💰 SNDK $24M Deep ITM Call Sale - Institutional Profit-Taking Before Earnings! 📊

📅 January 28, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out $24 MILLION worth of deep in-the-money SNDK calls at 12:29:56 today - selling 499 contracts of the $50 strike calls expiring March 20th, with the stock trading at $523. This is NOT a bearish bet. With the stock up over 1,000% since its February 2025 spinoff and earnings hitting TOMORROW (January 29), this trader is locking in massive profits on a position that was likely opened near the spinoff. Translation: Smart money cashing the winning lottery ticket before the next draw.

📊 Company Overview

SanDisk Corporation (SNDK) is a pure-play NAND flash memory powerhouse riding the AI storage revolution:

- Market Cap: $70.6 Billion

- Industry: Computer Storage Devices

- Current Price: $523.00 (all-time high territory)

- Headquarters: Milpitas, CA | 11,000 employees

- Primary Business: Among the world's top five NAND flash memory semiconductor suppliers. SanDisk manufactures most of its flash chips through a Japanese joint venture with Kioxia, then converts them into SSDs for consumer and enterprise applications. Spun off from Western Digital in February 2025.

💰 The Option Flow Breakdown

The Tape (January 28, 2026 @ 12:29:56):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:29:56 | SNDK | MID | SELL | CALL $50 | 2026-03-20 | $24M | $50 | 499 | 670 | 499 | $523.00 | $473.22 |

🤓 What This Actually Means

This is a profit-taking exit - someone closing a deep in-the-money long call position. Here is the breakdown:

- 💸 Massive cash-out: $24M collected ($473.22 per contract x 499 contracts)

- 🎯 Deep ITM call: The $50 strike with stock at $523 means these calls have $473 of intrinsic value alone - they are essentially stock proxies

- 📊 STC (Sell to Close): This is classified as closing an existing long call position, NOT opening a new short

- 🏦 Profit realization: If this trader bought these calls anywhere near the $50 level when SNDK was trading sub-$100 post-spinoff, they are sitting on 5-10x returns

- ⏰ Pre-earnings timing: Cashing out the day before Q2 FY2026 earnings (January 29) - locking in gains before the binary event

- 🔥 Unusual score: Z-Score of 6.11 (EXTREMELY UNUSUAL) with volume/OI ratio of 0.745 - this kind of deep ITM exit on this scale happens only a few times per year

What is really happening here: Think of deep in-the-money calls as a leveraged stock position. This trader likely accumulated SNDK $50 calls during the early post-spinoff days when the stock was trading under $100. With the stock now at $523, these calls have appreciated enormously. Rather than hold through tomorrow's earnings - which could swing the stock 10%+ in either direction - they are converting paper profits into cold hard cash. This is textbook institutional risk management: take the money off the table before the coin flip.

Why sell calls instead of selling stock? Deep ITM calls let institutions gain leveraged exposure with less capital. Now that SNDK has run up 1,000%+, these calls behave identically to stock (delta ~1.0), so selling them is functionally the same as selling shares - but with better capital efficiency.

