🚨 QQQ Massive $38M Options Activity - Institutions Positioning for December Volatility! 🎯

📅 December 1, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Smart money is making HUGE moves in QQQ! $76M in premiums traded across just three major positions this morning - with institutions selling $21M in covered calls at the $620 strike and closing $29M worth of put positions on their put ladders. This isn't random - these trades signal sophisticated players locking in profits after QQQ's explosive 22.8% YTD rally while positioning for December's catalyst-heavy environment: Nasdaq-100 reconstitution (Dec 12), FOMC meeting (Dec 9-10) with 83% rate cut probability, and Magnificent 7 earnings season starting late January. Translation: Institutions are taking chips off the table near all-time highs while managing risk into year-end!

📊 ETF Overview

Invesco QQQ Trust (QQQ) is the dominant tech growth ETF tracking the Nasdaq-100 Index:

- Assets Under Management: $335.5 billion (largest pure-tech ETF)1

- Current Price: $613.75 (as of Dec 1, 2025)

- YTD Performance: +22.8% through November 20252

- 52-Week High: $637.01 (only 3.7% above current price)3

- Expense Ratio: 0.20% (highly competitive)

- Total Holdings: 102 companies from Nasdaq-1001

What Makes QQQ Different:

QQQ provides concentrated exposure to U.S. innovation leaders with 64% technology allocation4 - far more aggressive than S&P 500 (~30% tech). The ETF is dominated by the Magnificent 7 (NVDA, AAPL, MSFT, AMZN, TSLA, META, GOOGL/GOOG) which represent over 40% of assets5. This concentration drives outperformance in bull markets but amplifies downside risk - [QQQ has outperformed the S&P 500 in seven out of the last 10 years as of September 30, 2025]6.

Top 10 Holdings (December 2025):

| Ticker | Company | Weight | Sector |

|---|---|---|---|

| NVDA | NVIDIA | 9.33% | AI/Semiconductors |

| AAPL | Apple | 8.78% | Consumer Tech |

| MSFT | Microsoft | 7.69% | Cloud/Software |

| AVGO | Broadcom | 6.59% | Semiconductors |

| AMZN | Amazon | 5.21% | E-commerce/Cloud |

| TSLA | Tesla | 3.53% | Automotive/EV |

| META | Meta Platforms | 3.47% | Social Media |

| GOOGL | Alphabet Class A | 3.08% | Internet/Cloud |

| GOOG | Alphabet Class C | 2.88% | Internet/Cloud |

| NFLX | Netflix | 2.73% | Streaming |

Top 10 Total: 53.88% of fund assets1

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (December 1, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Spot | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:02:20 | QQQ | ASK | SELL | CALL $620 | 2026-01-16 | $21M | $620 | 13K | 12K | $613.75 | 11.71 | EXTREMELY UNUSUAL 🔥 |

| 10:07:27 | QQQ | ASK | SELL | PUT $590 | 2026-03-20 | $17M | $590 | 10K | 164K | $613.75 | 0.56 | TYPICAL |

| 10:28:01 | QQQ | ASK | SELL | PUT $580 | 2026-06-18 | $12M | $580 | 5K | 12K | $613.75 | 5.94 | EXTREMELY UNUSUAL 🔥 |

Combined Activity: $50M in premiums traded (13,000 calls sold + 15,000 puts closed)

🤓 What This Actually Means

This is sophisticated portfolio management at year-end by institutions holding massive QQQ positions:

Trade #1: Selling 13,000 Covered Calls @ $620 Strike (Jan 16 expiration) - $21M

- 📊 Covered call overlay: Selling calls against existing QQQ long position to generate $21M income

- 💰 Income generation: Collecting ~$1.60/share premium (~0.26% yield in 45 days)

- 🎯 Strike selection: $620 is just 1.0% above current price ($613.75) - willing to cap upside for income

- 📈 Bullish but cautious: They WANT to keep the position (covered calls) but okay exiting at $620 (+1% from here)

- ⏰ Strategic timing: 45 days to expiration captures December FOMC (Dec 9-10), Nasdaq reconstitution (Dec 12), and holiday season momentum

- 🚨 Unusual size: Z-score of 11.71 means this is 12x larger than typical QQQ call trades - happens maybe a few times per year

What's really happening: This trader likely holds 1.3 million shares of QQQ (worth $798M at $613.75) and is selling calls against it to pocket $21M in premium. If QQQ stays below $620 by January 16th, they keep both the stock AND the premium - that's a 2.6% additional return on a $798M position in just 45 days. If QQQ rallies above $620, they're forced to sell at $620 (still profitable, just capping upside at +1%).

Trade #2: Closing 10,000 March $590 Puts - $17M

- 🛡️ Closing protection: Selling to close (STC) existing puts that were bought as insurance

- 📉 Strike context: $590 is 3.9% below current price - deep out-of-the-money protection no longer needed

- ⏰ March 20 expiration: 109 days out - they're unwinding protection 3.5 months early

- 💰 Realized gain: Likely bought these puts when QQQ was lower, now selling for profit as QQQ rallied

- 📊 Typical size: Z-score of 0.56 means normal institutional position management

- ✅ High conviction: If they're closing downside protection, they're confident in December catalysts

Trade #3: Closing 5,000 June $580 Puts - $12M

- 🛡️ Unwinding deep protection: $580 is 5.5% below current price - even deeper insurance being removed

- 📅 June 18 expiration: 199 days out - closing protection 6.5 months early!

- 🎯 Strong bullish signal: Selling protective puts this far out shows extreme confidence

- 🔥 Very unusual: Z-score of 5.94 means 6x larger than typical - significant position unwind

- 💸 Capital redeployment: Freeing up $12M that was tied up in insurance to redeploy elsewhere

Combined Trading Strategy Analysis:

This is a "reduce insurance, cap upside, generate income" positioning:

- ✅ They're reducing downside protection by closing $590 and $580 puts (bullish signal - don't need insurance)

- ✅ They're generating income by selling $620 calls against existing long (willing to cap upside)

- ✅ They're staying long QQQ core position but managing around it tactically

- ⚠️ The net effect: Bullish positioning with limited upside (happy with 1% gain to $620 vs full upside capture)

Translation for regular folks:

Imagine you own a house worth $613k that you bought for $500k (22.8% gain like QQQ YTD). You're confident it won't drop below $590k in the next few months, so you're canceling your expensive insurance policy to free up cash. At the same time, you're willing to sell the house for $620k if someone offers - locking in gains while collecting rental income in the meantime. You're not bearish (canceling insurance), but you're also not greedy (capping upside at $620k instead of holding for $650k).

Why this matters:

When institutions managing hundreds of millions take these actions simultaneously:

- 🎯 They see December catalysts (FOMC, reconstitution) as NEUTRAL-TO-POSITIVE (not negative, or they'd keep protection)

- 📈 They expect QQQ to trade in narrow range $605-$625 through January (hence selling $620 calls and $590 puts)

- 💰 They prefer collecting premium income vs speculating on big moves

- ⚠️ They're NOT expecting explosive upside to $640+ (would never sell $620 calls if they expected that)

