💾 SNDK Diagonal Call Spread — Smart Money Bets $11.8M on Sandisk's Long Runway! 🚀

📅 March 11, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $11.8M net into a sophisticated diagonal call spread on Sandisk (SNDK) — buying a 10-month LEAP at $750 while simultaneously selling a deep-ITM near-term call at $610 to fund part of the position. This isn't your average bullish bet — it's a chess move combining premium collection with long-term upside conviction on the #1 performing S&P 500 stock of the past two years. Translation: Big money is positioning for SNDK to keep running well past $750 while getting paid to wait.

📊 Company Overview

Sandisk Corporation (SNDK) is the hottest semiconductor stock in the market right now:

- Market Cap: $91.3 Billion

- Industry: Computer Storage Devices (NAND Flash Memory)

- Current Price: $634.21 (up +105% YTD, following a +559% gain in 2025!)

- Primary Business: One of the five largest NAND flash memory suppliers globally — vertically integrated, producing substantially all flash chips at in-house manufacturing sites. The only pure-play publicly traded NAND company after spinning off from Western Digital in February 2025.

💰 The Option Flow Breakdown

📊 The Tape (March 11, 2026 @ 12:10:42) — Diagonal Call Spread

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:10:42 | SNDK | BUY | CALL | 2027-01-15 | $17M | $750 | 1K | 134 | 979 | $634.21 | $175 | SNDK20270115C750 |

| 12:10:42 | SNDK | SELL | CALL | 2026-03-20 | $5.2M | $610 | 1K | 1.5K | 979 | $634.21 | $53 | SNDK20260320C610 |

Net Premium Paid: ~$11.8M ($17M long − $5.2M sold)

🤓 What This Actually Means — Diagonal Spread Mechanics Explained

Let me break down exactly what's happening here because this is NOT a simple bullish call buy. This is a diagonal call spread — two legs, two different expirations, working together as one position.

Leg 1 — Buying the LEAP (Long-dated, OTM, expensive):

- 💸 $17M paid for 979 contracts of the January 15, 2027 $750 calls at $175/contract

- 🎯 Strike is $115.79 OTM from current price of $634.21 (18.2% out-of-the-money)

- ⏰ 305 days to expiration — giving the position 10 full months to work

- 🚀 This is the long-term bullish engine of the trade, giving unlimited upside above $750 through January 2027

Leg 2 — Selling the Short-dated ITM call (Near-term, deep ITM, premium collection):

- 💰 $5.2M collected for 979 contracts of the March 20, 2026 $610 calls at $53/contract

- 📊 Strike is $24.21 ITM — SNDK is currently at $634.21, so this call is already in the money

- ⏰ Only 9 days to expiration — expires at OPEX on March 20

- 🛡️ This is the premium financing leg — collecting cash today by giving away the near-term upside above $610

Why sell a deep-ITM near-term call?

Real talk: When you sell a deep-ITM call with only 9 days left, you're essentially collecting the remaining time value on that contract. The $53 premium on a $610 call when SNDK trades at $634.21 means you're collecting ~$28.79 of pure time value (the rest is intrinsic value already). That $5.2M effectively reduces the cost of the January LEAP from $17M down to $11.8M.

The trade-off? If SNDK stays above $610 through March 20 (very likely given stock is at $634), the short call expires in-the-money. But that's fine — the trader already owns the stock position or is comfortable managing the assignment. The key insight is: they paid $11.8M net for 10 months of SNDK upside above $750, partially funded by collecting near-term ITM premium.

What does this signal?

- 🐋 This is NOT a casual retail trade — 979 contracts on a $634 stock represents exposure to ~97,900 shares

- 📊 The $750 strike is meaningful — it aligns closely with analyst price targets (Cantor Fitzgerald: $800, Citigroup: $750, average street target: $761)

- ⏰ January 2027 expiration captures Q3 FY2026 earnings (April/May 2026), Q4 FY2026 (July/August), and potentially Q1 FY2027 — the full NAND supercycle ramp

- 💡 Net cost of $11.8M is lower than the raw $17M because of smart premium engineering

Unusualness factor: With only 134 contracts of open interest on the $750 January 2027 call before this trade hit, this 979-contract buy represents 7.3x the existing open interest in a single print. That's a serious statement of conviction.

