🐋 WBD $7.1M Bullish Call Bet - Smart Money Loading Up Ahead of M&A Fireworks!

January 28, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $7.1 MILLION on WBD calls this morning at 11:22:47! This whale bought 19,630 contracts of the $25 strike calls expiring March 20th - a slightly in-the-money bullish bet with two competing acquisition offers on the table ($27.75 from Netflix, $30 from Paramount Skydance). With WBD trading at $28.00, this trader is positioning for upside through Q4 earnings on February 20th and the shareholder vote expected in April. Translation: Institutional money is betting the bidding war pushes WBD higher from here.

Company Overview

Warner Bros. Discovery (WBD) is one of the world's largest media and entertainment conglomerates, currently at the center of a historic M&A bidding war:

- Market Cap: $69.6B

- Industry: Cable & Other Pay Television Services

- Current Price: $28.00 (near 52-week high of $30.00)

- Primary Business: HBO Max streaming (128M subscribers), Warner Bros. film studios ($4B+ 2025 box office), HBO premium content, global cable networks (CNN, TNT, Discovery, HGTV), and the upcoming DC Universe franchise slate

The Option Flow Breakdown

The Tape (January 28, 2026 @ 11:22:47):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:22:47 | WBD | MID | BUY | CALL $25 | 2026-03-20 | $7.1M | $25 | 20K | 59K | 19,630 | $28.00 | $3.62 |

What This Actually Means

This is a bullish conviction bet on WBD through the March triple witch expiration. Here's the breakdown:

- Huge premium committed: $7.1M ($3.62 per contract x 19,630 contracts)

- Slightly in-the-money: The $25 strike sits $3.00 below the current $28.00 stock price, giving the buyer $3.00 of intrinsic value baked in from day one

- Strategic strike selection: By going ITM, this trader gets a higher delta (~0.75-0.80), meaning the position moves nearly dollar-for-dollar with the stock - this is a leveraged stock replacement, not a lottery ticket

- Massive size: 19,630 contracts controls ~1.96 million shares worth roughly $55M of WBD stock

- Classified BTO (Buy to Open): This is a NEW position, not a hedge roll or closing trade

- Z-Score: 3.88 (EXTREMELY UNUSUAL): This kind of single-ticket call buying happens only a few times a year in WBD options

What's really happening here: This trader is essentially buying leveraged exposure to the M&A outcome. With Netflix offering $27.75/share and Paramount Skydance bidding $30/share, the floor appears well-supported. The March 20th expiration captures both Q4 earnings (February 20) and positions ahead of the expected April shareholder vote. At $3.62 per contract with $3.00 intrinsic, they're only paying $0.62 in time value - that's cheap insurance on a stock sitting between two takeover bids.

Unusual Score: EXTREMELY UNUSUAL (Z-Score 3.88) - Vol/OI ratio of 0.34 with 20K volume against 59K open interest shows this is a meaningful addition to an already active strike. This level of single-ticket call buying is rare for WBD and signals strong institutional conviction.