📈 Technical Setup / Chart Check-Up

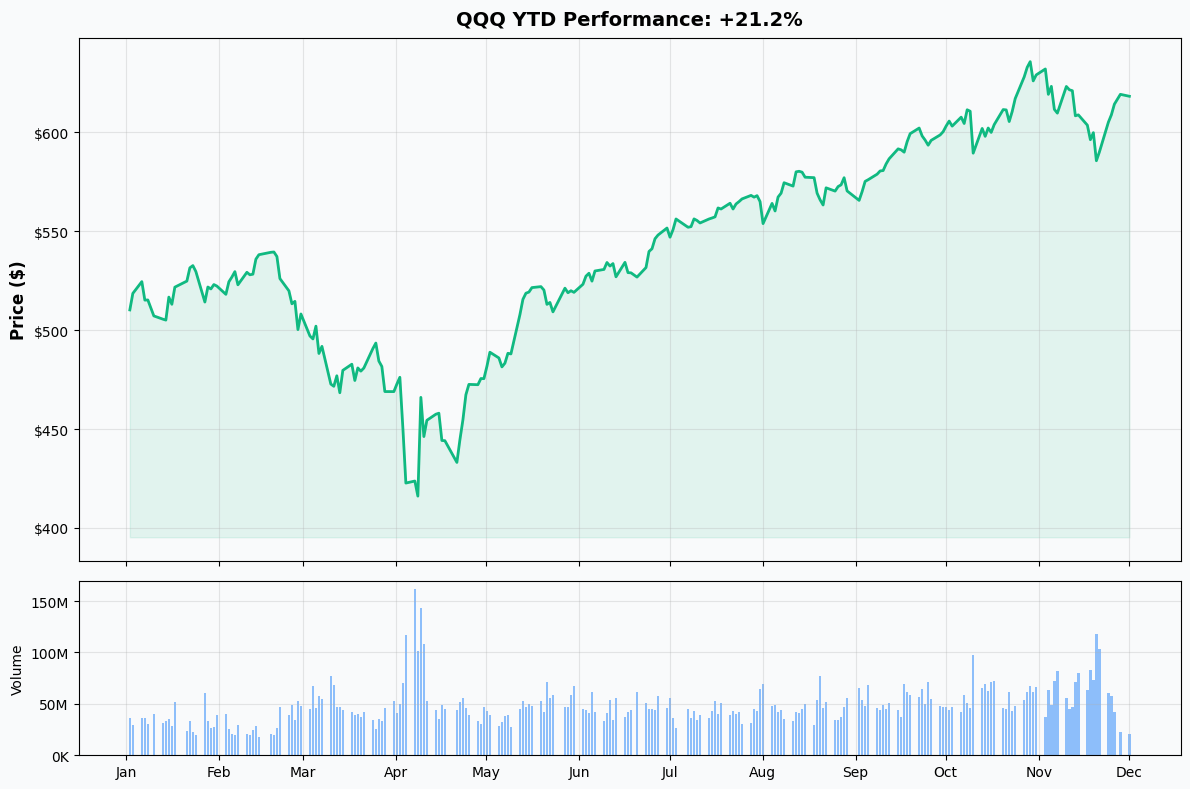

YTD Performance Chart

QQQ is absolutely crushing it in 2025 - up +22.8% YTD with current price at $613.75 (started year around $500). The chart shows a powerful AI-driven growth story - after recovering from March volatility, QQQ rallied from $560 in spring to near all-time highs of $637.01 in November.

Key observations:

- 🚀 Strong uptrend: Consistent higher highs and higher lows since April 2025

- 📈 Tech sector leadership: Magnificent 7 concentration driving outperformance vs S&P 500

- 📊 Recent consolidation: Trading in tight $605-625 range in November after hitting $637 peak

- 🎢 Relatively low volatility: Despite 22.8% gains, pullbacks have been shallow (max drawdown <10%)

- ⚠️ Near all-time highs: Only 3.7% below $637.01 peak - limited upside cushion

The covered call sale at $620 makes perfect sense in this context - sellers are willing to cap gains at historical resistance near the 52-week high, collecting premium while waiting for next catalyst.

Gamma-Based Support & Resistance Analysis

Important Note: Gamma exposure data is currently unavailable for QQQ, which is unusual given the high options activity. This could indicate:

- 🔄 Market makers actively repositioning gamma exposure

- 📊 Options market structure shifts ahead of Nasdaq reconstitution

- ⚠️ Reduced dealer hedging activity at year-end (tax considerations)

However, we can derive key technical levels from the options activity and price action:

Implied Support Levels:

- $610 - Immediate support (recent consolidation floor)

- $605 - Secondary support (November trading range bottom)

- $590 - Major structural support (where institutions closed puts - shows confidence this won't break)

- $580 - Deep support (second put strike closed - disaster floor)

Implied Resistance Levels:

- $620 - CRITICAL RESISTANCE (where $21M in calls were sold - institutions expect selling pressure here)

- $625-630 - Intermediate resistance zone

- $637 - All-time high / psychological barrier

- $640 - Upper range from implied move calculations

What the options flow tells us about gamma:

The sale of 13,000 calls at $620 creates negative gamma for the call sellers (institutions). This means:

- 📈 As QQQ approaches $620, call sellers will need to sell more QQQ to hedge (creates resistance)

- 🚧 $620 becomes a "gamma wall" that's difficult to break through

- 🎯 If $620 breaks, could see rapid acceleration to $630-635 as dealers flip from selling to buying

The closing of puts at $590 and $580 removes positive gamma that was supporting those levels:

- ⚠️ These levels may offer LESS support than before since protection was removed

- 📉 Institutions clearly don't expect downside below $590 (would never close insurance otherwise)

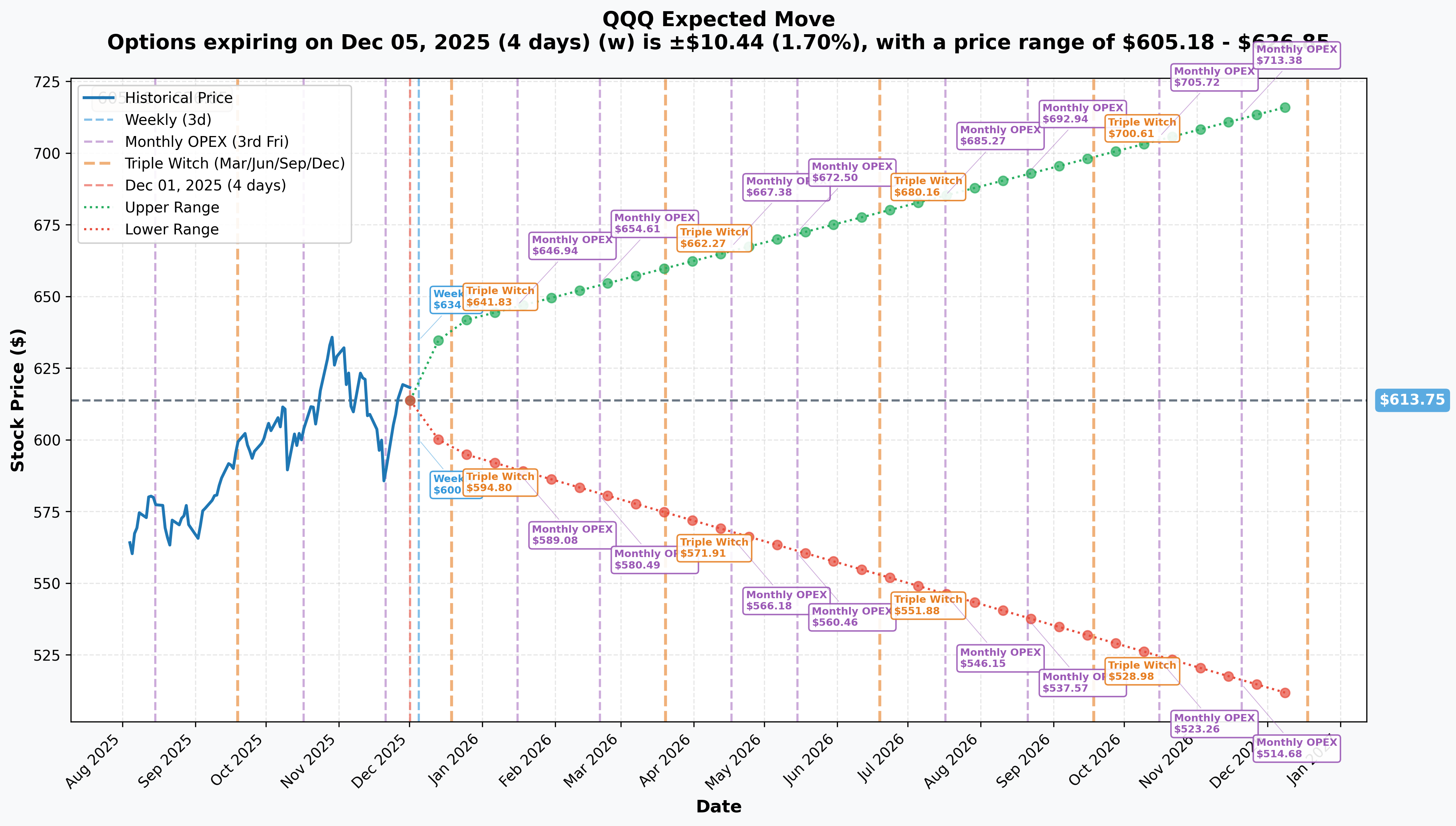

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 4 days): ±$10.44 (±1.7%) → Range: $605.18 - $626.85

- 📅 Monthly OPEX (Dec 19 - 18 days): ±$20.61 (±3.36%) → Range: $596.23 - $640.55

- 📅 Quarterly Triple Witch (Dec 19 - 18 days): ±$20.61 (±3.36%) → Range: $596.23 - $640.55

- 📅 Yearly LEAPS (Dec 18, 2026 - 382 days): ±$98.52 (±16.05%) → Range: $509.43 - $718.07

Translation for regular folks:

Options traders are pricing in:

- 🎯 1.7% move ($10) by Friday - very modest, suggesting calm week ahead

- 📊 3.36% move ($21) through December OPEX - includes FOMC meeting (Dec 9-10) and Nasdaq reconstitution (Dec 12)

- 🚀 Upper range of $640.55 aligns almost PERFECTLY with where institutions sold the $620 calls (they're playing the range!)

- 📉 Lower range of $596.23 sits comfortably ABOVE the $590 puts they closed (confirms they're confident in support)

Notice the symmetry?