📈 Technical Setup / Chart Check-Up

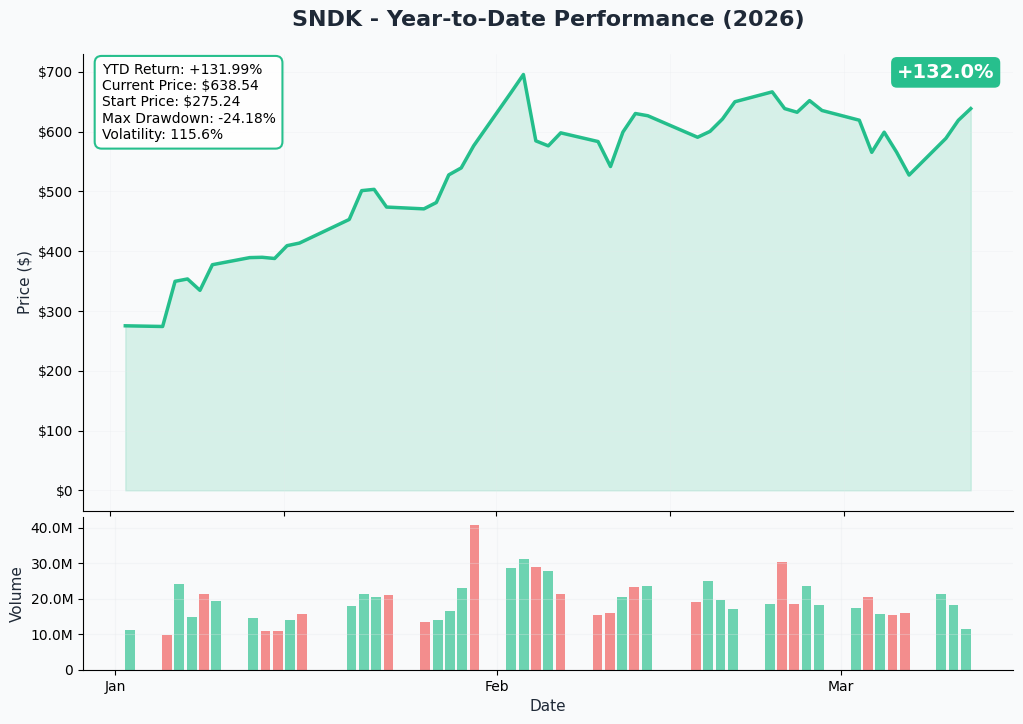

YTD Performance Chart

Buckle up — SNDK's 2026 YTD chart looks like a rocket ship. From ~$305 at year-end 2025, the stock has surged to $634.21, a +105% YTD gain layered on top of the already-staggering +559% full-year 2025 return. That's not a typo.

The 52-week range tells the whole story: $28.27 to $725.00. From sub-$30 to $634 in less than a year, driven by the AI-fueled NAND super-cycle. A major leg higher came on March 9, 2026, when SNDK surged +11.6% in a single session after Phison's CEO confirmed every NAND manufacturer told them 2026 supply is completely sold out. That's the kind of fundamental news that rerates a stock permanently.

Key chart observations:

- 🚀 Parabolic momentum: Stock has barely looked back since the January 29 earnings blowout

- 📈 Breakout from $450 zone in late February after secondary catalysts stacked up

- 🎢 Beta of 4.80 — this stock moves 4-5x the market on any given day

- ⚠️ Potential consolidation zone: After a 105% YTD run, digestion periods are normal and healthy

- 📊 Volume surges on catalyst days confirm institutional accumulation, not retail momentum chasing

