Ainvest Option Flow Digest - 2026-02-03 - $74M Institutional Positioning as Earnings Gauntlet Begins

WHALE ALERT: $74M+ in Unusual Options Activity Hits 8 Tickers

Executive Summary

Today we tracked $73.8 MILLION in institutional options activity across 8 tickers - from mega-cap ETFs to AI infrastructure plays. The dominant theme? Risk management ahead of mega-cap earnings and peak cycle hedging.

The Headline Trades:

- MU: $26M LEAP call spread roll - peak memory cycle positioning

- PYPL: $14.4M put activity as stock crashes 20% on CEO exit

- QQQ: $7.9M put spread roll before AMD/Google/Amazon earnings

- XLB: $6.3M put protection roll on materials sector

- SLV: $6.5M call selling after silver's historic 40% crash

- DIA: $5.5M September put bet on midterm year weakness

- TSLA: $4.5M short call cover before FSD deadline

- VRT: $3.2M LEAP call on AI data center infrastructure

The Message: Institutions are hedging, not panicking. They're staying invested but wearing seatbelts through the earnings gauntlet and macro uncertainty ahead.

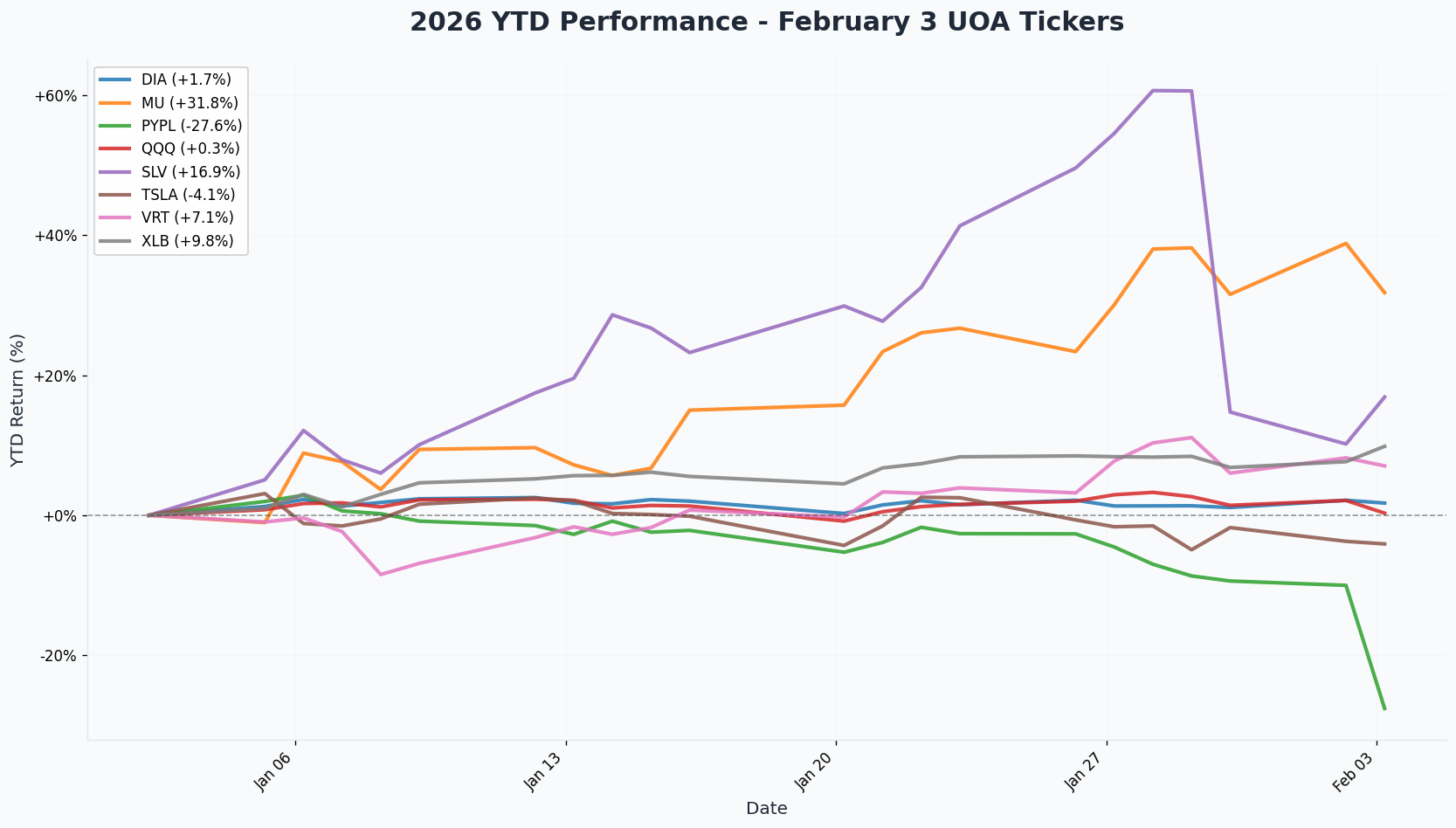

2026 YTD Performance

Complete Flow Summary

| Ticker | Premium | Direction | Expiration Range | Key Catalyst | Option Play | The Big Picture |

|---|---|---|---|---|---|---|

| MU | $26M | SELL Calls | Jan 2027 | Q2 Earnings Mar 26 | LEAP Roll | Peak memory cycle - seller caps upside at $550 |

| PYPL | $14.4M | Mixed PUT | Feb-Dec 2026 | New CEO Mar 1 | Hedge + New Bets | CEO fired, 20% crash - bears loading up |

| QQQ | $7.9M | PUT Roll | Feb 2026 | AMD/GOOG/AMZN This Week | Hedge Adjustment | Portfolio insurance repositioned lower |