The institutions who made these trades are positioning for QQQ to trade within the December implied move range of $596-640. They:

- ✅ Closed $590 puts (lower bound protection no longer needed)

- ✅ Sold $620 calls (happy to cap upside in upper third of range)

- ✅ Net positioning: Bullish $596-620 range trade through January

Key insight for December:

The 3.36% implied move through Dec 19 is SIGNIFICANT for a mega-cap ETF like QQQ. This reflects uncertainty around:

- 🎯 FOMC rate decision (Dec 9-10) - 83% probability of 0.25% cut but not guaranteed7

- 🔄 Nasdaq-100 reconstitution (Dec 12) - forced buying/selling creates volatility8

- 📊 Year-end rebalancing and tax-loss harvesting flows

- 🎪 Positioning ahead of Magnificent 7 earnings (late January)

The December 19 OPEX is also Quarterly Triple Witching - when stock options, stock index futures, and stock index options all expire simultaneously, creating amplified volatility.9

Historical context:

December typically shows lower volatility due to holiday trading, but the 3.36% implied move is ELEVATED compared to normal ~2% monthly ranges. The options market is pricing meaningful event risk in the next 18 days.

🎪 Catalysts

🔥 Immediate Catalysts (Next 14 Days)

FOMC Meeting - December 9-10, 2025 (8-9 DAYS AWAY!) 💰

The Federal Reserve's final meeting of 2025 carries massive implications for tech growth stocks:

Expected Outcome:

- 📊 83.2% probability of 0.25% rate cut according to CME FedWatch Tool (as of November 30, 2025)7

- 🎯 Target range if cut: 3.50%-3.75% (down from current 3.75%-4.00%)10

- 📈 Market pricing: Odds jumped from 50/50 in early November to 86% probability by late November11

Why this matters for QQQ:

Rate cuts are jet fuel for tech growth stocks because:

- 💸 Lower discount rates on future earnings make high-growth companies more valuable

- 📊 Improved borrowing costs for tech companies investing in AI/infrastructure

- 🚀 "Risk-on" sentiment drives capital into growth vs defensive sectors

- 💰 Bond yield compression makes equity yields more attractive (tech typically pays low dividends)

[According to T. Rowe Price, "Rising yields usually pressure growth stocks (especially tech), as future earnings are discounted at higher rates."]12 The reverse is also true - falling rates from Fed cuts support tech valuations.

Key uncertainties:

- ⚠️ Fed Chair Jerome Powell stated December cut is "not a foregone conclusion—far from it"13

- 🤔 FOMC minutes revealed "many" members expressed skepticism about need for additional reduction in 202514

- 🌫️ Government shutdown complicated decision-making; Powell compared situation to "driving in the fog" due to missing October economic data15

- 📊 Wharton's Jeremy Siegel called this "the most uncertain FOMC meeting in years"16

Potential outcomes for QQQ:

- ✅ Rate cut confirmed (83% probability): QQQ likely rallies 1-2% to test $620-625 resistance

- 🎯 Dovish language + cut: Could push QQQ toward $630-637 (all-time high test)

- 😰 No cut (17% probability): Would likely trigger 2-3% selloff to $595-600 support

- ⚠️ Cut but hawkish guidance: Mixed reaction, possible initial pop then fade (net neutral)

Historical precedent: The October 29, 2025 FOMC cut of 0.25% to 3.75%-4.00% range lifted tech stocks by reducing discount rates on future earnings.10 A similar reaction is expected if December cut proceeds.

Nasdaq-100 Reconstitution Announcement - December 12, 2025 (11 DAYS AWAY!) 🔄

What is reconstitution?

The Nasdaq-100 Index undergoes annual reconstitution where companies are added/removed based on market cap rankings and eligibility criteria. Since QQQ tracks this index, any changes trigger mandatory buying/selling by the ETF.

Key Dates:

- 📅 Announcement: December 12, 2025 (Thursday)8

- 📅 Implementation: December 19, 2025 (Friday - also Triple Witching!)8

Why this matters:

- 💰 Forced flows: QQQ and other index-tracking products (~$400B+ combined) must rebalance to match new composition

- 📊 Passive buying: Newly added stocks see surge in demand (historically 2-5% gains week post-announcement)9

- 📉 Passive selling: Deleted stocks see institutional liquidation (can drop 5-10%)

- 🎢 Amplified volatility: Coincides with December Triple Witching expiration, multiplying derivative market activity9

Recent Precedent (December 2024):

Last year's reconstitution added [Palantir (PLTR), MicroStrategy (MSTR), and Axon Enterprise (AXON)]17 while removing [Illumina (ILMN), Super Micro Computer (SMCI), and Moderna (MRNA)]17. Palantir surged following the announcement while deleted stocks declined sharply.

Expected changes for 2025 (speculation):

Based on market cap rankings and performance, potential candidates for addition include high-growth tech companies that crossed into top-100 market cap territory in 2025. Potential deletions could include companies that faced significant market cap declines.

Impact on QQQ:

- 📊 Net asset impact likely minimal (typically <0.5% of total assets change hands)

- 🎢 Increased trading volume December 12-19 creates short-term volatility

- ✅ Usually net positive for QQQ as deletions tend to be weak performers being replaced by strong growth names

- 🎯 Provides tactical trading opportunities for active managers around implementation

10-Year Treasury Yield Trajectory

Current Status: Weekly average at 4.05% at end of October 202518

Q4 2025 Forecasts: Continued downward trend toward 3.72% by December driven by Fed rate cuts19

Tech correlation context:

Historical correlation of -0.33 between tech stocks and 10-year yields suggests relatively weak inverse relationship20, meaning tech can rise even as yields stay elevated (not as coupled as commonly believed). However, at yields of 5%+ bonds compete strongly with equities, but current 4% level remains manageable for growth stocks.21

QQQ sensitivity:

- 📈 Yields below 3.75%: Strong tailwind for QQQ (growth stocks more attractive)

- ⚖️ Yields 4.00-4.50%: Neutral zone, minimal impact on positioning

- 📉 Yields above 4.50%: Significant headwind (5-8% potential decline in QQQ)12

The trend toward 3.72% by year-end is bullish for QQQ as it reduces competition from fixed income and lowers discount rates on tech earnings.

🚀 Near-Term Catalysts (Q1 2026)

Magnificent 7 Earnings Season - Late January 2026

The most critical catalyst for QQQ's 2026 performance is the earnings reports from its largest holdings, which represent over 40% of the portfolio.5

January 29, 2026 (Wednesday - After Market Close):22

Key metrics to watch:

- 🌥️ Azure Growth: Must maintain 35%+ YoY growth to justify valuation; Q4 FY2025 delivered 39% growth23

- 🤖 AI Monetization: Azure AI revenue trajectory and customer adoption (80% of Fortune 500 using Azure AI)24

- 💰 Capex Guidance: Expected to exceed $30B in Q1 FY2026 for AI infrastructure25

- 📊 Azure Annual Run Rate: Surpassed $75B in FY2025; watching for acceleration26

Catalyst potential: Microsoft is THE bellwether for enterprise AI spending. Strong Azure growth signals healthy hyperscaler capex, which cascades to NVDA, AVGO, and entire QQQ semiconductor holdings. Weak results would pressure entire tech sector.

Key metrics to watch:

- 💰 Advertising Revenue: Growth amid economic uncertainty

- 🤖 AI Investments ROI: Reality Labs losses vs AI-driven efficiency gains

- 📱 User Engagement: Instagram/Facebook/WhatsApp trends

- 💸 Capex/Operating Expenses: AI infrastructure spending sustainability

Key metrics to watch:

- 🚗 Cybertruck Production: Ramp progress and profitability

- 📊 Model 3/Y Demand: Pricing power and volume trends

- 🤖 FSD Progress: Autonomous driving timeline updates

- 🇨🇳 China Performance: Market share and competitive dynamics vs BYD

January 30, 2026 (Thursday - After Market Close):22

Apple (8.78% of QQQ - LARGEST CONSUMER TECH WEIGHT)

Consensus Estimates (Fiscal Q1):

- 💰 EPS: $1.77 (up 8% YoY)

- 📊 Revenue: $102B (up 7.5%)27

Key metrics to watch:

- 📱 iPhone 16 Sales: Momentum sustainability after strong initial 20% YoY surge28

- 🇨🇳 China Performance: Critical after October's 37% YoY surge - can it continue?29

- 💻 Services Revenue: Highest-margin segment growth trajectory

- ⚠️ Tariff Impact: CEO warned of $1.1B cost increase in Q427

- 🎯 Guidance: March quarter seasonality and full-year outlook

Catalyst magnitude: Apple is 8.78% of QQQ - largest single stock weight after NVDA. [China sales momentum is critical]30 - if sustained, could drive 5-7% upside for AAPL and add ~0.5% to QQQ. Conversely, tariff concerns or weak guidance could trigger 5-8% AAPL decline, costing QQQ ~0.7%.