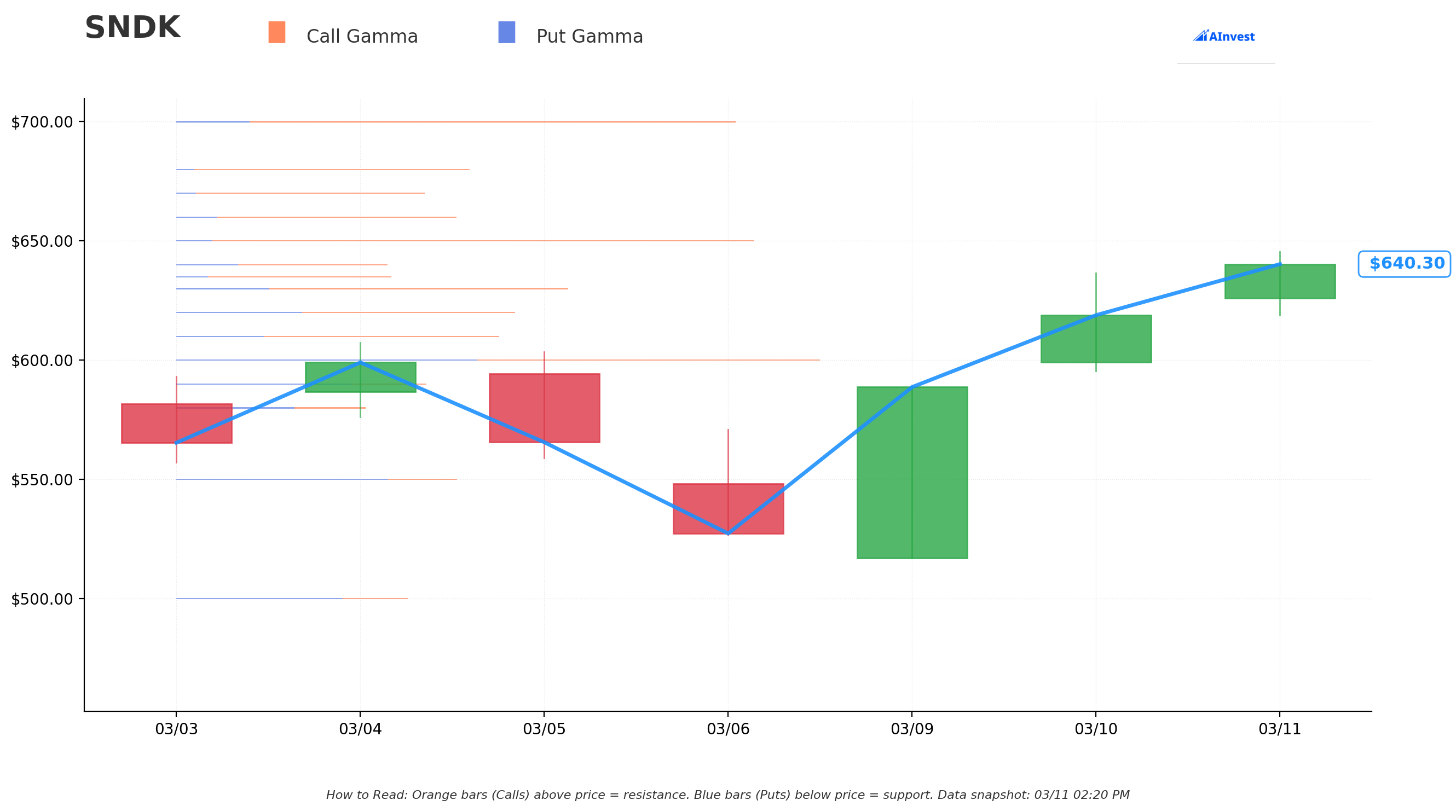

🔵🟠 Gamma-Based Support & Resistance Analysis

Current Price: $641.33 (at time of GEX snapshot)

The gamma exposure (GEX) map reveals the price levels where market makers have the heaviest options hedging obligations — these act as natural magnets and barriers:

🟠 Resistance Levels Above Price (Call Gamma):

- $650 — Immediate ceiling with 1.95B total gamma (1.35% above price) — strongest nearby resistance

- $660 — Secondary resistance at 943M gamma (2.9% overhead) — sellers likely emerge here

- $670 — Extended resistance at 831M gamma (4.5% overhead)

- $680 — Additional ceiling at 980M gamma (6.0% overhead)

- $700 — Major resistance zone at 1.89B total gamma (9.1% overhead) — key psychological and technical level

🔵 Support Levels Below Price (Put Gamma):

- $630 — Immediate support at 1.29B total gamma (1.77% below) — strongest nearby floor

- $620 — Secondary support at 1.12B gamma (3.3% below) — solid cushion zone

- $610 — Third support at 1.06B gamma (4.9% below) — note: this is EXACTLY where the short call is struck! Not coincidental.

- $600 — Major structural support at 2.11B total gamma (6.4% below) — the highest total gamma level overall, meaning dealers are heavily positioned here

- $550 — Extended floor at 886M gamma (14.2% below) — deep support if things get ugly

Net GEX Bias: Bullish — Total call gamma ($24.4B) nearly doubles total put gamma ($10.97B), confirming the overall positioning skew is to the upside.