Technical Setup / Chart Check-Up

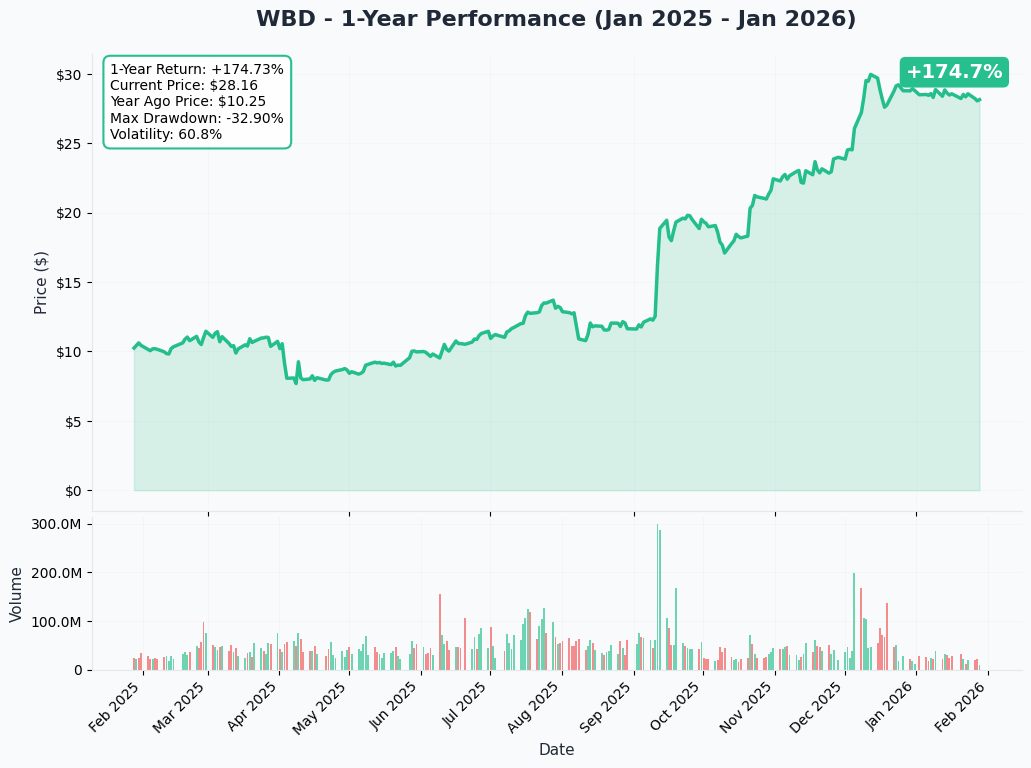

YTD Performance Chart

WBD has been on an absolute tear - up 175.5% over the past year from its 52-week low of $7.52 to the current $28.00. The stock's transformation from a $7 debt-laden media dinosaur to a $28 M&A darling is one of the most dramatic turnarounds in recent market history.

Key observations:

- M&A floor established: The Netflix deal at $27.75 and Paramount's $30 bid have created a visible price floor since December 2025

- Trading above Netflix offer: Current price of $28.00 sits ABOVE the $27.75 Netflix bid, suggesting the market assigns meaningful probability to either a deal sweetener or the Paramount $30 bid succeeding

- 52-week high proximity: Stock is just 6.7% below its $30.00 high (set on the Paramount bid announcement)

- Volume confirmation: Average daily volume of 23.5M shares shows heavy institutional interest and tight liquidity