📈 Technical Setup / Chart Check-Up

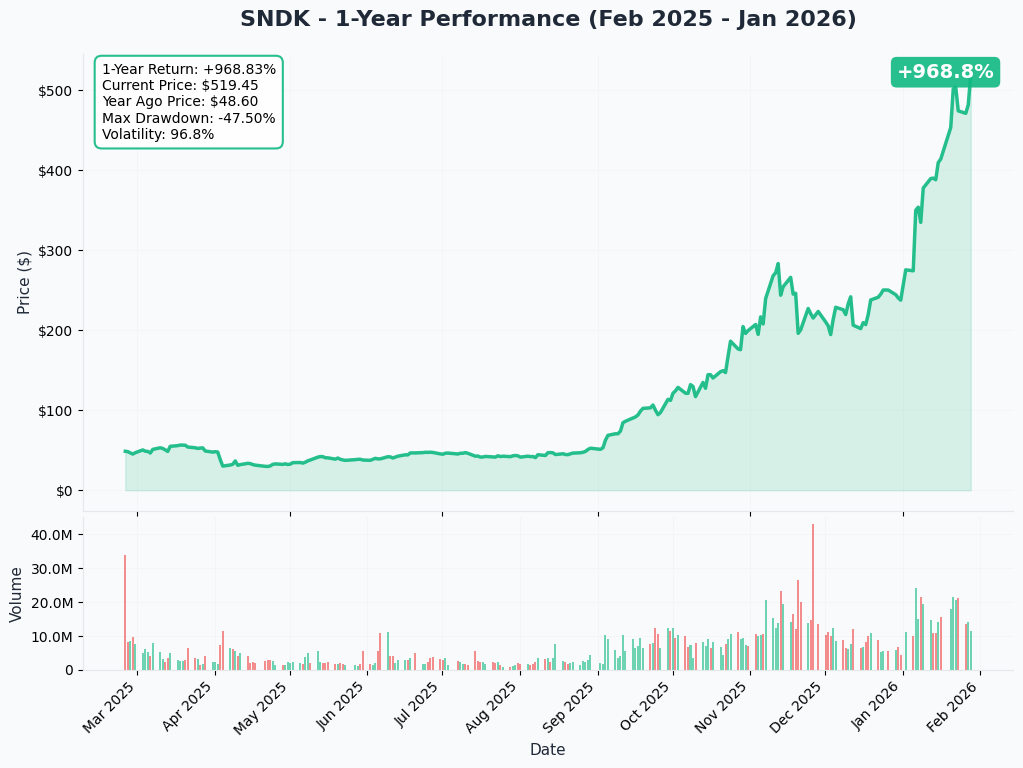

YTD Performance Chart

SNDK has been on a historic tear - up over 1,000% since its February 2025 spinoff from Western Digital at around $45 per share. The stock is now trading at all-time highs near $523, having more than doubled YTD 2026 alone (+105%). This is one of the most explosive rallies in semiconductor history, driven by the NAND flash super-cycle and insatiable AI data center storage demand.

Key observations:

- 🚀 Parabolic rally: From $27.89 low to $523 in under 12 months - vertical price action

- 📈 YTD 2026 performance: +105% already, making it one of the best performing large-caps this year

- 🎢 Extreme volatility: A stock that moves this fast can reverse just as quickly

- 📊 Outrunning analysts: Trading 30% ABOVE the average analyst price target of $364

- ⚠️ Stretched valuation: At 21x+ forward P/E, priced for near-perfect execution

Gamma-Based Support & Resistance Analysis

Current Price: $522.73

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Below Price):

- $520 - Immediate support with strongest nearby gamma floor (0.85 net GEX) - just 0.5% below current price

- $500 - Major structural support at 0.56 net GEX (4.3% below) - psychological round number

- $490 - Secondary support at 0.30 net GEX (6.3% below)

- $485 - Put-heavy zone with -0.53 net GEX (7.2% below) - negative gamma means dealers amplify moves here

- $475 - Deep support at -0.60 net GEX (9.1% below) - another put-dominant zone

- $470 - Extended floor at -0.38 net GEX (10.1% below)

- $450 - Disaster floor at -0.05 net GEX (13.9% below)

🟠 Resistance Levels (Above Price):

- $550 - First major ceiling with 0.78 net GEX (5.2% above) - options activity shows heavy interest here

- $600 - Extended upside target at 0.65 net GEX (14.8% above) - aligns with Mizuho's $600 price target

What this means for traders: SNDK is sitting right above strong $520 gamma support with $550 as the next major resistance overhead. The net GEX bias is Bullish (total call gamma of 11.2B vs put gamma of 7.5B), meaning dealer positioning generally supports the upside. However, below $485, gamma turns negative - meaning if the stock breaks that level, market makers would AMPLIFY the move lower rather than cushion it. The $475 zone is especially dangerous with heavy put gamma.

The key zone to watch: If earnings disappoint tomorrow and SNDK breaks below $500, the negative gamma zones at $475-$485 could accelerate selling. But if earnings impress, the path to $550 has relatively light resistance.

Net GEX Bias: Bullish - Overall dealer positioning supports higher prices, but the negative gamma pocket below $475 creates asymmetric downside risk.