What this means for the trade: The short $610 call is struck right at a major gamma support level. If SNDK pulls back toward $610 over the next 9 days (a ~3.9% drop), market maker hedging activity at that level would likely slow the decline and provide a natural floor — smart positioning by this trader.

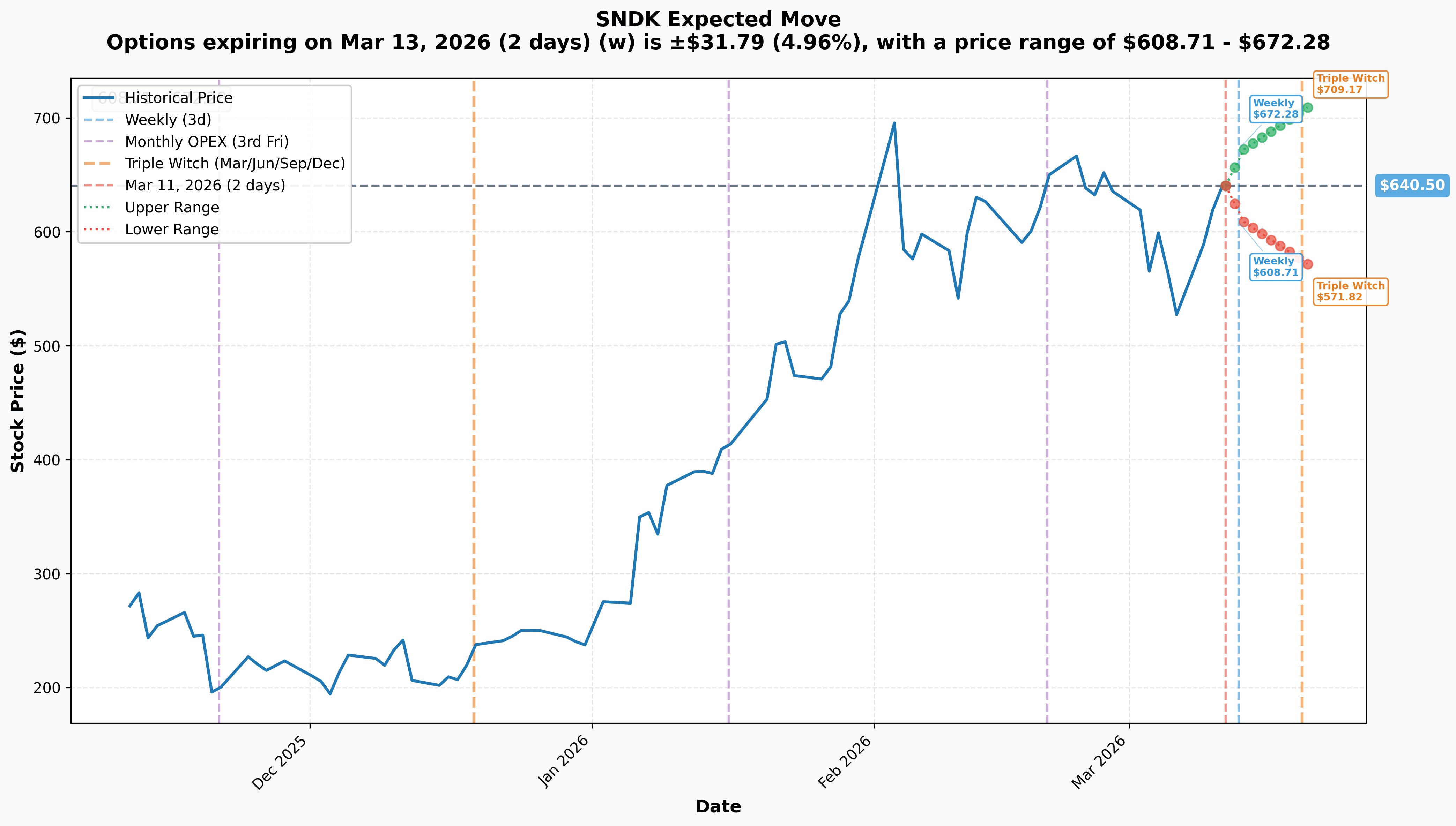

📊 Implied Move Analysis

Options market pricing in SNDK expected moves:

- 📅 Weekly (March 13 — 2 days): ±$31.79 (±4.96%) → Range: $608.71 to $672.28

- 📅 Monthly OPEX (March 20 — 9 days — THIS SHORT CALL EXPIRES HERE!): ±$68.68 (±10.72%) → Range: $571.82 to $709.17

Translation for regular folks: The options market is pricing a ±$32 swing just by Friday — that's serious weekly volatility in dollar terms. By March 20 OPEX (when the short $610 call expires), the implied range stretches all the way from $572 to $709.