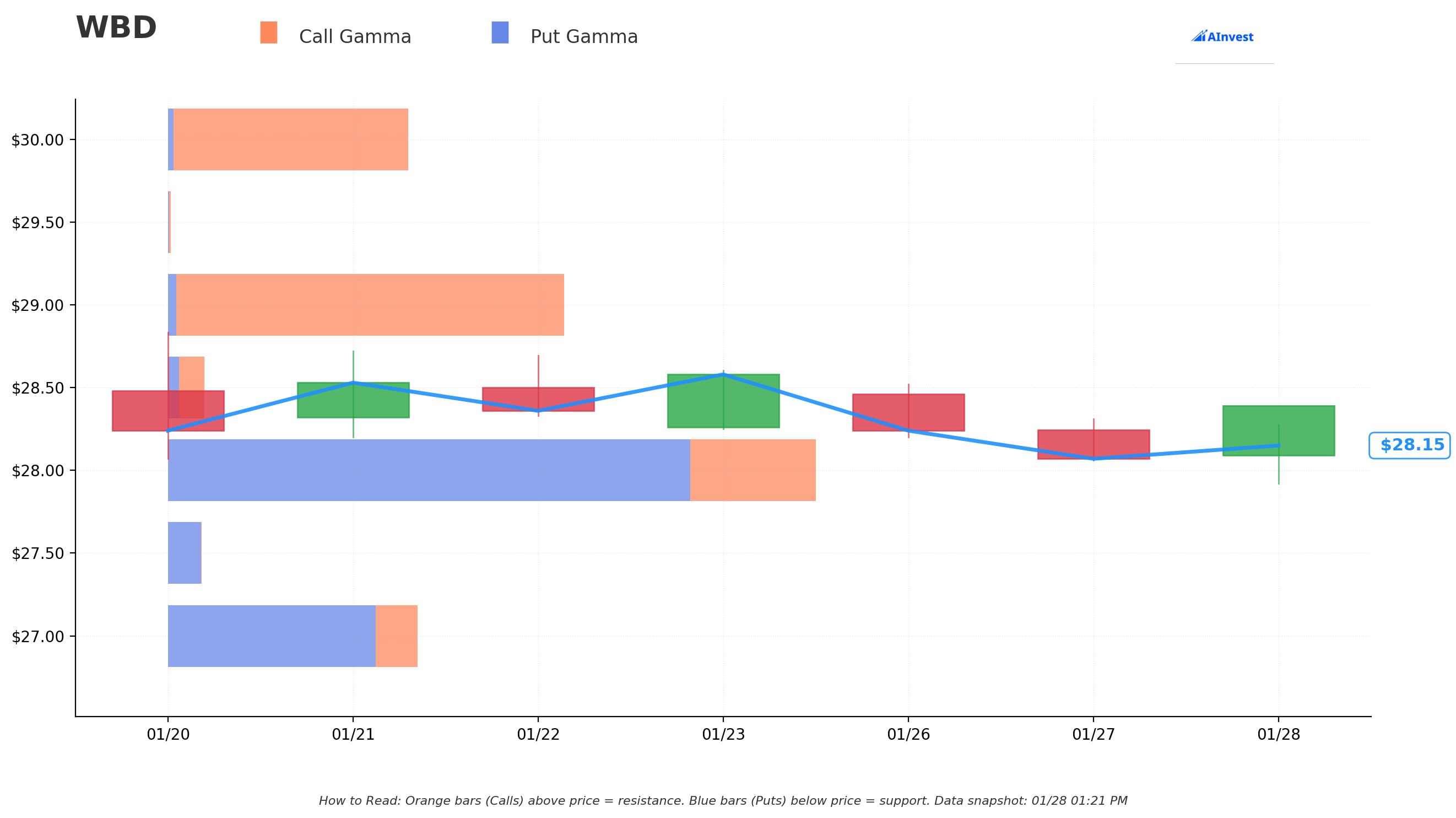

Gamma-Based Support & Resistance Analysis

Current Price: $28.00

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

Support Levels (Put Gamma Below Price):

- $28.00 - Strongest support with 125.9B total gamma exposure (massive floor right at current price!)

- $27.00 - Secondary support at 49.3B gamma (backs up against Netflix offer price)

- $26.00 - Tertiary support at 21.2B gamma

- $25.00 - Deep support at 30.0B gamma (this trade's strike price - not coincidental!)

- $24.00 - Extended floor at 9.1B gamma

Resistance Levels (Call Gamma Above Price):

- $28.50 - Immediate overhead at 7.5B gamma (light resistance)

- $29.00 - Major ceiling with 80.4B gamma (STRONGEST RESISTANCE - dealers will sell into rallies here)

- $30.00 - Critical level at 48.2B gamma (Paramount's $30 bid price creates massive options interest)

- $31.00 - Extended resistance at 12.2B gamma

- $32.00 - Upper ceiling at 6.8B gamma

What this means for traders: WBD is sitting right on top of its strongest gamma support at $28, with massive resistance at $29.00 (80.4B gamma). The price is pinned between two M&A gravity wells - the Netflix offer floor at $27.75 and the Paramount bid ceiling at $30.00. The $29 level is the key to watch - a break above that opens the path to $30.00 where the Paramount bid creates a natural magnet.

Notice anything? The call buyer struck at $25 where there's 30.0B gamma support - they're buying deep enough to have intrinsic value protection while capturing full upside toward $29-30. Smart positioning.

Net GEX Bias: Bullish (215.4B call gamma vs 197.4B put gamma) - Overall dealer positioning leans bullish, supporting the thesis that upside moves have more room to run.