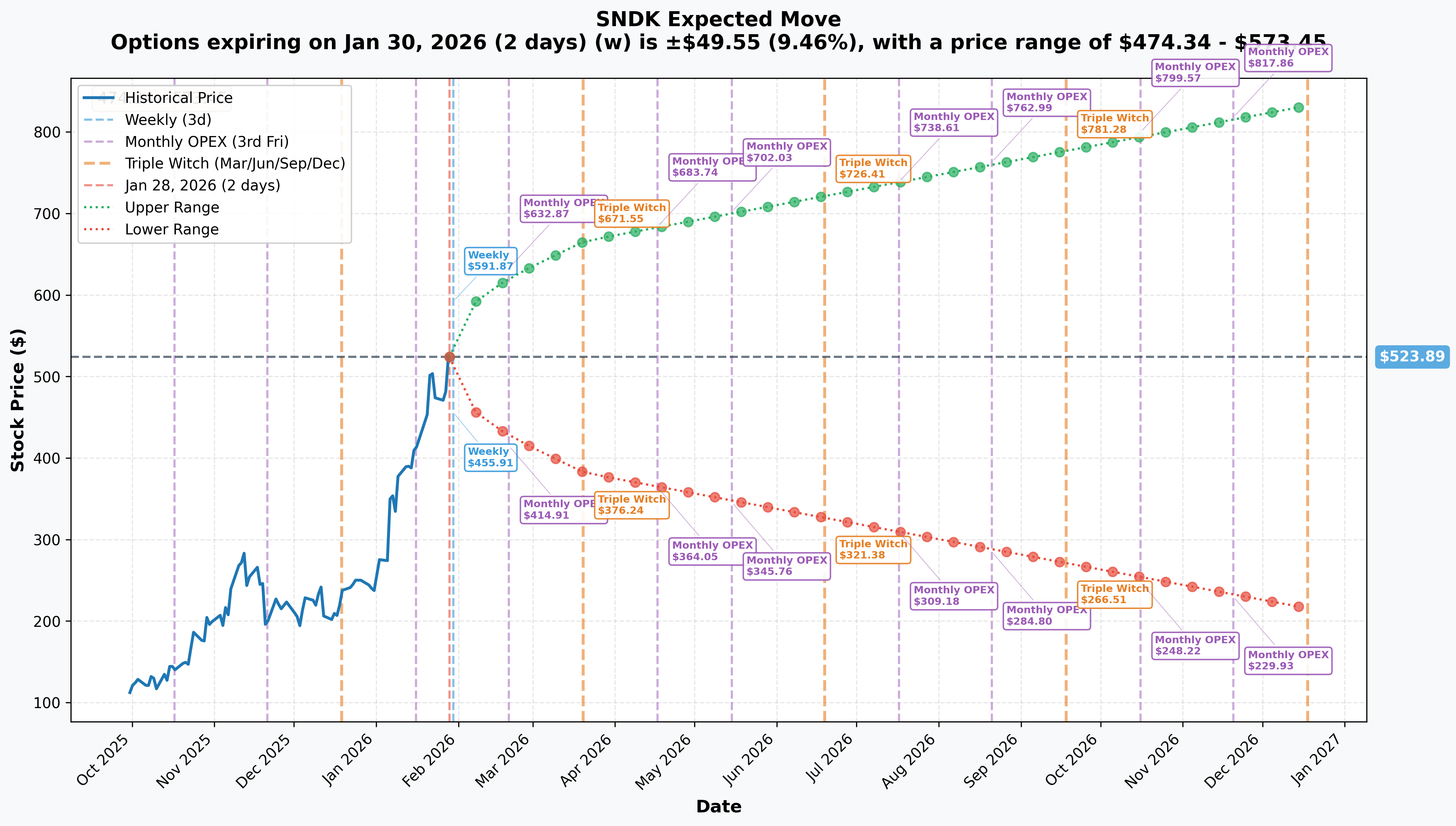

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 30 - 2 days): +/- $49.55 (+/-9.5%) -> Range: $474.34 - $573.45

- 📅 Monthly OPEX (Feb 20 - 23 days): +/- $97.92 (+/-18.7%) -> Range: $425.97 - $621.81

- 📅 Quarterly Triple Witch (Mar 20 - 51 days): +/- $142.16 (+/-27.1%) -> Range: $381.73 - $666.06

- 📅 Yearly LEAPS (Dec 18 - 324 days): +/- $308.59 (+/-58.9%) -> Range: $215.30 - $832.49

Translation for regular folks: The options market is pricing in a MASSIVE +/-9.5% move ($49.55) by THIS Friday - and that is almost entirely because of tomorrow's earnings. For a $70B company to have a nearly 10% expected weekly move is extraordinary. This is not AAPL or MSFT - this is memory semiconductor volatility on steroids.