This is critical for understanding the diagonal spread:

- 📈 Bull scenario by March 20: SNDK rallies to $700+. The short $610 call expires deep ITM and is likely assigned/closed, but the long $750 LEAP appreciates significantly on the move.

- 🎯 Base case by March 20: SNDK consolidates between $630-$660. The short call decays toward intrinsic value, the $750 LEAP holds its premium with 10 months of runway.

- 📉 Bear scenario by March 20: SNDK pulls back toward $572 (implied lower range). The short $610 call loses intrinsic value rapidly, potentially expiring worthless or near-worthless — the trader pockets the full $5.2M on the short leg.

Key insight: The $750 LEAP needs SNDK to rally another 18.2% from current levels to reach the strike. The implied move data shows the market prices a 10.7% range through March OPEX alone — if that bullish momentum extends through April earnings and beyond, the $750 target becomes very plausible.

🎪 Catalysts

🔥 Recent Catalysts — Already Happened

✅ NAND Supply Sold Out for 2026 (March 9-10, 2026) This was the gasoline that lit the most recent fire. Phison's CEO confirmed every NAND manufacturer said 2026 is sold out — triggering SNDK's +11.6% single-day surge on March 9. Samsung is reportedly set to double NAND flash prices in Q2 2026 after already raising them ~100% in Q1. No new non-China NAND capacity is being added in 2026 or potentially 2027.

✅ Q2 FY2026 Blowout Earnings (January 29, 2026) The numbers were staggering. Revenue of $3.03B (+61% YoY) vs $2.64B consensus — a 14.8% beat. Non-GAAP EPS of $6.20 vs $3.33 consensus — an 86% beat. Non-GAAP gross margin hit 51.1%, up 18.6 percentage points year-over-year. Stock surged 9.21% in after-hours on the print.

✅ HBF Standardization Kick-Off with SK Hynix (February 25, 2026) Sandisk and SK Hynix formalized joint efforts to standardize High Bandwidth Flash (HBF) memory under the Open Compute Project. HBF targets 1.6 TB/s bandwidth (50x faster than PCIe 5.0 SSDs) with 8-16x the capacity of HBM at similar cost — an entirely new memory tier for AI inference.

✅ S&P 500 Inclusion (November 28, 2025) Sandisk joined the S&P 500 just nine months after its spinoff — triggering mandatory passive fund buying and significantly broadening the institutional investor base overnight.

✅ Post-Earnings Analyst Upgrade Wave (January 30, 2026)

| Firm | Action | Price Target |

|---|---|---|

| Cantor Fitzgerald | Maintained Overweight | $800 |

| Raymond James | Upgraded to Outperform | $725 |

| Jefferies | Maintained Buy | $700 |

| Morgan Stanley | Maintained Overweight | $690 |

| Citigroup | Maintained Buy | $750 |

Street consensus: 14 Buy, 0 Sell with an average 12-month price target of $761 — implying ~20% upside from current levels. The $750 strike on this diagonal spread is literally the consensus target.

🚀 Upcoming Catalysts — What's Coming

📅 March 20, 2026 — Triple Witch OPEX (9 Days Away!) This is when the short $610 call leg expires. With a ±10.7% implied move through this date, there's real uncertainty about where SNDK settles. Heavy gamma positioning at $600 and $610 could act as a magnetic floor if SNDK pulls back.

📅 Late April / Early May 2026 — Q3 FY2026 Earnings (THE BIG ONE) This is the most important catalyst in the next 6 months. Management guided:

- 💰 Revenue: $4.40B — $4.80B (52%+ sequential growth at the midpoint)

- 📊 Non-GAAP Gross Margin: 65% — 67% (a jaw-dropping 14-16 percentage point sequential expansion!)

- 💵 Non-GAAP EPS: $12.00 — $14.00 (vs. $6.20 last quarter!)