China context: Apple captured [25% of China smartphone market with strong performance lifting overall market by 8%]31 in October 2025. iPhone 16 sales surged [37% YoY with mid-to-high double-digit growth across all models]29. This momentum is Apple's biggest positive surprise of 2025 and needs to continue into holiday quarter.

Mid-to-Late February 2026:

NVIDIA (9.33% of QQQ - LARGEST HOLDING!)

Q4 FY2026 Guidance: $65.0 billion revenue (±2%)32

Key metrics to watch:

- 🚀 Blackwell GPU Ramp: Production yields, customer deployment rates, supply constraint timeline

- 💰 Data Center Revenue: Sustainability of 60%+ YoY growth (Q3 delivered 66% growth to $51.2B)33

- 🤖 AI Demand: Blackwell represents 70% of data center compute revenues (3.6M GPUs ordered in 2025)34

- 📊 Long-Term Visibility: $307B revenue pipeline from Blackwell and Rubin systems over next 5 quarters35

- ⚖️ Competition: AMD/custom chip threats, market share trajectory

Catalyst magnitude: NVDA is QQQ's largest holding at 9.33% - its performance drives the entire ETF. Q3 results were spectacular ([revenue $57B, up 62% YoY, beating consensus]36), with CEO Jensen Huang declaring "Blackwell sales are off the charts" and cloud GPUs completely sold out.36 NVDA became the world's first $5 trillion company on October 29, 2025.37

Blackwell importance: Now represents 70% of data center compute revenues with [3.6 million GPUs ordered in 2025 vs 1.3 million Hopper GPUs in 2024 peak]34. Production and deployment success is CRITICAL - any delays or yield issues would crater NVDA and take QQQ down 5-10%.

Risk factor: ["Investors have long been aware that Nvidia's elevated exposure to hyperscalers—which could sharply cut spending at any point—is a risk worth monitoring."]38 Any hints of hyperscaler capex reduction in Q4 guidance would trigger massive tech selloff.

Aggregate Magnificent 7 Impact:

The Magnificent 7 comprises over 25% of S&P 500 market cap and 40%+ of QQQ.37 Collective earnings results will determine whether QQQ can sustain momentum above $620 or faces consolidation back to $590-600.

Best-case scenario (25% probability):

- ✅ All beat on revenue and earnings

- ✅ Strong AI monetization progress across MSFT, META

- ✅ NVDA Blackwell demand exceeds already-high expectations

- ✅ AAPL China momentum sustained

- Result: QQQ rallies to $640-650 (+4-6% from current)

Base-case scenario (50% probability):

- ⚖️ Mixed results - 4-5 beat, 1-2 meet/miss

- ⚖️ Guidance cautious due to macro uncertainty

- ⚖️ AI spending sustained but not accelerating

- Result: QQQ consolidates $605-625 range

Worst-case scenario (25% probability):

- 😰 Multiple misses or weak guidance

- 😰 Hyperscaler capex reduction signals

- 😰 China weakness impacts AAPL, NVDA export concerns

- Result: QQQ drops to $580-590 (-5-8% from current)

⚠️ Risk Catalysts (Negative)

AI Investment Overextension Risk 🤖

Magnitude: MEDIUM

["There's the risk of overinvestment in AI technologies. If this dynamic shifts, the demand for AI chips could weaken, creating a ripple effect across the supply chain."]39

The setup: Microsoft, Amazon, Google, Meta collectively spending $150B+ annually on AI infrastructure. This capex tsunami drives NVDA (9.33% of QQQ), AVGO (6.59%), and cloud provider revenues (MSFT, AMZN, GOOGL = 16% of QQQ).

The risk: If Q4 2025/Q1 2026 earnings reveal disappointing AI monetization relative to massive capex, hyperscalers could sharply cut AI spending. This would cascade through QQQ holdings:

- NVDA: -15-25% potential decline

- AVGO: -10-15% potential decline

- Cloud providers (MSFT, AMZN, GOOGL): -5-10% decline

- Aggregate QQQ impact: 5-10% decline scenario

Timing: Most likely risk window is Q1-Q2 2026 earnings if AI revenue growth doesn't justify capex.

Regulatory and Antitrust Scrutiny 🏛️

Magnitude: HIGH

["As November 2025 unfolds, the landscape for technology giants is increasingly fraught with challenges. A wave of intensified regulatory scrutiny globally, coupled with ongoing antitrust battles in the United States, continues to cast a long shadow over the sector."]40

Specific threats to QQQ holdings:

- Google (5.96% combined GOOGL+GOOG): Ongoing DOJ antitrust litigation over search monopoly; potential breakup scenarios

- Apple (8.78%): App Store antitrust cases in U.S. and EU; Digital Markets Act compliance costs

- Meta (3.47%): Privacy regulations, content moderation requirements, potential platform restrictions

- Amazon (5.21%): FTC antitrust lawsuit over marketplace practices

AI-specific focus: ["There is now a clear focus on AI foundation models where agencies are keen to guard against deals that would lead to high levels of concentration or foreclose access to the key inputs (data, accelerator chips, computing infrastructure, cloud capacity and technical expertise)."]41

Administration uncertainty: Trump Administration changes to FTC and DOJ leadership create uncertainty about enforcement approach.[^19_6]

Impact estimate: Major antitrust action against top-3 holdings (NVDA, AAPL, MSFT) could reduce QQQ by 5-15% depending on severity.

Concentration Risk - The "One Stock Problem" 🎯

Magnitude: CRITICAL

Top 10 holdings represent 53.88% of QQQ assets1, with more than 50% allocated to technology sector.42

The math is brutal:

- 10% decline in NVDA (9.33% weight) = -0.93% for QQQ

- 10% decline in top 3 (NVDA, AAPL, MSFT = 25.8%) = -2.58% for QQQ

- Simultaneous 10% decline in top 10 = -5.4% for QQQ

["If just one or two—say, Nvidia or a leading cloud provider—suffer a major rerating, QQQ can't hide in smaller holdings the way a broad index might."]43

The U.S. market's reliance on Magnificent Seven introduces systemic risks and raises questions about market sustainability.44

What this means: The $21M covered call sale at $620 and put closing at $590 suggests institutions are AWARE of this concentration risk and managing it by capping upside (via covered calls) rather than maintaining unlimited exposure.

China Geopolitical Risk 🇨🇳

Magnitude: MEDIUM-HIGH

Multiple QQQ holdings have significant China exposure:

- Apple: ~20% of revenue from Greater China; trade tensions or Huawei competition threaten sales45

- NVIDIA: Export restrictions on advanced chips limit addressable market

- Tesla: Major production facility in Shanghai, competitive threats from BYD

- Qualcomm, Broadcom: Semiconductor supply chain dependencies

Recent precedents:

- AAPL China iPhone sales faced headwinds as [Huawei remains a strong rival]45 despite recent October surge

- NVDA faced export restrictions requiring special China-specific chip designs

Taiwan risk: Geopolitical tensions over Taiwan strait would impact semiconductor supply chains (NVDA, AVGO, QCOM, AMD depend on TSMC manufacturing)

Trade policy: Tariff escalation would pressure margins - [AAPL warned tariffs could add $1.1B to costs in Q4]27

Valuation Risk After 22.8% YTD Rally 💰

Magnitude: MEDIUM

Current positioning:

- QQQ up 22.8% YTD through November2

- Trading only 3.7% below all-time high of $637.013

- Estimated aggregate P/E ratio: 32-35x forward earnings (above 10-year average of ~28x)

Multiple compression risk:

If earnings growth disappoints or Fed pivots back to rate hikes, QQQ faces 10-15% downside from multiple compression even with earnings growth. At current valuations, there's minimal margin for error.

Trigger events:

- Fed pivot back to rate hikes if inflation resurges

- Earnings misses from multiple Magnificent 7 members

- Broad market rotation from growth to value (economic slowdown scenario)

🎲 Price Targets & Probabilities

Using the options flow positioning, implied move data, catalysts, and technical analysis:

📈 Bull Case (30% probability)

Target: $640-650

How we get there:

- ✅ FOMC delivers rate cut + dovish guidance (Dec 9-10): 0.25% cut confirmed with signals of 1-2 more cuts in 2026, pushing 10-year yields below 3.75%

- 🔄 Nasdaq reconstitution net positive (Dec 12): Strong growth companies added, weak names removed, reinforcing QQQ's tech leadership

- 📊 10-year Treasury yields trend to 3.72% as forecasted19, making growth stocks more attractive vs fixed income

- 🎯 Risk-on sentiment into year-end as recession fears fade and AI momentum continues

- 🚀 January earnings exceed expectations: At least 5 of 7 Magnificent companies beat with strong AI monetization progress

- 🇨🇳 China stability: No new export restrictions, AAPL momentum sustained

- 📈 Break above $620 resistance triggers technical rally as $21M in sold calls are breached, forcing covering

Key metrics needed:

- FOMC dovish on December 10th (not just cut, but supportive language for 2026)

- MSFT Azure growth sustained 35%+

- NVDA Blackwell demand confirmed at Q4 earnings

- AAPL China strength continues through holiday quarter

- No hyperscaler capex reduction signals

Probability assessment: Only 30% because it requires PERFECT execution across multiple fronts. The $620 covered call sale signals institutions DON'T expect this scenario (they'd never cap upside at $620 if expecting $650). Multiple resistance levels ($620, $625, $637) create technical headwinds.

