, 2026 | Q1 2026 Earnings (consensus EPS: $0.73) | First quarter to reflect 2026 guidance trajectory. Key watch: COVID decline pace, oncology growth, GLP-1 investment spending |

| Throughout 2026 | 20+ pivotal Phase 3 trial initiations | Pfizer calls 2026 "rich in catalysts" -- any positive data readout could move the stock |

| 2026-2028 | Patent cliff exposure (key drugs facing LOE) | Revenue risk as blockbuster drugs lose exclusivity |

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, analyst consensus, and the catalyst calendar:

🐻 Bear Case: $24-$25 (-6% to -9%)

📉 If COVID product revenue declines faster than expected (~$1.5B annual headwind), Phase 2 danuglipron oral GLP-1 data disappoints, or the Metsera integration stumbles, PFE could break below the $26 gamma support and test the $25 structural floor. The IRA drug pricing provisions add a further headwind. The implied move downside of $23.47 by September represents the extreme scenario.

Probability: ~20% -- Would require multiple negative catalysts stacking up. The $59.5-$62.5B revenue guidance and diversified portfolio provide a buffer, and the $25-$26 gamma support zone is thick.

⚖️ Base Case: $26-$28 (flat to +6%)

📊 PFE continues to trade in its established $25-$28 range. Earnings meet expectations, the GLP-1 pipeline progresses on schedule but without breakthrough data, and the stock grinds toward the analyst consensus target of ~$27-$28. The covered call seller collects their $5.4M premium, the $28 strike is never seriously challenged, and the trade expires near or out of the money. The $27 gamma wall continues to act as a ceiling with occasional pokes above.

Probability: ~55% -- The most likely outcome. Analyst consensus is Hold with a tight $27-$28 average target. The stock has been rangebound and nothing in the near-term catalyst calendar is likely to dramatically change that.

🚀 Bull Case: $29-$31 (+10% to +17%)

📈 Danuglipron oral GLP-1 Phase 2 data comes in strong (competitive with Novo/Lilly), analysts upgrade en masse, and the market re-rates PFE as a legitimate GLP-1 player. The stock breaks through the $27 and $28 gamma resistance levels, pushes toward $29-$30, and potentially challenges the implied move upper bound at $29.49. The highest analyst target of $35.46 comes into play if multiple pipeline catalysts hit.

Probability: ~25% -- Requires a positive data surprise, likely from the oral GLP-1 program. If Pfizer can credibly challenge Novo Nordisk and Eli Lilly in the obesity space, the stock has meaningful upside from these levels. The $28 call seller would be tested -- but even at $29, they'd only lose $1/share minus the $1.40 premium collected, so they'd still net a small profit on the covered call.

💡 Trading Ideas

🛡️ Conservative: "The Pfizer Paycheck" -- Covered Call (Mirror the Whale)

Structure: Buy 100 shares of PFE at ~$26.49, sell 1 PFE $28 call expiring 2026-09-18

Why this works: You're doing exactly what the institutional player is doing -- owning the stock and selling calls against it. You collect the $1.40 premium ($140 per contract) plus PFE's quarterly dividend (~$0.42/share, roughly $0.84 through September). If PFE stays below $28, you keep the premium and the shares. If it gets called away at $28, you pocket a $1.51 capital gain + $1.40 premium + ~$0.84 in dividends = $3.75 total return on a $26.49 investment (~14.2% in 6 months).

📊 Premium collected: ~$1.40 per share ($140 per contract) 📊 Dividend income: ~$0.84 per share through September 📊 Max profit (if called at $28): ~$3.75/share (14.2% in 6 months) 📊 Downside breakeven: ~$25.09 (stock price minus premium) 📊 Win probability: ~70-75% (stock stays flat or rises modestly) 📊 Best for: Income-focused traders who are moderately bullish and want to get paid while they wait

⚖️ Balanced: "The Range Rider" -- Iron Condor

Structure: Sell PFE $25 put / Buy PFE $24 put / Sell PFE $28 call / Buy PFE $29 call, 2026-09-18 expiration

Why this works: The gamma profile and implied move data both point to PFE staying in a $25-$28 range through September. An iron condor profits from exactly that outcome -- you collect premium from both sides as long as PFE stays between your short strikes. The $25 put side is protected by strong gamma support, and the $28 call side is reinforced by today's massive institutional sell.

📊 Estimated credit: ~$0.50-$0.70 per spread 📊 Max risk: ~$0.30-$0.50 per spread (width minus credit) 📊 Max profit: Credit received (if PFE stays between $25-$28 at expiration) 📊 Win probability: ~60-65% 📊 Best for: Traders who see PFE as rangebound and want to profit from time decay on both sides

🚀 Aggressive: "GLP-1 Breakout Bet" -- Long Call Spread

Structure: Buy PFE $28 call / Sell PFE $31 call, 2026-09-18 expiration

Why this works: If you believe the oral GLP-1 danuglipron data will be the catalyst to break PFE out of its range, this is the cheapest way to bet on it. You're buying the exact strike the whale is selling -- taking the other side of their trade. If Pfizer delivers competitive obesity data and analysts upgrade, the stock could push through $28 and toward $30+. The $31 short call caps your risk and brings the cost down.