If Sandisk delivers on this guidance, the stock's earnings power narrative fundamentally re-rates higher. This catalyst falls squarely within the January 2027 LEAP's time window.

📅 H1 2026 — 256TB Enterprise SSD Commercial Availability The SN670 128TB and Ultra QLC 256TB enterprise SSDs target U.2 form factor commercial availability in H1 2026, opening the hyperscaler AI datacenter storage market at massive density.

📅 H2 2026 — First HBF Samples + Hyperscaler Qualifications Sandisk targets first HBF memory samples in H2 2026, with AI inference devices shipping in early 2027. Two hyperscalers already in qualification for the Stargate enterprise SSD product line, with more queued.

📅 Ongoing — NAND Pricing Escalation NAND pricing is projected to increase another 70-100% over the course of 2026, with Q1 2026 contract prices already up 37%+ QoQ. Every new pricing update is a catalyst.

🎲 Price Targets & Probabilities

Using gamma levels, implied moves, and the full catalyst stack, here are the scenarios through January 15, 2027 (LEAP expiration):

📈 Bull Case (35% probability)

Target: $750 — $900

- 💪 Q3 FY2026 earnings crush guidance ($5B+ revenue, EPS toward $14 high end)

- 🚀 NAND pricing continues surging — no new non-China capacity arriving in 2026-2027 means supply crunch persists

- 🤖 First HBF samples delivered H2 2026, validating the AI inference memory thesis with SK Hynix

- 📊 Hyperscaler qualifications convert to volume orders, data center becomes largest NAND end market

- 📈 Breakout above gamma resistance at $700 triggers momentum run toward Cantor's $800 target

- 💥 Short squeeze potential — 7.5% short interest with "extreme" squeeze score from S3 Partners adds rocket fuel

LEAP P&L in Bull Case:

- SNDK at $800 by Jan 2027: $750 call worth ~$50+, net position profitable

- SNDK at $900 by Jan 2027: $750 call worth ~$150+, massive gains on the 979-contract position

🎯 Base Case (45% probability)

Target: $650 — $750 (grind higher, digest gains)

- ✅ Solid Q3 earnings delivery near guidance midpoints ($4.6B revenue, ~$13 EPS)

- 📊 Stock consolidates between $630-$700 gamma zone through Q2, then re-rates higher on earnings

- 🔄 Near-term resistance at $650 and $700 gamma walls slows but doesn't stop the uptrend

- 💤 Short call at $610 expires in/near-the-money on March 20, trader manages or rolls the leg

- 📅 Position reaches its full potential as catalyst stack plays out through the LEAP's time window

- 🎯 $750 strike becomes reachable by Q3-Q4 2026 on continued NAND pricing strength

📉 Bear Case (20% probability)

Target: $500 — $600 (cycle turn fear)

- 😰 Memory cycle reversal — Samsung capacity expansion spooks the market

- 🇨🇳 Chinese NAND producers (YMTC) accelerate domestic capacity, softening the supply narrative

- 📉 Q3 guidance miss or gross margin disappointment — priced for perfection at current levels

- 💸 Western Digital secondary offering overhang (WDC still holds ~5.13% = 7.51M shares) creates selling pressure

- 🔨 Break below $600 gamma support triggers technical cascade toward $550

- 📊 LEAP loses significant time value; position shows unrealized loss but retains optionality through Jan 2027

💡 Trading Ideas

🛡️ Conservative: "The Patience Play" — Wait for the Dust to Settle on March OPEX

Play: Hold cash and watch March 20 OPEX play out before entering any SNDK position

Why this works:

- ⏰ With a ±10.7% implied move through March 20, SNDK could trade anywhere from $572 to $709 in the next 9 days — that's a $137 range on a $634 stock

- 💸 Implied volatility is elevated right now, making options expensive across all expirations

- 📊 After OPEX on March 20, IV typically contracts sharply — you'll get better prices on any options strategy

- 🎯 Wait for SNDK to find a post-OPEX base, then look for a pullback to the $600-$620 gamma support zone for entry

- ✅ The strong gamma support at $600 (highest total GEX level at 2.11B) and $610 means any dip there gets bought hard by dealer hedging flows

Action plan:

- 👀 Watch March 20 close — see where SNDK pins relative to the $610 short call level

- 🎯 Look for SNDK to test $620-$630 gamma support post-OPEX for a stock entry or long call entry