| XLB | $6.3M | PUT Roll | Mar 2026 | Construction Data Feb 27 | Roll UP | Materials sector fear - hedge closer to price |

| SLV | $6.5M | SELL Calls | Aug 2026 | Fed Transition | Premium Harvest | Betting silver stalls below $90 after crash |

| DIA | $5.5M | BUY PUT | Sep 2026 | Midterm Seasonality | Outright Bet | Positioning for -18% average midterm drawdown |

| TSLA | $4.5M | BUY Calls | Feb 2026 | FSD Deadline Feb 14 | Short Cover | De-risking before binary catalyst |

| VRT | $3.2M | BUY Calls | Jan 2027 | S&P 500 Inclusion Q1 | LEAP Bet | AI infrastructure supercycle conviction |

Individual Ticker Breakdowns

1. MU - $26M LEAP Call Spread Roll Signals Peak Cycle Positioning

SEE WHY SOMEONE IS CAPPING THEIR UPSIDE AT $550

- Flow: $26M collected selling $550 and closing $650 Jan 2027 calls

- Z-Score: 6.37x (EXTREMELY UNUSUAL)

- YTD Performance: +20%

- The Big Question: Has the memory supercycle peaked after MU's 247% rally?

- Catalyst: Q2 FY2026 Earnings (Late March) - $18.7B revenue guidance

2. PYPL - $14.4M Put Activity as Stock Crashes 20%

DECODE THE THREE-WAY PUT FLOW ON THIS COLLAPSE

- Flow: $14.4M across profit-taking, hedge closes, and NEW bearish bets

- Z-Score: 300.53x (December $40 put - HISTORIC)

- YTD Performance: -20% (today alone!)

- The Big Question: Is this capitulation or the start of something worse?

- Catalyst: New CEO Enrique Lores starts March 1

3. QQQ - $7.9M Put Spread Roll Before Earnings Gauntlet

UNDERSTAND THE INSTITUTIONAL HEDGE REPOSITIONING

- Flow: $3.9M net debit rolling puts from $600 down to $570

- Z-Score: 13.92x (EXTREMELY UNUSUAL)

- YTD Performance: +2.1%

- The Big Question: Why roll protection lower right before AMD, Google, and Amazon report?