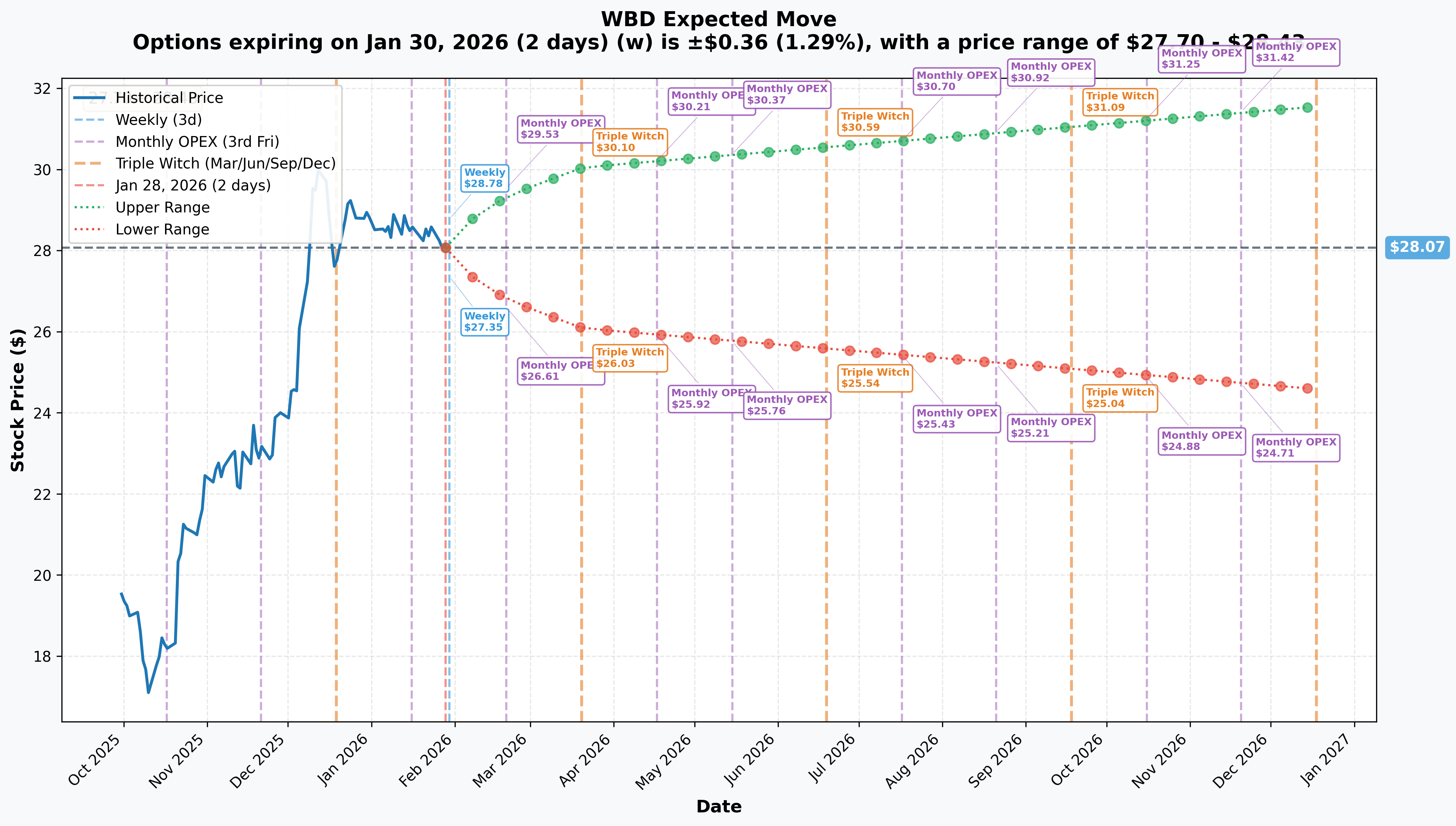

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 30 - 2 days): +/-$0.36 (+/-1.3%) -> Range: $27.70 - $28.43