The March 20th expiration (when the $24M trade's calls expire) has an implied range of $381.73 - $666.06 - meaning the market thinks SNDK could realistically trade anywhere in a nearly $285 range over the next 51 days. That is wild for a $70B company.

Key insight: The $24M call seller is getting out BEFORE this volatility plays out. At $473 of intrinsic value per contract, they are not waiting around to see if the stock adds another $50 or loses $100 on earnings. They are done. Profits locked.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

Q2 FY2026 Earnings - January 29, 2026 (TOMORROW!) 📊

SNDK reports fiscal Q2 results TOMORROW after market close. This is THE catalyst driving today's unusual activity. Here is what Wall Street expects:

- 📊 Revenue: $2.67-$2.68B (Company guided $2.55-$2.65B) - beating their own guidance range

- 💰 EPS: $3.10-$3.58 (Company guided $3.00-$3.40 non-GAAP)

- 📈 Gross Margin: Guided 41.0%-43.0% - historically high for memory companies

- 🤖 Key metrics to watch: Data center revenue growth, BiCS8 bit shipment percentage (was 15% in Q1), 128TB drive qualification updates, and most importantly - Q3 FY2026 guidance

Upside surprise potential: NAND contract prices surged 33-38% QoQ in Q1 2026 - if this flows through to earnings, we could see a massive beat. Bernstein named SNDK a "top pick" for 2026 citing "unprecedented NAND shortages."

Downside risk: Stock has outrun its average analyst target by ~30% ($523 vs $364 average). With 7.5% short interest (up from 4%), any disappointment could trigger a sharp pullback compounded by short covering gone wrong.

🚀 Near-Term Catalysts (Q1-Q2 2026)

NAND Flash Super-Cycle Pricing 💥

The NAND pricing environment is the best in memory industry history:

- 📈 NAND contract prices surging 33-38% QoQ across all product categories in Q1 2026

- 🏭 Global NAND inventory at historically low levels of 3-4 weeks

- 💰 Samsung weighing price hikes of 20-30% for 2026 supply deals

- 🤖 By 2026, one in five NAND bits used for AI applications, contributing up to 34% of total market value

BiCS8 & 128TB Enterprise SSD Ramp 🏭

- 📊 BiCS8 technology expected to reach majority of bit production by end of FY2026 (June 2026)

- 🎯 Two hyperscalers currently qualifying 128TB drives on BiCS8 technology

- 🚀 A third hyperscaler and a major storage OEM lined up for 2026

Kioxia/SanDisk BiCS10 Acceleration 🔬

Kioxia/SanDisk pulled forward 332-layer BiCS10 production from H2 2027 to 2026, targeting next-gen high-capacity solutions for AI and hyperscalers.

📊 Past Catalysts (Already Happened)

Q1 FY2026 Results (November 6, 2025) - CRUSHED IT:

- Revenue: $2.3B, up 21% QoQ and 23% YoY

- Non-GAAP EPS: $1.22, beating consensus of $0.77 by 58.4%

- Stock surged 27.2% in two trading sessions following the report

Kitakami K2 Fab Operations (September 30, 2025):

- Kioxia and SanDisk started operations at Fab2 (K2) producing 218-layer 3D flash memory

Analyst Price Target Upgrades:

| Firm | Price Target | Rating |

|---|---|---|

| Mizuho | $600 | Outperform |

| Bernstein | $580 | Outperform |

| Morgan Stanley | $483 | -- |

| RBC Capital | $400 | Sector Perform |

| Bank of America | $390 | Buy |

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and tomorrow's earnings catalyst, here are the scenarios through the March 20th expiration:

📈 Bull Case (30% probability)

Target: $575-$625

How we get there:

- 💪 Tomorrow's earnings CRUSH expectations - revenue $2.7B+ with gross margins above 43% guidance

- 🚀 Q3 FY2026 guidance surprises to the upside, validating the NAND super-cycle thesis

- 📈 128TB enterprise SSD qualifications announced with additional hyperscalers

- 🤖 Data center revenue growth accelerates beyond 26% sequential

- 📊 Break above $550 gamma resistance triggers technical rally toward $600 (Mizuho's target)

- 💰 Short squeeze dynamics (7.5% short interest) amplify the move higher

Key metrics needed:

- Revenue beat above $2.7B (guided $2.55-$2.65B)

- Gross margins at or above 43% (top of guided range)

- Q3 guidance showing continued acceleration

- BiCS8 approaching 25%+ of bit shipments

Why 30%: Requires a strong beat AND upside guidance in a stock that has already rallied 105% YTD. The implied move upper range for weekly ($573) and the $550 gamma resistance both suggest $575 as an achievable near-term ceiling. Getting to $600+ requires sustained momentum.