🎯 Base Case (50% probability)

Target: $605-625 RANGE (CONSOLIDATION)

Most likely scenario:

- ⚖️ FOMC delivers cut as expected (83% probability) but with neutral-to-slightly-hawkish 2026 guidance

- 📊 Nasdaq reconstitution neutral impact - normal turnover, no major surprises

- 💤 Holiday season low-volume consolidation - typical December pattern with range-bound trading

- 📈 Yields stabilize 3.9-4.1% range - neither strongly bullish nor bearish for tech

- ⚖️ January earnings mixed - 4-5 beats, 1-2 meets/misses, cautious guidance due to macro uncertainty

- 🎯 QQQ trades between $620 resistance and $605 support for 6-8 weeks

- 💰 Volatility crush post-December - implied vol drops from 3.36% to 2% range as events pass

- ⏰ Market waits for Q1 2026 earnings to provide next major catalyst

This is EXACTLY what the options flow predicts:

- ✅ Institutions sold $620 calls (expecting resistance there)

- ✅ Institutions closed $590 puts (confident support holds above there)

- ✅ Net positioning: $596-625 range through January expiration

- ✅ Income collection via covered calls suggests low-volatility expectations

Why 50% probability:

Stock at technical equilibrium - neither breaking out nor breaking down. December catalysts (FOMC, reconstitution) likely net neutral to slightly positive. Fundamentals solid but valuation fully reflects current growth expectations. Most institutional players positioned to collect premium in range rather than speculate on direction.

Covered call P&L in Base Case:

- QQQ stays $605-619 through Jan 16: Calls expire worthless, sellers keep $21M premium (2.6% return in 45 days)

- QQQ at $620 on Jan 16: Calls exactly at-the-money, minimal assignment risk

- This is the TARGET scenario for the $21M call seller

📉 Bear Case (20% probability)

Target: $580-595

What could go wrong:

- 😰 FOMC doesn't cut (17% probability) or cuts with VERY hawkish 2026 guidance - triggers immediate 2-3% gap down7

- 📊 10-year yields spike above 4.25% on inflation concerns or Fed hawkishness

- 🇨🇳 China export restrictions announced on advanced AI chips, hitting NVDA/AVGO

- 💸 Multiple Magnificent 7 earnings disappoint - even 2-3 misses would pressure entire QQQ

- 🚨 Hyperscaler capex reduction signaled by MSFT, AMZN, or GOOGL in Q4 reports

- 📉 Nasdaq reconstitution forces selling of popular names that drop out (unlikely but possible)

- 🌐 Major antitrust action announced against GOOGL, AAPL, or MSFT

- 🤖 AI monetization disappoints - revenue growth doesn't justify $150B+ annual capex spend

- 📊 Broader tech selloff on recession fears or sector rotation to value

- 🔨 Break below $605 support triggers cascade to $590, then $580

Critical support levels:

- 🛡️ $605: Immediate support (November range floor) - MUST HOLD

- 🛡️ $596: Lower bound of December implied move - technical support

- 🛡️ $590: Deep support where institutions closed puts (shows they don't expect breakdown here)

- 🛡️ $580: Disaster floor where second round of puts were closed

Probability assessment:

Only 20% because it requires multiple negative catalysts to align simultaneously. QQQ's fundamentals remain strong (AI growth, hyperscaler spending, Magnificent 7 earnings power), and the options flow shows institutions DON'T expect downside below $590 (would never close $29M in put protection otherwise).

However, concentration risk is real:

A single blow-up in NVDA (9.33% weight) or AAPL (8.78% weight) could quickly push QQQ toward $590 even without broader market issues.

Why institutions closed $590/$580 puts:

They're confident THIS scenario is low-probability through March/June timeframes. If they expected material downside, they'd KEEP the $29M in insurance, not close it out.

💡 Trading Ideas

🛡️ Conservative: Copy The Smart Money - Covered Calls

Play: Sell covered calls against existing QQQ position, mirroring the $21M institutional trade

Structure (if you own 100 shares QQQ):

- Current position: 100 shares QQQ at ~$614/share = $61,400 value

- Sell 1 contract QQQ Jan 16 $620 calls

- Collect: ~$160-180 premium per contract ($1.60-1.80/share)

Why this works:

- 💰 Generate income: Collect $160-180 premium (0.26% yield in 45 days = 2.1% annualized)

- 📊 Keep position: You're LONG QQQ but willing to sell at $620 (+1% upside)

- 🎯 Smart positioning: Institutions managing HUNDREDS OF MILLIONS made this EXACT trade

- ⚖️ Risk defined: Max gain is $620 - if called away, you sell at profit and keep premium

- 🛡️ Downside help: Premium reduces effective cost basis to $612.20-$612.40

- ⏰ Strategic timing: 45 days captures FOMC (Dec 9-10), reconstitution (Dec 12), holiday season

Scenario analysis:

- 📈 QQQ closes below $620 on Jan 16: Keep stock + $160 premium = 0.26% bonus return (plus any appreciation)

- 📈 QQQ at $620-622 on Jan 16: Likely called away at $620, total return = $6/share gain + $1.60 premium = $7.60 (1.24% return in 45 days)

- 🚀 QQQ above $622 on Jan 16: Stock called away at $620, you "miss" gains above $620 but still profit

- 📉 QQQ drops to $600: Keep stock, keep $160 premium, effective loss reduced by premium

Who this is for:

- ✅ Current QQQ holders who believe in long-term story but expect consolidation

- ✅ Investors comfortable capping upside at $620 (1% above current) for income

- ✅ Those who want to follow institutional positioning (never a bad idea!)

Position sizing: Use on 25-50% of QQQ holdings, not entire position (keep some upside optionality)

Risk level: Low (already own underlying) | Skill level: Beginner-friendly

Expected outcome: 80% probability of keeping stock + premium (QQQ stays below $620), 2.1% annualized income boost

⚖️ Balanced: FOMC Straddle - Bet On Volatility

Play: Buy straddle ahead of December 9-10 FOMC meeting, betting actual move exceeds 1.7% weekly implied move

Structure:

- Buy QQQ Dec 5 (weekly) $615 calls

- Buy QQQ Dec 5 (weekly) $615 puts

- Expiration: December 5 (captures FOMC Dec 9-10 announcement)

Note: Adjust to December 12 weekly if December 5 doesn't capture the FOMC timing properly - want expiration 2-3 days AFTER Dec 10 announcement.

Why this could work:

- 💥 Implied move "too low": Market pricing only 1.7% ($10) move for the week, but FOMC meetings historically move QQQ 2-4%

- 🎰 Binary event: 83% cut probability still means 17% chance of NO CUT - either outcome creates movement7

- 📊 Wharton's Jeremy Siegel: Called this "the most uncertain FOMC meeting in years"16 - uncertainty = volatility opportunity

- ⚡ Fed Chair Powell: "Not a foregone conclusion—far from it"13 suggests genuine debate

- 🌫️ Missing economic data from government shutdown adds unpredictability15

- 🚀 Need only 2% move either way to profit (vs 1.7% priced in)

Estimated P&L (adjust after checking current pricing):

- 💰 Cost: ~$6-8 per straddle ($600-800 per contract)

- 📈 Profit scenario: QQQ moves to $622+ or $608- (2%+ move) = $5-7 gain per contract (60-80% ROI)

- 🚀 Home run: QQQ moves to $625+ or $605- (3%+ move) = $10+ gain (100%+ ROI)

- 📉 Loss scenario: QQQ stays $611-619 range = lose $2-6 per contract (25-75% loss)

- 💀 Total loss: QQQ exactly at $615 = lose entire premium (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$621-623 (1.3% rally needed)

- 📉 Downside breakeven: ~$607-609 (1.3% drop needed)

Critical timing:

- ⏰ Enter: Monday Dec 8 or Tuesday Dec 9 morning (1-2 days before announcement)

- 🎯 Exit: Wednesday Dec 10 afternoon or Thursday Dec 11 (immediately after FOMC reaction)

- ⚠️ DO NOT hold to expiration - take profits/losses within 24-48 hours of announcement

Why this is "Balanced" not "Aggressive":

- ✅ Defined risk (can only lose premium paid)

- ✅ Two-way bet (profit from either direction)

- ✅ Short-dated (only 4-5 days of theta decay)

- ✅ Based on identifiable catalyst (FOMC) not speculation

- ⚠️ But still requires disciplined exit plan and volatility timing

Risk level: Moderate (can lose 100% of premium) | Skill level: Intermediate

Probability of profit: ~45-50% (slightly better than implied odds if you're right about vol being underpriced)

