Ainvest Option Flow Digest - 2025-12-04: Gold, China & M&A Mega-Bets - $73.8M Institutional Wave Targets Year-End Catalysts

December 4, 2025 | MASSIVE FLOW: GLD's $38M Bull Spread on Fed Pivot + CRM's Historic $13M Agentforce Bet + WBD's $5.2M M&A Speculation | Gold, AI Enterprise, China Tech & Corporate Events Dominate

The $73.8M Institutional Tsunami: Smart Money Positioning for Q1 2026

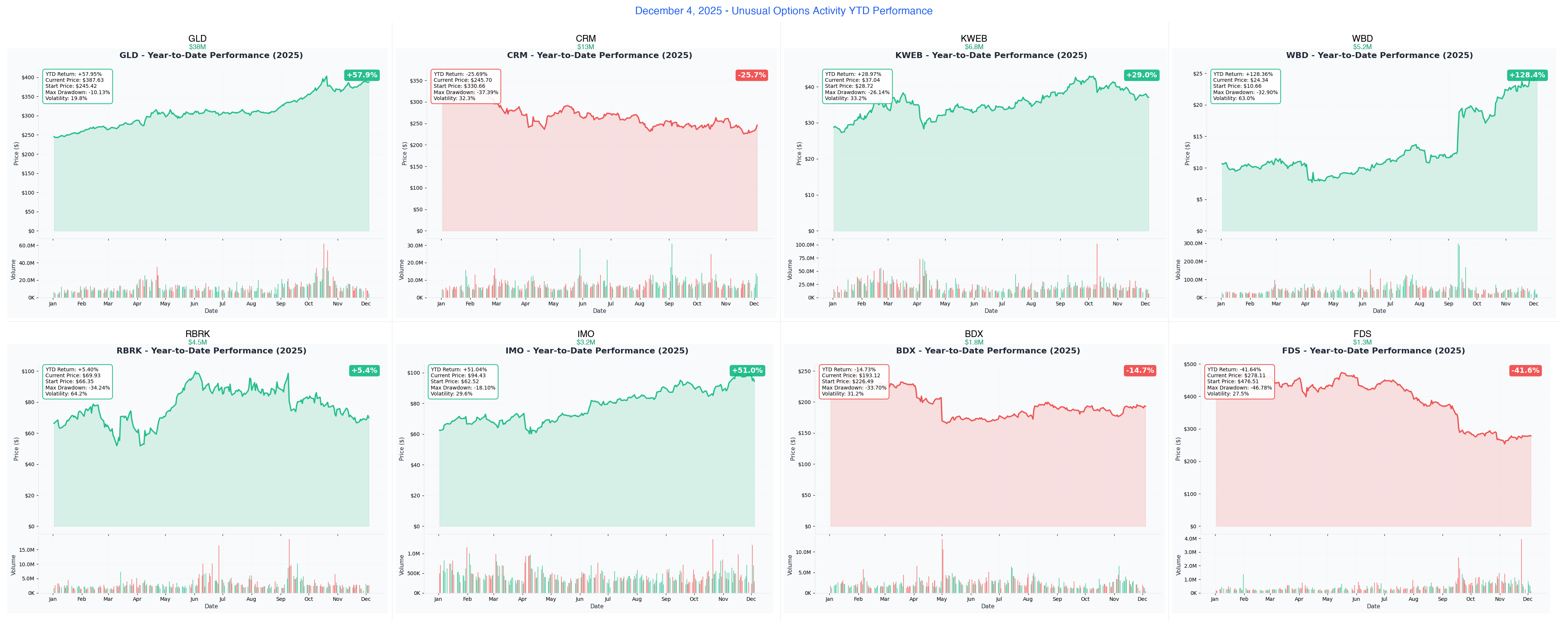

DIVERSIFIED CONVICTION: We tracked $73.8 MILLION in institutional options activity across 8 names today - led by GLD's massive $38M bull call spread betting on gold's Fed-driven breakout, CRM's unprecedented $13M call buy (largest in company history) targeting Agentforce AI scaling, and KWEB's $6.8M China recovery spread. The unified theme: institutions positioning for January FOMC, Q4 earnings surprises, and corporate M&A events before year-end.