- Monthly OPEX (Feb 20 - 23 days): +/-$1.28 (+/-4.6%) -> Range: $26.78 - $29.35

- Quarterly Triple Witch (Mar 20 - 51 days - THIS TRADE!): +/-$1.98 (+/-7.1%) -> Range: $26.08 - $30.05

- Yearly LEAPS (Dec 18 - 324 days): +/-$3.48 (+/-12.4%) -> Range: $24.58 - $31.55

Translation for regular folks: Options traders are pricing in a modest 1.3% move ($0.36) by Friday - WBD is range-bound in the short term. But through February OPEX (which captures Q4 earnings on February 20), the market expects a 4.6% move ($1.28) - enough to push the stock to either $26.78 or $29.35.

The March 20th expiration (when this $7.1M trade expires) has an upper range of $30.05 - almost exactly Paramount's $30/share bid price. The implied move suggests the market sees a realistic path to the Paramount offer level by triple witch. On the downside, the lower range of $26.08 sits below the Netflix offer of $27.75, reflecting some deal-break risk.

Key insight: The relatively low implied volatility (7.1% through March) for a stock with two competing takeover bids reflects the market's view that the M&A floor limits downside. This makes call options relatively cheap - and may be exactly why this institutional buyer is loading up.

Catalysts

Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings Report - February 20, 2026

WBD reports fiscal Q4 results on February 20, 2026. Wall Street consensus and key expectations:

- Revenue: $10.37B (+0.8% YoY)

- EPS: $0.10/share (+162.5% YoY)

- Streaming Subscribers: Tracking toward 130M+ (Q3 was 128M with +16% YoY growth)

- Content Revenue: $3.44B (+16.1% YoY) driven by Superman's $616M worldwide box office

- Key metrics to watch: Streaming profitability trajectory toward $1.3B target, debt reduction updates, and any commentary on Netflix/Paramount deal process

Near-Term Catalysts (Q1-Q2 2026)

WBD Shareholder Vote on Netflix Deal - Expected April 2026

The revised all-cash transaction at $27.75/share is expected to go to a shareholder vote by April 2026. This is a critical binary catalyst:

- If approved: Path clears for closing in mid-2027, stock likely gravitates toward $27.75 deal price

- If rejected or deal collapses: $5.8B breakup fee payable to WBD by Netflix; Paramount Skydance's $30/share bid could re-emerge as the winning offer

Senate Antitrust Hearings - Early 2026

Netflix co-CEO Ted Sarandos will testify before the U.S. Senate regarding the merger's antitrust implications. Senate antitrust subcommittee chairman Mike Lee has stated the deal "appears likely to raise serious antitrust issues". The DOJ has already issued a second request for information. Any regulatory clarity - positive or negative - could move the stock significantly.

HBO Max UK/Ireland Launch - March 2026

HBO Max set to launch in the UK and Ireland in March 2026, completing the European rollout. Combined with the recent Germany/Italy/Austria launch on January 13 and the password sharing crackdown, WBD is targeting 150M global streaming subscribers by end of 2026.

Discovery Global Separation - Expected Q3 2026

WBD plans to complete its tax-free separation into two publicly traded companies: Warner Bros. (streaming + studios, CEO: Zaslav) and Discovery Global (networks + CNN, CEO: Wiedenfels). This separation is a precondition for the Netflix acquisition. Discovery Global has scheduled its first upfront presentation for May 13, 2026.

Recent Catalysts (Already Happened)

Netflix Acquisition Agreement - December 5, 2025

Netflix announced a definitive agreement to acquire Warner Bros. for $27.75/share ($82.7B enterprise value). The deal was amended to all-cash on January 20, 2026.

Paramount Skydance Hostile Counter-Bid - December 8, 2025

Three days later, Paramount Skydance submitted a rival all-cash bid at $30/share ($108.4B valuation). Paramount filed a lawsuit and announced plans for a proxy fight. The WBD Board unanimously recommended shareholders reject the Paramount offer.

Superman Box Office Blockbuster - 2025

James Gunn's Superman grossed over $616M worldwide, and WBD's Motion Picture Group exceeded $4B in 2025 box office revenue, leading the global industry.