🎯 Base Case (45% probability)

Target: $480-$550 range (POST-EARNINGS CONSOLIDATION)

Most likely scenario:

- ✅ Solid earnings meeting or slightly beating consensus (~$2.65-2.70B revenue, $3.20-3.50 EPS)

- 📊 Guidance in-line with expectations - good enough to hold current levels but not explosive

- ⚖️ Stock initially volatile on earnings, then settles into consolidation between gamma support ($500-$520) and resistance ($550)

- 🔄 Volatility crush post-earnings reduces option premiums significantly

- 📈 Market digests the 1,000%+ rally and waits for next catalyst (BiCS10, new qualifications)

- 💤 Short interest provides floor but ceiling exists at analyst targets

This is what the $24M call seller is positioning for: They have already captured the bulk of the move. Whether SNDK trades at $500 or $550 over the next 51 days, they are done collecting profits. The risk/reward of holding deep ITM calls through a binary earnings event simply does not make sense when you are already sitting on enormous gains.

Why 45%: SNDK has strong fundamentals but is priced for perfection. Most likely outcome is a "good but not great" earnings print that keeps the stock in a trading range while the market reassesses the next leg of growth.

📉 Bear Case (25% probability)

Target: $400-$475

What could go wrong:

- 😰 Earnings miss or Q3 guidance disappoints - even a small miss at 21x+ P/E could trigger -15-20% correction

- 🚨 NAND pricing cycle shows signs of peaking - Samsung's 50% capacity expansion threatens supply-demand balance

- 📊 BiCS8 ramp slower than expected, 128TB qualification delays

- 💸 Short interest at 7.5% creates selling pressure if momentum breaks

- 🇨🇳 New "Annual Approval System" for NAND exports to China (effective January 2026) impacts revenue outlook

- 📉 Break below $500 gamma support triggers cascade through negative gamma zones at $475-$485

- 🔨 Institutional profit-taking accelerates (today's $24M sale could be the tip of the iceberg)

Critical support levels:

- 🛡️ $520: Immediate gamma floor - must hold or momentum shifts bearish

- 🛡️ $500: Major structural support (round number + strong gamma) - THE line in the sand

- 🛡️ $475: Negative gamma zone - break below here accelerates selling

- 🛡️ $450: Deep support - a 14% drawdown aligns with monthly OPEX lower range ($426)

Why 25%: The NAND super-cycle fundamentals are strong, but memory stocks are cyclical beasts. At 21x+ forward P/E (vs Micron and SK Hynix under 10x), SNDK has zero margin for error. One bad earnings print or cycle-turn signal could trigger rapid multiple compression.

💡 Trading Ideas

🛡️ Conservative: Wait for the Dust to Settle

Play: Stay on sidelines until after tomorrow's earnings volatility clears

Why this works:

- ⏰ Earnings TOMORROW creates massive binary event risk - implied move is +/-9.5% ($49.55)

- 💸 Options are EXTREMELY expensive right now (implied vol elevated pre-earnings)

- 📊 Stock at all-time highs after 1,000%+ rally with 21x+ forward P/E - zero margin of safety

- 🎯 Better entry likely post-earnings whether stock gaps up (buy dips from profit-taking) or gaps down (buy the pullback)

- 🤔 The $24M institutional call exit signals smart money is reducing exposure - why fight the tape?

Action plan:

- 👀 Watch tomorrow's earnings closely for revenue ($2.68B target), margins (43%+ needed), and Q3 guidance

- 🎯 Look for pullback to $480-500 gamma support zone for stock entry with 5-10% margin of safety

- ✅ Need to see Q3 guidance acceleration before committing new capital

- ⏰ Revisit in 1-2 weeks once post-earnings volatility settles and new positioning emerges

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After earnings, sell a bull put spread to collect premium while defining your risk

Structure: Sell $500 put / Buy $480 put (February 20 expiration - 23 days)

Why this works:

- 🎢 IV crush after earnings makes selling premium much more attractive

- 📊 $500 is major gamma support - dealers will buy dips aggressively at this level

- 🎯 Defined risk spread ($20 wide = $2,000 max risk per spread)