Total Flow Tracked: $73,800,000 Largest Single Trade: GLD $38M bull call spread (3.5:1 risk/reward on gold breakout) Historic Trade: CRM $13M call buy (2,130x average size - UNPRECEDENTED) Defensive Positioning: IMO $3.24M put protection + RBRK $4.5M call selling M&A Speculation: WBD $5.2M + BDX $1.8M = $7M in event-driven plays

Complete Flow Summary Table

| Ticker | Premium | Expiration | Category | Strategy | Catalyst | Play Type |

|---|---|---|---|---|---|---|

| GLD | $38M | Jan 16, 2026 | Monthly | Bull Call Spread ($400/$415) | Fed rate cuts + central bank buying ahead of Jan FOMC | Directional Bullish |

| CRM | $13M | Mar 20, 2026 | Quarterly | Call Buy ($270) | Agentforce AI scaling ahead of Feb 26 earnings | Directional Bullish |

| KWEB | $6.8M | Mar 20, 2026 | Quarterly | Bull Call Spread ($39/$44) | China NPC policy + Q4 earnings wave | Directional Bullish |

| WBD | $5.2M | Mar 20, 2026 | Quarterly | Call Buy ($25) | M&A bidding war (Comcast/Netflix/Paramount) | Event-Driven |

| RBRK | $4.5M | Jan 16, 2026 | Monthly | Call Sell ($85) | Income play during low-catalyst consolidation | Income/Neutral |

| IMO | $3.24M | Jan 16, 2026 | Monthly | Put Buy ($95) | Oil price protection as WTI sinks to $59 | Hedging |

| BDX | $1.8M | Mar 20, 2026 | Quarterly | Call Buy ($220) | Waters Corp merger + $17.5B spin-off | Event-Driven |

| FDS | $1.3M | Dec 19, 2025 | Weekly | Call Buy ($290) | Dec 18 earnings - gamma squeeze setup | Directional Bullish |

The Complete Whale Lineup

1. GLD - $38M Bull Call Spread: Betting on Gold's Fed-Driven Breakout

DISCOVER WHY SOMEONE BET $38M ON GOLD BREAKING $400

- Flow: $38M net debit on $400/$415 bull call spread (113,670 contracts each leg)

- What's Happening: Gold at $387, just 3% from all-time highs as central banks bought 1,045 tonnes in 2024

- The Big Question: Will January FOMC pivot talk push GLD through $400 psychological resistance?

- Why It's Genius: Paid $38M for a structure that returns $132M at $415 (348% ROI) - expires 12 days BEFORE the critical Jan 28-29 FOMC

2. CRM - $13M Historic Call Bet: Largest Salesforce Trade EVER

SEE WHY SOMEONE MADE THE BIGGEST CRM BET IN HISTORY

- Flow: $13M on $270 March calls (14,000 contracts - 2,130x average size)

- What's Happening: Agentforce AI platform scaling from 200 Q3 deals toward 600-1,000+ enterprise deployments

- The Big Question: Can Salesforce prove AI agents are the next $10B+ revenue stream by Feb 26 earnings?

- Why It's Historic: 2,130x average trade size - this happens maybe once per year on CRM

3. KWEB - $6.8M Bull Call Spread: Sophisticated China Recovery Play

ANALYZE THE $6.8M BET ON CHINA TECH'S NEXT LEG HIGHER

- Flow: $6.8M net debit on $39/$44 spread (71,000 contracts each leg)

- What's Happening: KWEB up 38% YTD but smart money says there's more runway before March

- The Big Question: Will China's National People's Congress stimulus announcements extend the rally?