🚀 Aggressive: Directional Put Spread - Fade The Rally (ADVANCED)

Play: Bear put spread betting QQQ pulls back from highs after initial FOMC rally

Structure:

- Buy QQQ Jan 16 $615 puts

- Sell QQQ Jan 16 $605 puts

- Net debit: ~$4-5 per spread ($400-500 per contract)

- Max profit: ~$5-6 per spread ($500-600 per contract) if QQQ below $605

- Max loss: ~$4-5 per spread (100% of premium paid) if QQQ above $615

Why this could work:

- 📊 Fighting the trend BUT... institutions showed CLEAR positioning by selling $620 calls (expect resistance)

- ⚖️ Post-FOMC fade: Even if Fed cuts, classic pattern is rally then pullback as reality sets in

- 🎯 Targeting $605 support where November range floor sits

- 💰 Defined risk: Only lose max $400-500 per spread, not unlimited downside like short stock

- 📉 Technical setup: QQQ overbought near $620 after 22.8% YTD rally, due for consolidation

- 🌐 Macro concerns: Valuation stretched, concentration risk, AI overinvestment worries3943

- ⏰ Time on your side: 45 days to expiration allows multiple attempts to break $610

Why this could blow up (SERIOUS RISKS):

- 🚀 Fighting momentum: QQQ up 22.8% YTD with institutional bid - dangerous to short2

- 📈 January earnings could drive upside: Magnificent 7 reports could push QQQ to $630-640

- 💸 Rate cut = bullish: If FOMC cuts, natural reaction is UP for growth stocks

- 🎯 Institutions closing puts: The $29M put closing signals confidence in support - you're betting against that

- 🔥 Limited profit potential: Max gain only $100-200 per spread (20-40% ROI) vs 100% risk

- 📊 $620 resistance may not hold: If broken, no ceiling until $637 all-time high

Entry conditions (DO NOT enter unless ALL are met):

- ✅ QQQ trades above $618 (need cushion for spread to work)

- ✅ FOMC cut delivered and initial rally exhausts (don't fight the immediate reaction)

- ✅ RSI above 70 on daily chart (overbought confirmation)

- ✅ You can afford to lose ENTIRE $400-500 per spread

- ✅ You have experience trading directional spreads through major events

Scenario analysis:

- 📉 QQQ drops to $600: Puts worth $10 (spread max value), profit = $5-6 per spread (100-120% ROI)

- 📉 QQQ at $608: Profit = $2-3 per spread (40-60% ROI)

- 📉 QQQ at $605: Breakeven (max spread value but paid $4-5)

- 📈 QQQ at $615: Near breakeven, small loss

- 📈 QQQ above $618: Max loss of $4-5 per spread (100% loss)

Position sizing: Risk ONLY 1-3% of portfolio (this is pure directional speculation against the trend)

Exit plan:

- 🎯 Take profits at 50% gain ($200-250 profit per spread)

- ⚠️ Cut losses at 50% loss if QQQ breaks above $622

- ⏰ Don't hold past January 9 (close week before expiration to avoid gamma risk)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand you're betting AGAINST institutional positioning ($21M calls sold, $29M puts closed)

- ✅ Have traded bear put spreads through earnings seasons before

- ✅ Can withstand being wrong if January earnings surprise to upside

- ✅ Accept you're fighting 22.8% YTD momentum and strong underlying fundamentals

- ✅ Will STRICTLY follow exit rules (no "hoping it comes back")

Risk level: HIGH (directional bet against trend) | Skill level: Advanced only

Probability of profit: 30-35% (you're fading a bull market near all-time highs - low odds but asymmetric payoff IF you're right)

Alternative (safer) approach: WAIT until after January earnings. If Magnificent 7 beats cause rally to $625-630, THEN put on this spread with better risk/reward from higher strikes.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎯 Concentration risk is EXTREME: Top 10 holdings = 53.88% of assets1, with single-stock NVDA at 9.33%1 - ["If just one or two—say, Nvidia or a leading cloud provider—suffer a major rerating, QQQ can't hide in smaller holdings the way a broad index might."]43 A 15% drop in NVDA alone would cost QQQ 1.4%. The U.S. market's reliance on Magnificent Seven introduces systemic risks and raises questions about market sustainability.44

-

🚨 FOMC meeting uncertainty is REAL (Dec 9-10): Despite 83% probability of rate cut7, Powell said it's "not a foregone conclusion—far from it"13 and FOMC minutes revealed "many" members skeptical about further cuts.14 Wharton's Jeremy Siegel called this "the most uncertain FOMC meeting in years".16 A surprise NO CUT would trigger immediate 2-3% QQQ selloff. Even a cut with hawkish 2026 guidance could disappoint markets positioned for dovish tilt.

-

🤖 AI overinvestment bubble risk: Hyperscalers spending $150B+ annually on AI infrastructure with uncertain monetization timeline. ["There's the risk of overinvestment in AI technologies. If this dynamic shifts, the demand for AI chips could weaken, creating a ripple effect across the supply chain."]39 Any hyperscaler capex reduction in Q4/Q1 earnings would cascade through NVDA (-15-25%), AVGO (-10-15%), cloud providers (-5-10%), causing aggregate 5-10% QQQ decline. ["Investors have long been aware that Nvidia's elevated exposure to hyperscalers—which could sharply cut spending at any point—is a risk worth monitoring."]38

-

🏛️ Regulatory assault intensifying: ["As November 2025 unfolds, the landscape for technology giants is increasingly fraught with challenges. A wave of intensified regulatory scrutiny globally, coupled with ongoing antitrust battles in the United States, continues to cast a long shadow over the sector."]40 DOJ antitrust litigation against GOOGL (5.96% combined weight), FTC actions against AMZN (5.21%) and META (3.47%), App Store restrictions on AAPL (8.78%). ["There is now a clear focus on AI foundation models where agencies are keen to guard against deals that would lead to high levels of concentration."]41 Major action against top-3 holdings could reduce QQQ 5-15%.

-

🇨🇳 China geopolitical wildcard: Multiple exposure points - AAPL derives ~20% revenue from Greater China and faces [Huawei competition despite October's 37% sales surge]2945; NVDA subject to export restrictions on advanced AI chips; TSLA production in Shanghai with BYD competition; Taiwan strait tensions threaten semiconductor supply chain for entire QQQ. [AAPL already warned tariffs could add $1.1B to Q4 costs.]27 Any escalation would hit 30-40% of QQQ holdings simultaneously.

-

💰 Valuation stretched after 22.8% YTD gain: QQQ trading only 3.7% below all-time high3 at estimated 32-35x forward P/E (above 10-year average ~28x). Already up 22.8% YTD2 with most gains in rear-view mirror. At current multiples, requires PERFECT execution from Magnificent 7 earnings to avoid compression. Mean reversion to historical average valuation would mean 10-15% downside even WITH earnings growth. Zero margin for error - any disappointment magnified 3-4x at this valuation.

-

⚖️ Institutions capping upside signals limited conviction: The $21M covered call sale at $620 is telling - sophisticated players managing hundreds of millions are willingly capping gains at just 1% above current levels. If they expected rally to $640-650, they'd NEVER sell $620 calls. This suggests professional money managers see better risk/reward in collecting premium than betting on upside - a cautious signal when you're considering bullish positioning.

-

📊 January earnings "beat-and-drop" risk: Even if Magnificent 7 companies beat estimates, stocks often sell off on "good but not great" results when valuations are extended. NVDA, AAPL, MSFT, TSLA, META all trading at premium multiples - guidance must be SPECTACULAR to satisfy expectations. Historical pattern shows high-flyers often pull back 5-10% post-earnings even on beats due to profit-taking. With these 7 stocks representing 40%+ of QQQ5, coordinated profit-taking would hit ETF hard.

-

🎢 December Triple Witching volatility (Dec 19): Nasdaq reconstitution implementation (Dec 19)8 occurs on SAME DAY as quarterly triple witching when stock options, stock index futures, and stock index options all expire simultaneously.9 This creates amplified volatility and unpredictable price action as ~$400B in QQQ and index funds rebalance while derivative positions unwind. Typically see 1-3% intraday swings on triple witch days.

-

📈 Interest rate sensitivity if Fed stays hawkish: ["Rising yields usually pressure growth stocks (especially tech), as future earnings are discounted at higher rates."]12 Current 10-year at ~4.05%18 is manageable, but if Fed doesn't cut or yields spike above 4.50%, QQQ faces 5-8% potential decline from higher discount rates. Tech stocks have -0.33 correlation with yields20 (relatively weak), but at yields of 5%+ bonds compete strongly with equities.21 Upside in yields = downside in QQQ.