- 💰 Collect premium while the NAND super-cycle fundamentals remain intact

- ⏰ February OPEX gives 23 days of time decay working in your favor

- 🛡️ Only enter AFTER seeing earnings results - do not sell premium into a binary event blind

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$5-7 net credit per spread (depending on post-earnings IV)

- 📈 Max profit: Full credit received if SNDK stays above $500 at February OPEX

- 📉 Max loss: $13-15 per spread if SNDK below $480

- 🎯 Breakeven: ~$493-495

Entry timing:

- ⏰ Wait until January 30 (day after earnings) for IV to collapse

- 🎯 Only enter if stock holds above $500 and earnings were solid

- ❌ Skip if stock gaps below $490 (spread too close to the money)

Risk level: Moderate (defined risk, neutral-to-bullish) | Skill level: Intermediate

🚀 Aggressive: Post-Earnings Call Spread Targeting $600

Play: Buy a call spread betting SNDK continues its run after a strong earnings print

Structure: Buy $550 call / Sell $600 call (March 20 expiration - 51 days)

Why this could work:

- 💥 If earnings crush expectations (revenue $2.7B+, margins 43%+), momentum could carry SNDK toward Mizuho's $600 target

- 📊 $550 is the next major gamma resistance - a breakout above it opens the path to $600

- 🚀 Short squeeze dynamics (7.5% short interest) could amplify post-earnings rally

- 🤖 NAND pricing surging 33-38% QoQ provides fundamental tailwind

- 📈 $50-wide spread caps risk while offering 5:1+ potential reward

- ⏰ 51 days to expiration gives time for the thesis to play out

Estimated P&L:

- 💰 Cost: ~$10-15 per spread (after post-earnings IV adjustment)

- 📈 Max profit: $35-40 per spread if SNDK above $600 at March OPEX

- 📉 Max loss: $10-15 per spread (entire premium paid)

- 🎯 Breakeven: ~$560-565

CRITICAL WARNING:

- ✅ Only enter AFTER earnings if results are strong and stock holds above $520

- ⚠️ If earnings disappoint, DO NOT chase - the move lower will be equally violent

- 📊 This is a directional bet requiring SNDK to rally another 5-15% from current all-time highs

- 💸 You could lose the entire premium - size accordingly (2-5% of portfolio max)

Risk level: HIGH (directional, can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Do not get caught by these potential landmines:

-

⏰ Earnings binary event TOMORROW: Results January 29 after close create MASSIVE volatility risk. Options market pricing +/-9.5% move ($49.55) for the week - that is a potential $50 swing in either direction for a $523 stock. Consensus expects $2.68B revenue and $3.31-3.58 EPS, but any miss on gross margins or Q3 guidance could trigger a 10-15% gap down given stretched valuation.

-

💸 Valuation at nosebleed levels: Trading at 21x+ forward P/E vs Micron and SK Hynix both under 10x. Stock has outrun the average analyst price target by ~30% ($523 vs $364 average). After a 1,000%+ rally, SNDK is priced for PERFECT execution. Zero margin of safety.

-

🔄 Memory market cyclicality: Memory markets are inherently cyclical. Samsung planning 50% production capacity expansion, SK Hynix ramping 321-layer QLC, and Micron investing $125B in U.S. megafabs. All this new supply could flip the supply-demand balance in late 2026 or 2027, compressing margins and earnings.

-

📉 Short interest rising despite losses: Short interest has climbed from 4% to 7.5% of float even though shorts have lost $3B. This signals bears are getting MORE convicted, not less. Creates extreme two-way volatility risk around earnings.

-

🇨🇳 China export restrictions: New "Annual Approval System" for NAND exports to China effective January 2026 increases compliance burden. Further U.S.-China chip war escalation could restrict access to Chinese consumer electronics market.

-

🏭 Execution risk on technology transitions: BiCS8 and BiCS10 technology transitions carry execution risk. Kitakami K2 fab ramp must proceed on schedule. Still early as an independent company (less than 1 year public) with limited standalone operating history.

-

🐋 Institutional profit-taking underway: Today's $24M deep ITM call exit is the kind of trade that signals sophisticated players are REDUCING exposure. When funds who rode a 1,000%+ rally start cashing out before earnings, retail traders should pay close attention. Major institutions like UBS (-81%), Citadel (-85%), and FIL (-99.8%) have already been reducing positions.