- Sophistication: Structured around gamma dynamics - $39 strike at resistance, $44 at implied move cap

4. WBD - $5.2M M&A Speculation: Betting on Bidding War

DISCOVER THE $5.2M BET ON WARNER BROS' CORPORATE DESTINY

- Flow: $5.2M on $25 March calls (40,000 contracts at ASK - brand new position)

- What's Happening: Three competing bidders (Comcast, Netflix, Paramount) battling for WBD assets

- The Big Question: Will Christmas M&A decision drive WBD above $25 resistance?

- Gamma Angle: Struck at $25 where there's 105.2M net gamma - positioning for squeeze

5. RBRK - $4.5M Call Selling: Smart Money Capping Upside

UNDERSTAND WHY INSTITUTIONS ARE SELLING RBRK CALLS

- Flow: $4.5M collected selling $85 January calls (26,000 contracts sold)

- What's Happening: Stock up 94% from $32 IPO but down 32% from October highs - consolidation zone

- The Big Question: Is the cyber resilience rally exhausted until March earnings?

- Income Logic: Collecting 2.5% premium in 43 days betting stock stays below $85

6. IMO - $3.24M Put Protection: Hedging Oil Collapse

SEE WHY INSTITUTIONS ARE HEDGING IMO DESPITE ALL-TIME HIGHS

- Flow: $3.24M on $95 January puts (13,100 contracts across two desperate trades)

- What's Happening: WTI crude at $59 (down 15.7% YTD) while IMO trades near 52-week highs

- The Big Question: Can IMO sustain premium valuations as WCS differentials widen to $13?

- Red Flag: Two trades at SAME strike, DIFFERENT premiums - fear-based hedging, not routine insurance

7. BDX - $1.8M Call Buy: Betting on Merger Value Unlock

DISCOVER THE $1.8M BET ON BDX'S TRANSFORMATION

- Flow: $1.8M on $220 March calls (10,000 contracts - 808x average size)

- What's Happening: Waters Corp merger completing Q1 2026, unlocking $15-20B from Biosciences spin-off

- The Big Question: Will management's worst execution phase finally be over?

- Contrarian Angle: Buying at 52-week lows (stock down 19.8% YTD) for 13.6% upside

8. FDS - $1.3M Earnings Gamma Play: 15-Day Binary Bet

DECODE THE $1.3M FDS EARNINGS GAMBLE

- Flow: $1.3M on $290 December 19 calls (1,500 contracts - expires ONE DAY after earnings)

- What's Happening: December 18 earnings for financial data giant down 44% from highs

- The Big Question: Can new CEO deliver surprise that triggers gamma squeeze at $290 max gamma?

- High Risk: Zero margin for error - needs 7-8% immediate gap-up on December 18

Upcoming Catalysts - Clearly Separated

Option Expiration Schedule:

| Date | Ticker | Expiration Event |

|---|---|---|

| Dec 19, 2025 | FDS | Weekly calls expire (15 DTE) |

| Jan 16, 2026 | GLD, IMO, RBRK | Monthly options expire (43 DTE) |

| Mar 20, 2026 | CRM, KWEB, WBD, BDX | Quarterly options expire (106 DTE) |

Catalyst Calendar (Separate from Expirations):

| Date | Ticker | Catalyst Event |

|---|---|---|

| Dec 18, 2025 | FDS | Q1 FY2026 Earnings |

| Late Dec 2025 | WBD | M&A Decision Expected (Comcast/Netflix/Paramount) |

| Jan 28-29, 2026 | GLD | January FOMC Meeting |

| Jan 30, 2026 | IMO | Q4 Earnings |

| Feb 26, 2026 | CRM | Q4 FY2025 Earnings |

| Mar 5, 2026 | KWEB | China National People's Congress |

| Mar 13, 2026 | RBRK | Q4 Earnings |

| Q1 2026 | BDX | Waters Corp Merger Completion |

Smart Money Themes: What Institutions Are Really Betting

Gold & Macro (52% of Today's Flow: $38M)