-

🌐 Macro recession risk in 2026: At current valuation, QQQ has ZERO recession protection. If economy weakens in 2026 (unemployment rises, consumer spending slows, corporate IT budgets cut), even strong AI narrative won't save tech from 30-40% correction. QQQ's tech concentration makes it most vulnerable major ETF in recession scenario - would underperform S&P 500 by 10-15% in downturn.

🎯 The Bottom Line

Real talk: The $76M in options activity today tells a clear story - institutions are managing risk, not making directional bets. They're selling $620 covered calls to generate income (saying "we're happy to sell here"), closing $29M in put protection (saying "we don't expect crashes"), and positioning for QQQ to consolidate in the $605-625 range through January expiration.

What this options flow reveals:

- ✅ Bullish, but not aggressively so: Closing put protection shows confidence, but capping upside at $620 shows limited conviction in explosive rally

- 📊 Expecting low volatility through year-end: Income generation via covered calls only makes sense if you expect range-bound trading

- 🎯 December catalysts seen as NEUTRAL: If they expected FOMC or reconstitution to be major positive, would never sell $620 calls; if expected major negative, would never close $590 puts

- 💰 Prefer collecting premium over speculation: $21M in covered call income suggests professional managers prioritizing steady returns over upside capture

- ⏰ Positioned for $596-625 range: Exactly matches December implied move bounds[^implied_move]

This is NOT a "buy everything" or "sell everything" signal - it's a "manage risk and collect income in range" signal.

If you own QQQ:

- ✅ Consider partial profit-taking: Up 22.8% YTD at all-time high area - nothing wrong with locking in gains2

- 💰 Mirror the smart money: Sell covered calls at $620-625 strikes to generate income (2%+ annualized yield)

- 📊 Keep long-term core holding: AI growth story, hyperscaler spending, Magnificent 7 earnings power remain intact

- ⚠️ Set mental stops: $605 is key support - if broken, expect move to $590-595

- 🎯 Trim overweight positions: If QQQ >30% of portfolio, consider rebalancing to 20-25% (concentration risk management)

If you're watching from sidelines:

- ⏰ Wait for December clarity: FOMC (Dec 9-10), reconstitution (Dec 12), and Triple Witch (Dec 19) create near-term uncertainty

- 🎯 Entry zones: $605-610 pullback would offer 2-3% margin of safety vs current price

- 📊 January earnings are THE catalyst: Magnificent 7 results (late Jan) will determine if QQQ breaks to $640+ or consolidates $590-620

- 🚀 Long-term remains compelling: QQQ delivered 25.58% total return in 202446, outperformed S&P 500 in 7 of last 10 years6, positioned for continued AI-driven growth

- 💰 Dollar-cost averaging beats timing: Rather than trying to time bottom, consider spreading entries over 4-6 weeks

If you're bearish:

- ⚠️ Don't fight 22.8% momentum into year-end: Institutions clearly not expecting crash (closed $29M puts)

- 📊 Better risk/reward AFTER January earnings: If Mag 7 beats cause rally to $625-630, THEN put on bearish positions from higher levels

- 🎯 Key breakdown level is $605: Below that, next stop is $590-595 (where puts were closed)

- ⏰ Timing matters: Premature bearish positioning risks getting steamrolled by December rally

Mark your calendar - Key dates:

- 📅 December 5 (Thursday) - Weekly options expiration (1.7% implied move window)[^implied_move]

- 📅 December 9-10 (Monday-Tuesday) - FOMC Meeting, 83% probability of 0.25% rate cut7

- 📅 December 10 (Tuesday) 2:00 PM ET - FOMC announcement and Powell press conference47

- 📅 December 12 (Thursday) - Nasdaq-100 reconstitution announcement8

- 📅 December 19 (Thursday) - Nasdaq reconstitution implementation + Quarterly Triple Witching89

- 📅 January 16, 2026 (Friday) - Monthly OPEX, expiration of $21M covered calls and institutional put positions

- 📅 January 29, 2026 (Wednesday after close) - [Microsoft, Meta, Tesla earnings]22

- 📅 January 30, 2026 (Thursday after close) - [Apple earnings (8.78% of QQQ)]22

- 📅 Mid-to-late February 2026 - [NVIDIA earnings (9.33% of QQQ, LARGEST HOLDING)]32

Final verdict:

QQQ's long-term AI-driven growth story remains INCREDIBLY compelling - [22.8% YTD performance]2, [Magnificent 7 earnings strength]37, [record NVDA data center revenues ($51.2B in Q3, up 66% YoY)]33, [Microsoft Azure $75B annual run rate growing 39%]2326, and [Apple's 37% China surge]29 are all real. The [December FOMC meeting carries 83% cut probability]7 which would provide tailwind, and [Nasdaq reconstitution typically adds strong growth companies]17 reinforcing tech leadership.

BUT - and this is critical - at 22.8% YTD gains, only 3.7% below all-time highs, with 32-35x forward P/E valuation, the risk/reward is NO LONGER heavily skewed to upside for NEW aggressive positioning.

The $76M in institutional options activity is a CLEAR signal: smart money is derisking at the peak (closing puts they no longer need), managing upside (selling covered calls at $620), and positioning for consolidation rather than explosion.

Be patient. Let December catalysts clear. The AI revolution will still be here in January, and you'll sleep better at night entering at $605-610 instead of chasing $620.

If you own it, consider selling some covered calls like the pros. If you're looking to enter, wait for better prices. If you're bearish, wait until after January earnings to short from strength.

This is a marathon, not a sprint. Protect your capital. Follow the smart money. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The options flow discussed represents sophisticated institutional strategies that may not be appropriate for retail traders. QQQ's 64% technology concentration creates elevated volatility and concentration risk. December FOMC and Nasdaq reconstitution events create binary risk with potential for 3-5% moves either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Invesco QQQ Trust (QQQ): The Invesco QQQ Trust tracks the Nasdaq-100 Index, providing exposure to 102 of the largest non-financial companies listed on the Nasdaq Stock Market. With $335.5 billion in assets under management and a 64% technology sector allocation4, QQQ is the premier ETF for concentrated exposure to U.S. innovation leaders including NVIDIA, Apple, Microsoft, and the Magnificent 7.

References

Footnotes

-

Stock Analysis, "QQQ Holdings List - Invesco QQQ Trust Series I", December 2025, https://stockanalysis.com/etf/qqq/holdings/ ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

StatMuse Money, "QQQ YTD Return", 2025, https://www.statmuse.com/money/ask/qqq-ytd-return ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

TS2 Space & Defense, "QQQ Stock Outlook Before December 1, 2025 Open: How Fund Outflows, Billionaire Buying and a Nasdaq 100 Shake‑Up Set the Stage", November 2025, https://ts2.tech/en/qqq-stock-outlook-before-december-1-2025-open-how-fund-outflows-billionaire-buying-and-a-nasdaq-100-shake%E2%80%91up-set-the-stage/ ↩ ↩2 ↩3

-

Invesco, "Holdings & Sector Allocations of Invesco QQQ", September 30, 2025, https://www.invesco.com/qqq-etf/en/about.html ↩ ↩2

-

TS2 Space & Defense, "QQQ Stock Outlook Before December 1, 2025 Open", November 2025, https://ts2.tech/en/qqq-stock-outlook-before-december-1-2025-open-how-fund-outflows-billionaire-buying-and-a-nasdaq-100-shake%E2%80%91up-set-the-stage/ ↩ ↩2 ↩3

-

Invesco, "Invesco QQQ ETF Performance", 2025, https://www.invesco.com/qqq-etf/en/performance.html ↩ ↩2

-

Growbeansprout, "US Fed Funds Interest Rate", November 30, 2025, https://growbeansprout.com/tools/fedwatch ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7

-

Trading Calendar, "Index Rebalance Calendar", 2025, https://www.tradingcalendar.com/index-rebalance ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

Brian Freitas / SmartKarma, "NASDAQ 100 Index Rebalance: Six Changes at the Annual Reconstitution", 2024, https://www.smartkarma.com/insights/nasdaq-100-index-rebalance-six-changes-at-the-annual-reconstitution ↩ ↩2 ↩3 ↩4 ↩5

-

Federal Reserve, "Federal Reserve Board - Federal Reserve issues FOMC statement", October 29, 2025, https://www.federalreserve.gov/newsevents/pressreleases/monetary20251029a.htm ↩ ↩2

-

Stocktwits, "Fed Rate Cut Odds For December Nearly Double After NY Fed's Williams Signals 'Room For Further Adjustment'", November 2025, https://stocktwits.com/news-articles/markets/equity/fed-rate-cut-probability-december-shoots-up-ny-fed-room-for-cut/cLPMplbREOV ↩

-

Fisher Investments, "Do Rising Yields Trouble Tech?", 2025, https://www.fisherinvestments.com/en-us/insights/market-commentary/do-rising-yields-trouble-tech ↩ ↩2 ↩3