Debt Reduction Progress

WBD has reduced gross debt from $55B to ~$34B, with debt-to-equity hitting 0.96x - the lowest in 10 years.

Price Targets & Probabilities

Using gamma levels, implied move data, and the M&A backdrop, here are the scenarios through the March 20th expiration:

Bull Case (30% probability)

Target: $30.00-$32.00

How we get there:

- Paramount Skydance raises its bid or succeeds in its proxy fight, pushing price toward or above $30

- Netflix sweetens the deal to compete (analysts have a street-high price target of $35)

- Q4 earnings on February 20 show streaming subscribers surging past 130M with improved profitability

- Antitrust hearings go smoothly, reducing regulatory overhang

- Breakout above $29.00 gamma resistance triggers technical rally to $30.00 (Paramount bid level)

- Implied move upper range of $30.05 by March 20 aligns perfectly with this target

Call P&L in Bull Case:

- Stock at $30 on March 20: Calls worth $5.00, profit = $1.38/share x 19,630 = $2.7M gain (38% ROI)

- Stock at $32 on March 20: Calls worth $7.00, profit = $3.38/share x 19,630 = $6.6M gain (93% ROI)

Base Case (50% probability)

Target: $27.50-$29.00 range (M&A HOLDING PATTERN)

Most likely scenario:

- Stock continues trading between the Netflix floor ($27.75) and the Paramount ceiling ($30)

- Q4 earnings meet consensus ($10.37B revenue, $0.10 EPS) - solid but no fireworks

- Regulatory process continues without clear resolution, keeping deal uncertainty elevated

- Market waits for April shareholder vote for clarity

- Gamma support at $28 and resistance at $29 keep price range-bound

- Volatility stays compressed as M&A dynamics dominate fundamental trading

Call P&L in Base Case:

- Stock at $28.00 on March 20: Calls worth $3.00, loss = -$0.62/share x 19,630 = -$1.2M loss (17% loss)

- Stock at $29.00 on March 20: Calls worth $4.00, profit = $0.38/share x 19,630 = $746K gain (10.5% ROI)

This is the call buyer's sweet spot: Even in a range-bound scenario, the ITM strike means they only lose the time value ($0.62/share) if the stock stays flat. The asymmetry is favorable - limited downside if stock stays near $28, significant upside if it moves toward $30.

Bear Case (20% probability)

Target: $24.00-$26.00 (DEAL COLLAPSE RISK)

What could go wrong:

- DOJ or Senate action signals the Netflix deal will be blocked - stock could drop below the $27.75 offer as deal premium evaporates

- Both deals fall apart due to regulatory opposition, stock reprices to standalone value ($10-15 range in worst case)

- Q4 earnings disappoint, highlighting linear TV decline (-17% ad revenue) without M&A premium support

- Broader market selloff drags merger arb spreads wider

- Break below $27.00 gamma support triggers cascade toward $25.00

Call P&L in Bear Case:

- Stock at $25 on March 20: Calls worth ~$0.05, loss = -$3.57/share x 19,630 = -$7.0M loss (99% loss)

- Stock at $26 on March 20: Calls worth $1.00, loss = -$2.62/share x 19,630 = -$5.1M loss (72% loss)

Why only 20% probability: Two competing bidders at $27.75 and $30 create a strong floor. Both buyers have committed significant resources and legal teams. Even if one deal fails, the other likely persists. A total deal collapse would require BOTH bids to be withdrawn or blocked - a low-probability outcome given the $5.8B breakup fee providing downside cushion.