Fed Pivot Play:

- GLD $38M bull spread - Central banks bought 1,045 tonnes in 2024, betting Fed cuts drive breakout

AI Enterprise (18% of Flow: $13M)

Agentforce Validation:

- CRM $13M call buy - Largest CRM trade ever, betting AI agents scale 5x by Q4 earnings

China Recovery (9% of Flow: $6.8M)

Policy Stimulus:

- KWEB $6.8M spread - Sophisticated spread structure targeting NPC policy catalyst

Event-Driven M&A (10% of Flow: $7M)

Corporate Actions:

- WBD $5.2M calls - Three bidders, Christmas decision expected

- BDX $1.8M calls - Merger unlock at 52-week lows

Defensive & Income (10% of Flow: $7.74M)

Hedging & Premium Collection:

- IMO $3.24M puts - Oil price collapse protection

- RBRK $4.5M call selling - Income during consolidation

Your Action Plan By Investor Type

YOLO Trader (1-2% Portfolio MAX)

EXTREME RISK - Binary events with asymmetric payoff

Top YOLO Plays:

- FDS $290 December calls - Earnings in 14 days, expires 1 day after. Win big or lose 100%.

- WBD $25 calls - M&A decision could drop any day before Christmas. Gamma squeeze potential if bidding war heats up.

Why these work: Binary M&A/earnings outcomes. FDS gamma squeeze could 3-5x if earnings beat. WBD takeover premium could push stock to $28-30.

Critical warning: These are lottery tickets. FDS trade is 15 days to expiry with zero margin for error. Size TINY.

Swing Trader (3-5% Portfolio)

Multi-week opportunities with institutional backing

Top Swing Plays:

- GLD $400/$415 spread - Follow the $38M whale through January FOMC. 43 days, defined risk, 3.5:1 payoff.

- CRM March $270 calls - Ride the AI momentum into Feb 26 earnings. 106 days, historic institutional backing.

- KWEB spread - China recovery into NPC policy announcements. Defined risk, sophisticated structure.

Risk Management:

- GLD: Stop if gold breaks below $380 support

- CRM: Take profits at 50% gain, reassess before earnings

- KWEB: Close if U.S.-China tensions escalate significantly

Premium Collector (Income Focus)

Harvest premium from high IV

Top Income Plays:

- RBRK covered calls - Follow the $4.5M call seller. Sell $85 January calls collecting 2.5% in 43 days. Stock needs to rally 21.5% to get called away.

- GLD iron condor - If you think gold stays range-bound $375-$410, sell premium on both sides around January expiry.

Why these work: RBRK has no catalyst until March earnings. 56-day dead zone perfect for theta decay. GLD has elevated IV from Fed uncertainty.

Warning: Never sell naked calls without understanding margin requirements. RBRK at $70 going to $85 would cause significant losses on naked short calls.

Entry Level Investor (Learning Mode)

Start small, focus on education

Recommended Starting Points:

- Paper trade first: Watch how FDS earnings plays behave on Dec 18. Learn about IV crush and gamma dynamics without risking capital.

- Study spreads: The GLD and KWEB bull call spreads are textbook examples of defined-risk structures. Understand why smart money uses them.

- Learn hedging: Watch IMO puts through January. This is institutional portfolio insurance in action.