- Catalyst: AMD (Tonight), Google (Tomorrow), Amazon (Thursday)

4. XLB - $6.3M Put Protection Roll Signals Materials Fear

ANALYZE WHY THEY PAID $1.7M TO MOVE HEDGE CLOSER

- Flow: $1.7M net debit rolling puts UP from $46 to $48.5

- Z-Score: 23.35x (23 TIMES NORMAL!)

- YTD Performance: +8.64%

- The Big Question: Why pay MORE for LESS downside protection at 52-week highs?

- Catalyst: Delayed Construction Spending Data (February 27)

5. SLV - $6.5M Premium Seller Bets Silver Stalls Below $90

LEARN WHY THEY'RE HARVESTING PREMIUM AT 97TH PERCENTILE IV

- Flow: $6.5M collected selling August $90 calls

- Z-Score: 21.2x (EXTREMELY UNUSUAL)

- YTD Performance: +58% (but -40% from highs after crash)

- The Big Question: Is the silver rally truly over after the Warsh-triggered 40% crash?

- Catalyst: Warsh Fed Confirmation Hearings

6. DIA - $5.5M September Put Bet on Midterm Meltdown

DISCOVER THE MIDTERM YEAR SEASONALITY THESIS

- Flow: $5.5M on September $480 puts (2.1% OTM)

- Z-Score: LOW (but Vol/OI ratio 1500x = HIGH ACTIVITY)

- YTD Performance: +10.39%

- The Big Question: Will the average -18% midterm year drawdown materialize in 2026?

- Catalyst: Fed Leadership Transition (May), September Seasonal Weakness

7. TSLA - $4.5M Short Call Cover Before FSD Deadline

SEE WHY INSTITUTIONS ARE DE-RISKING HERE

- Flow: $4.5M buying back short $440/$450 calls (closing positions)

- Z-Score: 3.91x (EXTREMELY UNUSUAL)

- YTD Performance: +9.1%

- The Big Question: What happens when the FSD one-time purchase deadline hits February 14?

- Catalyst: FSD Deadline (Feb 14), Optimus V3 Reveal (Q1)

8. VRT - $3.2M LEAP Bet on AI Data Center Gold Rush

UNPACK THE YEAR-LONG AI INFRASTRUCTURE BET

- Flow: $3.2M on January 2027 $230 calls

- Z-Score: 4.46x (EXTREMELY UNUSUAL)

- YTD Performance: +61%

- The Big Question: Can the "picks and shovels" AI play keep running at 60x P/E?

- Catalyst: Q4 Earnings (Feb 11), S&P 500 Inclusion Expected Q1

Trading Ideas By Investor Type

YOLO Plays (1-2% Portfolio Max)

- PYPL $40/$35 Put Spread (April) - Join the $1.8M bear betting on more downside

- VRT March $190 Straddle - Capture the 12% implied move around earnings

Swing Trades (3-5% Portfolio)

- QQQ Feb $600/$570 Put Spread - Mirror the institutional hedge at lower cost

- XLB Mar $48.5/$46 Put Spread - Follow the whale's exact strikes

Premium Collection Strategies

- SLV Aug $90 Covered Call - Harvest 97th percentile IV like the $6.5M seller

- MU Feb $450 Covered Call - Mimic institutional positioning at elevated IV

- TSLA $400 Cash-Secured Put - Collect premium at major gamma support

Entry Level / Conservative

- DIA Mar $480 Put - Portfolio protection through Triple Witch

- VRT Shares with 10% Trailing Stop - Ride the AI infrastructure theme

Catalyst Calendar

This Week (Feb 3-7)

| Date | Ticker | Event | Impact |

|---|---|---|---|

| Feb 3 (Tonight) | QQQ | AMD Q4 Earnings | HIGH |

| Feb 4 | QQQ | Google Q4 Earnings | HIGH |

| Feb 5 | QQQ | Amazon Q4 Earnings | HIGH |

| Feb 6 | DIA | January Employment Report | MEDIUM |

Next 2 Weeks (Feb 10-21)