-

📊 Negative gamma pocket creates downside acceleration risk: Below $485, gamma turns negative, meaning market makers would AMPLIFY selling rather than cushion it. A break below $500 support into this negative gamma zone could trigger a cascade to $475 or lower before finding a floor.

-

🤖 AI demand normalization risk: If AI infrastructure spending moderates or shifts away from NAND-intensive architectures, the entire thesis unwinds. Consumer NAND demand (eMMC/UFS) is already weakening as the smartphone market enters inventory adjustment.

🎯 The Bottom Line

Real talk: Someone just cashed out $24 MILLION in deep in-the-money SNDK calls the day before earnings. This is not a bearish signal - it is a profit-taking signal. They rode the $50 calls from the early post-spinoff days all the way to $523, collected a massive payout, and are now free to watch tomorrow's earnings from the sidelines with their profits locked in.

What this trade tells us:

- 🎯 Sophisticated player had deep conviction on SNDK early (buying $50 calls when few believed)

- 💰 They made an extraordinary return and are now harvesting profits responsibly

- ⏰ The pre-earnings timing is deliberate - why risk a binary event when you have already won?

- 📊 The MID execution (between bid and ask) suggests orderly exit, not panic selling

- ⚖️ Volume of 499 vs OI of 670 means a significant portion of open interest was closed today

This is a "take the money and run" signal, NOT a "the sky is falling" signal.

If you own SNDK:

- ✅ Consider trimming 25-40% ahead of earnings to lock in gains - you have had an incredible run

- 📊 If holding through earnings, know that $520 is immediate gamma support and $500 is the major floor

- ⏰ Set mental stops - a break below $500 post-earnings would be a warning sign for bigger pullback

- 🎯 If earnings beat AND stock breaks $550, you can re-enter trimmed shares on momentum toward $600

If you are watching from sidelines:

- ⏰ January 29 after close is the moment of truth - DO NOT enter before earnings!

- 🎯 Post-earnings pullback to $480-500 would be an excellent entry with gamma support underneath

- 📈 Looking for: Revenue beat above $2.68B, gross margins 43%+, Q3 guidance acceleration

- 🚀 Longer-term, the NAND super-cycle, BiCS10 acceleration, and potential Kioxia merger optionality are legitimate catalysts for $600+

If you are bearish:

- 🎯 Wait for earnings before initiating shorts - fighting 1,000% momentum into all-time highs is dangerous

- 📊 First support at $520 (gamma), major support at $500, negative gamma acceleration below $485

- ⚠️ Post-earnings put spreads ($500/$480) offer defined-risk downside exposure after IV crush

- 📉 Watch for break below $500 - that is the trigger for cascade into negative gamma territory

Mark your calendar - Key dates:

- 📅 January 29 (Thursday) after close - Q2 FY2026 earnings report (TOMORROW!)

- 📅 January 30 - Post-earnings price action and analyst reactions (weekly OPEX)

- 📅 February 20 - Monthly OPEX (implied range: $426-$622)

- 📅 March 20 - Triple Witch / this call trade's expiration (implied range: $382-$666)

- 📅 Late April/Early May 2026 - Q3 FY2026 earnings expected

- 📅 H1 2026 - BiCS8 majority production milestone and K2 fab ramp

- 📅 H2 2026 - BiCS10 332-layer production begins

Final verdict: SNDK's AI storage story is powerful - NAND prices surging 33-38%, hyperscaler qualifications ramping, and the technology roadmap accelerating. But at $523 after a 1,000%+ rally with earnings TOMORROW and the stock 30% above its average analyst target, this is not the time for aggressive new positioning. The $24M institutional call exit is a CLEAR signal: smart money is taking profits at the top.

Be patient. Let earnings clear. The NAND super-cycle will still be here next week, and you will sleep better buying at $490 than $523 if the opportunity presents itself.

This is a marathon, not a sprint. Protect your capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The Z-score of 6.11 reflects this trade's unusual size relative to recent SNDK history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 10%+ gaps in either direction. Deep ITM call sales represent position management, not directional views.

About SanDisk Corporation: SanDisk is among the world's top five NAND flash memory semiconductor suppliers. The firm manufactures most of its flash chips through a Japanese joint venture with Kioxia, then converts them into SSDs for consumer and enterprise applications. Spun off from Western Digital in February 2025, with a market cap of $70.6 billion in the Computer Storage Devices industry.