If you must trade real money:

- Consider GLD or CRM shares instead of options (avoid time decay risk)

- Never put more than 1% of portfolio in any single option position

- Avoid FDS and WBD - these are expert-level event-driven plays

Key educational takeaways from today:

- GLD spread: How to get 3.5:1 payoff with defined risk

- CRM: What "2,130x average size" means for institutional conviction

- IMO: Why two trades at same strike, different prices signals fear

- RBRK: How institutions generate income during consolidation

Risk Warnings - Read Before Trading

Universal Rules:

- Position Sizing: YOLO 1-2%, Swing 3-5%, never more than 5% in single options trade

- Stop Losses: 30% loss on options premium triggers exit

- Time Decay: January monthly options losing ~2% per day now; December weeklies losing 5%+ daily

- IV Crush: FDS calls will get crushed 40-50% on earnings even if directionally correct

Today's Specific Risks:

GLD ($38M spread):

- Gold is correlated to dollar strength - strong jobs report could sink gold

- Fed could surprise hawkish at January FOMC

- Geopolitical de-escalation would remove safe-haven bid

CRM ($13M calls):

- Stock already up 40% YTD at all-time highs

- Agentforce scaling could disappoint if enterprises slow AI spending

- February earnings is AFTER Christmas seasonality peak

KWEB ($6.8M spread):

- Trump tariff announcements could crash China tech overnight

- ADR delisting risk remains despite 38% YTD rally

- Property market recovery pushed to late 2026-2027

WBD ($5.2M calls):

- M&A deals can collapse at any moment

- If no deal by January, stock could give back recent gains

- Paramount bid was only $24/share - WBD at $24.37 already

IMO ($3.24M puts):

- Oil could spike on OPEC+ surprise cuts

- Stock has momentum despite fundamentals

- Put decay accelerates in final weeks

The Bottom Line

$73.8 million across 8 tickers, but ONE clear theme: institutions positioning for January FOMC and Q1 2026 catalysts.

The GLD $38M spread is the signal - smart money expects Fed pivot to drive gold breakout. CRM's historic $13M bet validates AI enterprise is the 2026 growth story. Meanwhile, IMO puts and RBRK call selling show not everyone is bullish - some whales are hedging and collecting income.

Key Questions This Week:

- Will gold break $400 before January FOMC?

- Can CRM prove Agentforce scales to 1,000+ deals?

- Does WBD M&A decision come before Christmas?

- Will FDS earnings trigger $290 gamma squeeze?

Remember: These are sophisticated institutional trades that may be part of larger hedged portfolios. Don't blindly follow - understand the thesis, manage risk, and be patient. The best trades often take weeks to play out.

Complete Link Directory

Bullish Plays:

- GLD $38M Bull Call Spread - Fed Pivot + Gold Breakout

- CRM $13M Call Buy - Historic Agentforce Bet

- KWEB $6.8M Bull Call Spread - China Recovery

- WBD $5.2M Call Buy - M&A Speculation

- BDX $1.8M Call Buy - Merger Value Unlock

- FDS $1.3M Call Buy - Earnings Gamma Play

Defensive/Income Plays:

Expiration Tags

Weekly (Dec 19, 2025):

- FDS - Earnings December 18, calls expire December 19

Monthly (Jan 16, 2026):

- GLD - FOMC January 28-29 (AFTER expiry)

- IMO - Q4 earnings January 30 (AFTER expiry)

- RBRK - Q4 earnings March 13 (AFTER expiry)

Quarterly (Mar 20, 2026):

- CRM - Q4 earnings February 26 (BEFORE expiry)

- KWEB - NPC March 5 (BEFORE expiry)

- WBD - Q4 earnings February 27, M&A catalyst (BEFORE expiry)

- BDX - Waters merger Q1 2026 (BEFORE expiry)

Options involve substantial risk and are not suitable for all investors. The unusual activity tracked here represents sophisticated institutional strategies that may be part of larger hedged portfolios not visible to retail traders. These positions represent past institutional behavior and don't guarantee future performance. Always practice proper risk management and never risk more than you can afford to lose completely. The $73.8M tracked today could be hedging activity rather than directional bets - we only see one leg of potentially complex multi-leg strategies.

Total Flow Summary:

- Total Tracked: $73,800,000

- Bullish Positions: $66.1M (90%)

- Defensive Positions: $7.74M (10%)

- Largest Trade: GLD $38M (51% of total flow)

- Expiry Range: December 19, 2025 through March 20, 2026