-

CNBC, "Fed minutes show divide over October rate cut and cast doubt about December", November 19, 2025, https://www.cnbc.com/2025/11/19/fed-minutes-october-2025.html ↩ ↩2 ↩3

-

CNBC, "Fed minutes show divide over October rate cut and cast doubt about December", November 19, 2025, https://www.cnbc.com/2025/11/19/fed-minutes-october-2025.html ↩ ↩2

-

Federal Reserve, "FOMC Minutes, October 28-29, 2025", November 2025, https://www.federalreserve.gov/monetarypolicy/fomcminutes20251029.htm ↩ ↩2

-

Fortune, "December Fed cut: FOMC members in for 'rare, suspenseful' meeting", November 25, 2025, https://fortune.com/2025/11/25/wall-street-divided-fed-meeting-base-rate-december-cut/ ↩ ↩2 ↩3

-

Nasdaq, "Annual Changes to the Nasdaq-100 Index", December 13, 2024, https://www.nasdaq.com/press-release/annual-changes-nasdaq-100-indexr-2024-12-13 ↩ ↩2 ↩3

-

Advisor Perspectives, "10-Year Treasury Yield Long-Term Perspective: October 2025", November 3, 2025, https://www.advisorperspectives.com/dshort/updates/2025/11/03/10-year-treasury-yield-long-term-perspective-october-2025 ↩ ↩2

-

Axis Intelligence, "10-Year Treasury Yield: 2025 Outlook, Market Impacts, and Strategic Insights", 2025, https://axis-intelligence.com/10-year-treasury-yield-2025/ ↩ ↩2

-

Morningstar, "Busting the Tech-Stock, Bond-Yield Connection Myth", 2025, https://www.morningstar.com/markets/busting-tech-stock-bond-yield-connection-myth ↩ ↩2

-

T. Rowe Price, "How high could the 10-year U.S Treasury yield go?", 2025, https://www.troweprice.com/financial-intermediary/us/en/insights/articles/2025/q1/how-high-could-the-10-year-us-treasury-yield-go.html ↩ ↩2

-

Wall Street Horizon, "Earnings Season Kicks into High Gear with Magnificent 7 Reports", 2025, https://www.wallstreethorizon.com/blog/Earnings-Season-Kicks-into-High-Gear-with-Magnificent-7-Reports ↩ ↩2 ↩3 ↩4

-

Futurum Group, "Microsoft Q4 FY 2025 Results Driven by 39% Azure Growth", July 2025, https://futurumgroup.com/insights/microsoft-q4-fy-2025-earnings-beat-driven-by-39-azure-growth/ ↩ ↩2

-

Microsoft, "FY25 Q4 - Intelligent Cloud Performance", July 2025, https://www.microsoft.com/en-us/investor/earnings/fy-2025-q4/intelligent-cloud-performance ↩

-

Data Center Dynamics, "Microsoft Azure brought in $75bn for FY2025, company deployed 2GW data center capacity", July 2025, https://www.datacenterdynamics.com/en/news/microsoft-azure-brought-in-75bn-for-fy2025-company-deployed-2gw-data-center-capacity/ ↩

-

GeekWire, "Microsoft beats expectations, reveals Azure revenue for the first time — $75 billion a year", July 2025, https://www.geekwire.com/2025/microsoft-posts-strong-quarter-cites-broad-ai-and-cloud-growth-as-azure-revenue-tops-75b-annually/ ↩ ↩2

-

Nasdaq, "Magnificent 7 Earnings: What to Expect (AMZN, AAPL, META and MSFT)", 2025, https://www.nasdaq.com/articles/magnificent-7-earnings-what-expect-amzn-aapl-meta-and-msft ↩ ↩2 ↩3 ↩4

-

Yahoo Finance, "iPhone 16 Sales Soar 20% in China Debut as Demand Returns", October 2025, https://finance.yahoo.com/news/apple-iphone-16-sales-soar-055818158.html ↩

-

Apple Insider, "One in four smartphones sold in China is an iPhone", November 2025, https://appleinsider.com/articles/25/11/18/one-in-four-smartphones-sold-in-china-is-an-iphone ↩ ↩2 ↩3 ↩4

-

Insider Monkey, "Apple's iPhone Sales in China Rebound 8% in Q2 2025 Driven by Price Cuts, iPhone 16 Demand", 2025, https://www.insidermonkey.com/blog/apples-iphone-sales-in-china-rebound-8-in-q2-2025-driven-by-price-cuts-iphone-16-demand-1565257/ ↩

-

Yahoo Finance, "Apple's iPhone Sales Surge in China to Take 25% Market Share", 2025, https://finance.yahoo.com/news/apple-iphone-sales-surge-china-040850440.html ↩

-

NVIDIA, "NVIDIA Announces Financial Results for Third Quarter Fiscal 2026", November 2025, https://nvidianews.nvidia.com/_gallery/download_pdf/691e34d93d633290a88deeef/ ↩ ↩2

-

NVIDIA, "NVIDIA Announces Financial Results for Third Quarter Fiscal 2026", November 2025, https://nvidianews.nvidia.com/_gallery/download_pdf/691e34d93d633290a88deeef/ ↩ ↩2

-

Futurum Group, "NVIDIA Earnings Preview: Blackwell Demand Set to Fuel Another Blowout", 2025, https://futurumgroup.com/insights/nvidia-earnings-preview-blackwell-demand-set-to-fuel-another-blowout/ ↩ ↩2

-

IO Fund, "Nvidia CEO Predicts AI Spending Will Increase 300%+ in 3 Years", 2025, https://io-fund.com/semiconductors/data-center/nvidia-ceo-predicts-ai-spending-will-increase-300-percent-in-3-years ↩

-

TweakTown, "NVIDIA Q3 2025 results: $57 billion revenue, Blackwell AI GPU sales are 'off the charts'", November 2025, https://www.tweaktown.com/news/108974/nvidia-q3-2025-results-dollars57-billion-revenue-blackwell-ai-gpu-sales-are-off-the-charts/index.html ↩ ↩2

-

Nasdaq, "Breaking Down Magnificent 7 Earnings Results", 2025, https://www.nasdaq.com/articles/breaking-down-magnificent-7-earnings-results ↩ ↩2 ↩3

-

Schwab, "Nvidia Earnings Ahead: AI Demand, Margins In-Focus", 2025, https://www.schwab.com/learn/story/semiconductor-earnings-preview ↩ ↩2

-

Financial Content Markets, "The Silicon Supercycle: How AI Chip Demand is Reshaping the Semiconductor Industry", November 10, 2025, https://markets.financialcontent.com/wral/article/tokenring-2025-11-10-the-silicon-supercycle-how-ai-chip-demand-is-reshaping-the-semiconductor-industry ↩ ↩2 ↩3

-

Financial Content Markets, "Big Tech Under Siege: Regulatory Crackdown and Market Reliance Fuel Uncertainty", November 6, 2025, http://markets.chroniclejournal.com/chroniclejournal/article/marketminute-2025-11-6-big-tech-under-siege-regulatory-crackdown-and-market-reliance-fuel-uncertainty ↩ ↩2

-

Baker McKenzie, "Driving Tech Growth Amid Regulatory and Antitrust Scrutiny", February 2025, https://www.bakermckenzie.com/en/insight/publications/2025/02/driving-tech-growth-amid-regulatory-and-antitrust-scrutiny ↩ ↩2

-

Growth Shuttle, "Invesco QQQ Trust: Analyzing the Risks and Rewards in 2025's Tech-Heavy ETF Landscape", 2025, https://growthshuttle.com/invesco-qqq-trust-analyzing-the-risks-and-rewards-in-2025s-tech-heavy-etf-landscape/ ↩

-

TS2 Space & Defense, "QQQ Stock Outlook Before December 1, 2025 Open", November 2025, https://ts2.tech/en/qqq-stock-outlook-before-december-1-2025-open-how-fund-outflows-billionaire-buying-and-a-nasdaq-100-shake%E2%80%91up-set-the-stage/ ↩ ↩2 ↩3

-

Financial Content Markets, "Big Tech Under Siege: Regulatory Crackdown and Market Reliance Fuel Uncertainty", November 6, 2025, http://markets.chroniclejournal.com/chroniclejournal/article/marketminute-2025-11-6-big-tech-under-siege-regulatory-crackdown-and-market-reliance-fuel-uncertainty ↩ ↩2

-

South China Morning Post, "Apple's China iPhone sales face headwinds in second half as Huawei remains a strong rival", 2025, https://www.scmp.com/tech/big-tech/article/3316846/apples-china-iphone-sales-face-headwinds-second-half-huawei-remains-strong-rival ↩ ↩2 ↩3

-

FinanceCharts, "Invesco QQQ Trust (QQQ) Total Return YTD, TTM, 3Y, 5Y, 10Y, 20Y", 2025, https://www.financecharts.com/etfs/QQQ/performance/total-return ↩

-

Federal Reserve, "The Fed - Meeting calendars and information", 2025, https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm ↩