Trading Ideas

Conservative: Merger Arb Stock Position

Play: Buy WBD shares at $28.00 with a target of $27.75 (Netflix floor) to $30.00 (Paramount ceiling)

Why this works:

- Two competing bids create a visible floor at $27.75 - your downside is ~1% to the Netflix deal price

- If Paramount succeeds or Netflix sweetens, you capture $2-4/share upside (7-14%)

- No theta decay unlike options - you can hold patiently through the shareholder vote in April

- $5.8B breakup fee from Netflix provides financial cushion even in deal-break scenarios

- Dividend-like return: Even if stock sits at $28 for 3 months waiting for the vote, you're not losing premium

- Q4 earnings on February 20 could provide a near-term catalyst

Position sizing: Allocate 5-10% of portfolio. Set a stop at $25.00 (below both gamma support and the $25 strike where this whale is positioned)

Risk level: Low-Moderate | Skill level: Beginner-friendly

Balanced: March $27/$30 Call Spread

Play: Buy March 20 $27 calls, sell March 20 $30 calls

Structure: Bull call spread targeting the M&A range

Why this works:

- Captures the $27.75-$30.00 deal range with defined risk

- Buying $27 ITM call (~$1.50-1.80 intrinsic) reduces theta exposure

- Selling $30 call offsets premium cost and caps risk at Paramount's bid level

- Max profit if stock at or above $30 at March expiration (Paramount bid succeeds)

- Defined risk: Can only lose the net debit paid

Estimated P&L:

- Net debit: ~$1.50-2.00 per spread

- Max profit: $3.00 - debit = ~$1.00-1.50 per spread (50-75% ROI)

- Max loss: Net debit paid (~$1.50-2.00)

- Breakeven: ~$28.50-$29.00

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Copy the Whale - March $25 Calls

Play: Buy March 20 $25 calls mimicking the institutional flow

Why this could work:

- Riding the same trade as the $7.1M whale - they did the homework, you follow the money

- $25 strike ITM means high delta (~0.78) - moves nearly dollar-for-dollar with stock

- Only $0.62 in time value at $3.62 cost - most of your premium is intrinsic value

- If Paramount bid at $30 succeeds: calls worth $5.00 = 38% return

- If Netflix sweetens to $29: calls worth $4.00 = 10.5% return

- 51 days to expiration captures earnings AND shareholder vote buildup

Why this could hurt:

- $3.62 per contract means $362 per contract commitment

- If both deals collapse and stock drops to $20, you lose nearly everything

- Regulatory headline risk could gap the stock down overnight

- Time decay accelerates in the last 30 days

Position sizing: Risk 3-5% of portfolio maximum. This is a leveraged M&A bet, not a core holding.

Risk level: HIGH (leveraged directional bet on M&A outcome) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

M&A deal collapse is a REAL risk: Both the Netflix and Paramount deals face significant regulatory headwinds. The DOJ has issued a second request, Senate antitrust chairman publicly opposes the deal, and bipartisan opposition spans both parties. If BOTH deals fail, WBD's standalone value is dramatically lower - the stock was trading at $10-11 before the Netflix announcement. That's a potential 60%+ drawdown from current levels.

-

Binary event risk around shareholder vote: The expected April shareholder vote on the Netflix deal is an all-or-nothing moment. WBD's Board supports the Netflix deal while rejecting Paramount, but shareholders may disagree. The outcome could swing the stock $5+ in either direction overnight.

-

Political interference wildcard: President Trump stated the Netflix deal "could be a problem" and will "be involved." Unpredictable political commentary could cause sharp volatility at any time without warning.

-

Linear TV secular decline accelerating: Advertising revenue fell 17% ex-FX in Q3 2025. Cable cord-cutting is accelerating, and the loss of NBA live rights removes a key audience anchor for TNT. If M&A deals fail, the standalone business faces serious revenue headwinds.

-

Valuation makes NO sense on standalone basis: Forward P/E of 109.22 vs industry average of 12.05 is almost entirely M&A premium. Strip out the deal premium, and WBD's fundamentals don't support anywhere near current prices. This is NOT a stock you want to own if the deals evaporate.

-

Debt load still massive: Even after reducing from $55B to $34B in gross debt, WBD carries 3.3x net leverage. The planned separation puts majority of debt onto Discovery Global, which could struggle as a standalone entity.

-

Execution risk on corporate separation: Splitting into two public companies while managing an $82.7B acquisition is operationally complex. The separation is a PRECONDITION for the Netflix deal - any delays push back the entire timeline.