- 📅 Mark April/May earnings as the next major binary event — position before then for Q3 guidance reaffirmation

Cost: $0 upfront | Max loss: Opportunity cost only | Risk level: Minimal

⚖️ Balanced: "Follow the Smart Money Lite" — Buy a Smaller LEAP Call Spread

Play: Buy the June 2026 $700/$800 call spread to get defined bullish exposure at lower cost

Structure: Buy June 2026 $700 calls, Sell June 2026 $800 calls

Why this works:

- 💰 A $700/$800 call spread captures most of the upside if SNDK runs from $634 to the $750-$800 analyst target zone, at a fraction of the cost of an outright LEAP

- 🎯 Defined risk — you know the maximum loss on day one (the net debit paid)

- 📊 June 2026 captures Q3 earnings in April/May — the single biggest catalyst in the near term

- 🤖 If NAND pricing keeps ripping and Q3 guidance is confirmed or raised, this spread could go full value

- ⚖️ Selling the $800 call funds part of the position — just like the whale is doing on the other leg

Estimated parameters (indicative — verify live quotes):

- 💸 Estimated net debit: $15-$25 depending on IV at entry

- 📈 Max profit: $100 per spread if SNDK above $800 at June expiration

- 📉 Max loss: Net debit paid (fully defined)

- 🎯 Breakeven: ~$715-$725 at expiration

Position sizing: Risk only 3-5% of portfolio — this is a directional bet, not a hedge

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: "Ride the Supercycle" — Short-Duration Call on Earnings Momentum

Play: Buy April 2026 $680/$720 call spread targeting the Q3 earnings catalyst

Why this could work:

- 💥 Q3 FY2026 earnings (late April/early May) guided $12-$14 non-GAAP EPS vs $6.20 last quarter — that's roughly doubling earnings in one quarter

- 📊 If SNDK delivers even the low end of guidance ($12 EPS), the stock will reprice meaningfully higher

- 🎢 With a beta of 4.80, any positive earnings surprise gets amplified — SNDK regularly moves 9-12% on earnings prints

- 🎯 $680 breakeven is only 7.2% above current price — achievable if any positive catalyst hits before April OPEX

- 🔥 The $700 gamma resistance level will be the key test — a confirmed break above it could trigger a run to $750

Estimated parameters (indicative):

- 💸 Estimated net debit: $8-$14 per spread

- 📈 Max profit: $40 per spread if SNDK above $720 at April expiration

- 📉 Max loss: Net debit paid (fully defined risk)

- 🎯 Breakeven: ~$688-$694 at expiration

- 🎰 Risk/reward: Up to 3:1 if spread goes full value

CRITICAL WARNING:

- ⚠️ Earnings binary events can go either way — SNDK has a beta of 4.80, so misses hurt BADLY

- 💸 Short-dated options lose time value rapidly — enter as close to the catalyst as practical

- ❌ Do NOT size this aggressively — this is high-risk, high-reward speculation

Risk level: HIGH (can lose full premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎢 Extreme volatility (beta 4.80): SNDK moves 4-5x the broader market. A 2% S&P selloff could translate to a 10% SNDK drop in a single day. After a ~1,000% rally from its spinoff IPO, the stock has NO margin of safety on valuation — priced for perfection.

-

📉 Memory cycle reversal — the eternal NAND risk: Every prior memory supercycle has eventually reversed. If Samsung or Chinese manufacturers accelerate capacity additions, NAND prices could peak and roll over faster than the market expects. The resulting gross margin compression would be violent.

-

🇨🇳 China NAND expansion: YMTC and other Chinese NAND producers continue adding domestic capacity. While currently not competitive at the leading-edge enterprise level, longer-term they erode the supply tightness narrative. Geopolitical trade restrictions could also cut both ways.

-

💔 Short squeeze math cuts both ways: Short sellers have accumulated nearly $30 billion in mark-to-market losses in 2026 — they're in pain and could accelerate a squeeze. But when/if shorts finally cover or the squeeze exhausts, the stock can reverse just as violently. The S3 Partners "extreme" squeeze score is a double-edged sword.

-

📊 Western Digital overhang: WDC still holds ~5.13% of SNDK (7.51M shares) worth approximately $4.7B at current prices. They've already done two secondary offerings and could do more. Each offering creates supply pressure.