| Date | Ticker | Event | Impact |

|---|---|---|---|

| Feb 11 | VRT | Q4 & FY2025 Earnings (Pre-Market) | HIGH |

| Feb 11 | All | January CPI Release | HIGH |

| Feb 14 | TSLA | FSD One-Time Purchase Deadline | HIGH |

| Feb 20 | QQQ | Monthly OPEX | MEDIUM |

Upcoming (Feb-Sep 2026)

| Date | Ticker | Event | Impact |

|---|---|---|---|

| Feb 27 | XLB | Delayed Construction Spending Data | HIGH |

| Mar 1 | PYPL | New CEO Enrique Lores Starts | HIGH |

| Late Mar | MU | Q2 FY2026 Earnings | HIGH |

| Q1 2026 | VRT | S&P 500 Index Inclusion (Expected) | HIGH |

| Apr 28 | PYPL | Q1 2026 Earnings | MEDIUM |

| May 15 | SLV | Powell's Fed Term Expires | HIGH |

| Sep 18 | DIA | September Put Expiration | HIGH |

Option Expirations in Focus

| Timeframe | Tickers | Key Levels |

|---|---|---|

| Feb 6 | PYPL | $49 put strike |

| Feb 13 | TSLA | $440/$450 call strikes |

| Feb 20 | QQQ | $600/$570 put strikes |

| Mar 20 | XLB | $48.5/$46 put strikes |

| Aug 21 | SLV | $90 call strike |

| Sep 18 | DIA | $480 put strike |

| Jan 2027 | MU, VRT | $550 call (MU), $230 call (VRT) |

Risk Management Notes

Key Themes to Watch:

-

Earnings Concentration Risk: AMD, Google, and Amazon all report in 72 hours - the $7.9M QQQ put roll shows institutions are hedged

-

Fed Transition Uncertainty: Warsh nomination triggered silver's 40% crash; his confirmation hearings will move markets

-

Peak Cycle Positioning: The $26M MU trade and $6.5M SLV call selling suggest big money believes certain rallies are exhausted

-

Midterm Year Seasonality: The $5.5M DIA put is a direct bet on the historical -18% average intra-year drawdown

-

Single-Stock Event Risk: PYPL's 20% crash shows how quickly positions can unwind; always size appropriately

Quick Links

Today's Analyses:

- MU: $26M LEAP Call Spread Roll

- PYPL: $14.4M Put Activity

- QQQ: $7.9M Put Spread Roll

- XLB: $6.3M Put Spread Roll

- SLV: $6.5M Premium Seller

- DIA: $5.5M September Put

- TSLA: $4.5M Short Call Cover

- VRT: $3.2M LEAP Bet

The Bottom Line

$74 million speaks volumes. Today's institutional flow paints a clear picture: smart money is staying invested but managing risk through one of the most catalyst-dense weeks of the year.

The key takeaways:

-

Peak Cycle Awareness: MU's $26M roll and SLV's $6.5M call selling show institutions believe certain rallies have run their course

-

Earnings Insurance: The QQQ and DIA put activity demonstrates professional hedging ahead of mega-cap reports

-

Single-Stock Catastrophe Warning: PYPL's 20% crash and the $14.4M put flow remind us why position sizing matters

-

Long-Term Conviction Still Exists: VRT's $3.2M LEAP bet shows big money hasn't abandoned the AI infrastructure thesis

Mark Your Calendar:

- Tonight: AMD earnings

- Tomorrow: Google earnings

- Thursday: Amazon earnings

- February 11: VRT earnings + CPI

- February 14: TSLA FSD deadline

The institutions aren't running - they're repositioning. Follow the flow.

Disclaimer: This newsletter is for informational purposes only and does not constitute investment advice. Options trading involves significant risk of loss. Past unusual activity does not guarantee future results. Always conduct your own research and consider your risk tolerance before trading.

Data sources: Proprietary tape analysis, Polygon.io, Company filings, ThetaData