-

Streaming competition remains fierce: Reaching 150M subscribers by end of 2026 requires adding 22M subscribers in ~5 quarters against Netflix (~300M+), Disney+ (~157M), and Amazon Prime Video. International expansion costs could pressure margins.

The Bottom Line

Real talk: Someone just dropped $7.1M on WBD March $25 calls while the stock sits between two competing acquisition bids. This is smart, calculated positioning - not a reckless gamble. The trader chose an ITM strike ($25 vs $28 stock) for high delta exposure, paying only $0.62 in time value while getting $3.00 of intrinsic protection. They're betting the bidding war continues and the stock moves toward the $29-30 range by March expiration.

What this trade tells us:

- Sophisticated player believes the M&A floor holds and upside exists toward the Paramount $30 bid

- ITM strike selection shows this is a stock replacement trade, not a speculative lottery ticket

- March expiration is strategic: captures Q4 earnings (February 20), regulatory headlines, and positions ahead of the April shareholder vote

- The Z-score of 3.88 (EXTREMELY UNUSUAL) means this level of single-ticket conviction in WBD is rare - maybe a handful of times per year

If you're bullish on the M&A outcome:

- Consider buying shares at $28.00 with a $25.00 stop - you're getting in above the Netflix deal but below the Paramount bid

- The $27/$30 call spread captures the deal range with defined risk

- Q4 earnings on February 20 could provide a near-term catalyst if streaming growth continues

- Watch the $29.00 gamma resistance level - a break above opens the door to $30.00

If you're watching from the sidelines:

- This is fundamentally an M&A trade, not a fundamental investment. Know what you're buying.

- The stock's 175.5% rally is almost ENTIRELY driven by deal speculation

- If you can't stomach a potential 60% drawdown if both deals collapse, stay away

- Wait for regulatory clarity from the Senate hearings before committing capital

- February 20 earnings is a good "check-in" point to reassess the thesis

If you're bearish:

- Don't fight the M&A floor at $27.75 unless you have strong conviction that regulators will block BOTH deals

- Put spreads below $25 capture deal-break scenarios with defined risk

- Watch for DOJ or Senate actions signaling a deal block - that's your entry trigger for bearish positioning

- The $28.00 gamma support must break before downside momentum accelerates

Mark your calendar - Key dates:

- January 30 (Friday) - Weekly OPEX (+/-1.3% implied move)

- February 20 (Friday) - Q4 2025 earnings report + Monthly OPEX (+/-4.6% implied move)

- March 20 (Friday) - Triple witch expiration, THIS $7.1M call trade expires (+/-7.1% implied move)

- April 2026 (expected) - WBD shareholder vote on Netflix deal

- May 13 - Discovery Global first upfront presentation

- Q3 2026 - Discovery Global separation expected

Final verdict: WBD is a merger arbitrage play, pure and simple. The $7.1M call buy signals institutional confidence that the bidding war supports current prices and likely drives them higher. With two competing bids ($27.75 and $30.00), the risk/reward tilts favorably for patient longs as long as at least one deal remains alive. But this is NOT a buy-and-forget stock - the outcome is binary, the regulatory risk is real, and the entire premium evaporates if both deals collapse.

If you believe the deals survive regulatory scrutiny, the asymmetry favors the long side here. But size your position for the possibility that you're wrong - because in M&A land, anything can happen.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. WBD's current valuation is almost entirely driven by M&A speculation, creating significant binary event risk. If both acquisition deals fail, the stock could decline 50-60%+ from current levels. Always do your own research and consider consulting a licensed financial advisor before trading. The institutional call buy reflects one trader's view and does not guarantee the trade will be profitable.

About Warner Bros. Discovery: Warner Bros. Discovery is a global media and entertainment company operating HBO Max streaming (128M subscribers), Warner Bros. film studios, HBO premium content, and global cable networks (CNN, TNT, Discovery, HGTV). The company has a market cap of $69.6B in the Cable & Other Pay Television Services industry and is currently the subject of competing acquisition bids from Netflix ($27.75/share) and Paramount Skydance ($30/share).