-

🏭 BiCS8 execution risk: The transition to BiCS8 (218-layer) technology as majority of bit production is technically complex. Yield issues, ramp delays, or competitive technology leapfrog from Micron or Samsung could impair the gross margin expansion story.

-

🤖 AI demand deceleration: SNDK is priced for AI data center storage demand continuing to accelerate. Any signal that AI buildout is slowing — more compute efficiency, model optimization reducing storage needs, or hyperscaler capex pullback — hits the stock hard at these multiples.

-

📉 Macro headwinds amplified by high beta: A broader semiconductor rotation, rising rate environment, or recession fear could pressure SNDK regardless of fundamentals. A stock with a 4.80 beta in a down tape gets punished disproportionately.

🎯 The Bottom Line

Real talk: Someone just structured an $11.8M net diagonal call spread that says SNDK is heading to $750+ over the next 10 months — and they were smart enough to partially finance that conviction by collecting $5.2M of near-term ITM premium. This is chess, not checkers.

What this diagonal structure tells us:

- 🎯 The $750 strike is intentional — it's the street's consensus price target, implying this trader believes consensus is conservative

- 💰 The short March $610 call signals comfort with the current price level — they don't need SNDK to drop to make this trade work

- ⏰ The January 2027 LEAP window captures every major catalyst: Q3 earnings, Q4 earnings, HBF sample delivery, and full BiCS8 production ramp

- 📊 Selling the near-term ITM call is a statement: "I'm long-term bullish and willing to give up near-term upside to reduce my entry cost"

- 🐋 This is sophisticated institutional-grade positioning — not panic buying, not a lottery ticket

If you're bullish on SNDK:

- ✅ The $600-$630 gamma support zone is your entry target — wait for pullbacks there

- 📅 Mark April/May Q3 earnings as the must-watch catalyst — a $12-$14 EPS delivery re-rates this stock

- 🚀 Longer-term thesis: HBF partnership with SK Hynix + 256TB enterprise SSDs positions SNDK at the center of AI data center storage for years

- 🛡️ Size appropriately — this is a 4.80 beta stock, not a bond substitute

If you're watching from the sidelines:

- ⏰ Post-March 20 OPEX is the cleanest entry window — IV contracts, gamma resets, price discovery continues

- 🎯 Entry around $600-$620 gamma support with a defined risk strategy (call spread, not naked calls) is the disciplined approach

- 📊 Watch for confirmation: NAND pricing updates, hyperscaler qualification announcements, and BiCS8 mix commentary

Key dates to mark:

- 📅 March 20, 2026 — Triple Witch OPEX, short $610 call expires, position restructured

- 📅 Late April / Early May 2026 — Q3 FY2026 earnings ($12-$14 EPS guided)

- 📅 H1 2026 — 256TB enterprise SSD commercial availability

- 📅 H2 2026 — First HBF samples delivered; hyperscaler qualifications progress

- 📅 January 15, 2027 — Long $750 LEAP call expires

Final verdict: Sandisk is the purest-play beneficiary of the AI-driven NAND supply crunch, with supply sold out through 2026, pricing surging, and Q3 guidance representing some of the most explosive quarter-over-quarter earnings growth in the S&P 500. The diagonal spread structure captured here is a high-conviction, cost-efficient way to express a $750+ price target without paying full price for the LEAP. The 14 analyst Buy ratings with zero Sells and $761 average price target are in the same neighborhood. Whether you follow this trade or use it as a signal, the smart money's message is clear: the NAND supercycle isn't over.

Manage your risk. Stay sized right. And don't forget — beta of 4.80 means the ride will be wild in both directions. 💪

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. The unusual options activity described reflects a single transaction and does not imply the trade will be profitable or that you should replicate it. Diagonal spreads and LEAP options involve complex mechanics including assignment risk, time decay, and volatility sensitivity — thoroughly understand the risks before trading. SNDK is an extremely high-volatility stock (beta 4.80) with potential for rapid and substantial losses. Always do your own research and consider consulting a licensed financial advisor before making any investment decisions.

About Sandisk Corporation: Sandisk Corporation is one of the five largest suppliers of NAND flash memory semiconductors globally, with a vertically integrated manufacturing model and a market cap of $91.3 billion. Spun off from Western Digital in February 2025, it is the only major pure-play publicly traded NAND company and has been the top-performing S&P 500 stock over the trailing twelve months.