📊 Estimated cost: ~$0.60-$0.80 per spread 📊 Max profit: ~$3 per spread at $31+ (~4:1 risk/reward) 📊 Breakeven: ~$28.70 📊 Risk: 100% of premium if PFE stays below $28 📊 Best for: Traders with high conviction on Pfizer's GLP-1 pipeline who want defined-risk upside exposure. Only risk what you can afford to lose.

Pro tip: Wait for the danuglipron Phase 2 data readout (expected early-to-mid 2026) before entering. If the data is strong, IV will spike and the stock could gap -- but the move will be based on real evidence, not hope.

⚠️ Risk Factors

❗ COVID Revenue Headwind -- Pfizer explicitly guides for ~$1.5B in annual COVID product revenue decline. Paxlovid and Comirnaty revenue continues to shrink, and each quarterly report brings scrutiny on whether non-COVID growth can offset the gap.

❗ Patent Cliff Exposure -- Several blockbuster drugs face loss of exclusivity (LOE) in the coming years. Generic competition on key products could create revenue cliffs that the pipeline needs to fill -- and pipeline drugs are never guaranteed.

❗ GLP-1 Competition is Brutal -- Pfizer is entering the obesity space against Novo Nordisk (Ozempic/Wegovy) and Eli Lilly (Mounjaro/Zepbound), who have multi-year head starts, massive manufacturing scale, and deeply established physician relationships. Even strong data may not be enough to gain meaningful market share quickly.

❗ Pipeline Execution Risk -- With 20+ pivotal Phase 3 trials expected to initiate in 2026, the probability that everything goes right is low. Clinical trial failures are common in pharma, and a high-profile setback (especially in GLP-1 or oncology) could tank sentiment.

❗ Metsera Integration Risk -- The $10B Metsera acquisition adds GLP-1 pipeline assets but also adds integration complexity and dilution risk. If the acquired assets underperform, this becomes an expensive mistake.

❗ IRA Drug Pricing Provisions -- The Inflation Reduction Act's Medicare drug price negotiation provisions are a structural headwind for big pharma profitability. Pfizer's large Medicare-exposed portfolio makes it particularly vulnerable.

❗ Rangebound Stock = Low Upside -- With analyst consensus at Hold and an average target of $27-$28, the Street sees limited upside from current levels. If you're buying calls, you're fighting the consensus. The $5.4M institutional call sell today reinforces this ceiling view.

🎯 The Bottom Line

Here's the deal: A sophisticated player just collected $5.4M in premium by selling 38,301 PFE $28 calls through September. This is textbook institutional income generation -- they're saying "Pfizer is a fine company, but it's not going above $28 anytime soon. Pay me to hold that view."

And honestly? The data backs them up. The analyst consensus is Hold at ~$27-$28. The gamma profile shows a massive wall at $27 and another at $28. The implied move says PFE's upper range is $29.49 by September -- achievable but not the base case. And while the GLP-1 pipeline is exciting, Phase 2 data is still pending and the stock hasn't broken out of its $25-$28 range in months.

If you agree with the whale (rangebound view): The covered call strategy is the move. Buy the stock, sell the $28 calls, collect the ~6% dividend, and pocket an all-in return of ~14% annualized if the stock stays in its lane. The $26 gamma support gives you a nice floor. Mark May 5 (Q1 earnings) on your calendar as the first checkpoint.

If you are on the sidelines: Watch for the danuglipron Phase 2 data readout. That is the single catalyst most likely to break PFE out of its range in either direction. Strong oral GLP-1 data = buy the breakout. Weak data = the rangebound thesis gets even stronger and premium selling becomes the dominant play.

If you are bullish on Pfizer's GLP-1 story: The cheap call spread ($28/$31) gives you defined-risk exposure to a breakout. But be honest with yourself -- you're betting against a $5.4M institutional trade and the Street consensus. Have a thesis, not just hope. Wait for data.

The key dates: Q1 earnings May 5, danuglipron data early-to-mid 2026, and this trade's expiration on September 18. Between now and then, Pfizer's story is about execution, not excitement. Size accordingly. 👀

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Options trading involves significant risk of loss. Always do your own research and consider your risk tolerance before entering any trade. Past unusual options activity is not a reliable predictor of future stock price movement.

About Pfizer Inc.: Pfizer is one of the world's largest pharmaceutical firms with annual sales of roughly $60B. Prescription drugs and vaccines account for the majority of sales, with top products including Prevnar 13, Vyndaqel, and Eliquis. Market cap: $151.3B in the Pharmaceutical Preparations industry.